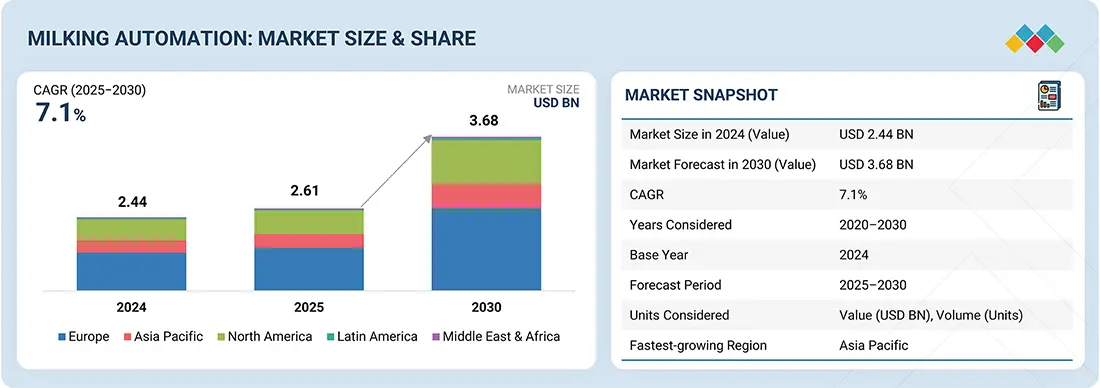

The global milking automation market is valued at USD 2.61 billion in 2025 and is projected to reach USD 3.68 billion by 2030, growing at a CAGR of 7.1%. The market is undergoing a significant transition driven by rising milk demand, labor shortages in dairy farming, and the growing emphasis on efficiency, animal welfare, and sustainability. Traditionally manual, dairy operations are rapidly shifting toward automation through robotic milking systems, automated parlors, and herd management platforms.

Adoption is currently strongest in Europe and North America, where large-scale farms and supportive regulatory frameworks enable deeper market penetration. While global adoption is still developing, growth is expected to be steady as automation addresses key challenges in food security, product quality, resource optimization, and customer-specific production.

Download PDF Brochure:

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=265039621

Software Leading the Offering Segment

Software is projected to capture a major share of the market. Initially limited to basic yield tracking, herd management platforms have evolved into advanced decision-support systems integrating health, reproduction, nutrition, and compliance data. These platforms consolidate inputs from robots, parlors, sensors, and ID systems into actionable dashboards. They track milk yields by stall or robot, flag issues such as incomplete milkings or mastitis risks, and generate daily worklists for reproduction and herd health. Interoperability—through open APIs, standardized data, and localized support—has become essential as farms increasingly rely on multi-vendor solutions.

Growing Role of Goat Dairying

The goat milking automation segment is forecast to register a notable CAGR during the period. Goat dairying is shifting from smallholder production to semi-industrial operations, fueled by demand for specialty cheeses, infant formula ingredients, and lactose-free products. Growth is particularly strong in the Mediterranean, MENA, East Africa, India, China, and North America. Automation solutions for goats must account for unique physiology, requiring smaller teat cup designs, higher pulsation rates at lower vacuum levels, and compact parlor systems. Parallel and rotary parlors equipped with automatic detachers, gentle liners, auto-spray systems, and in-line quality sensors are increasingly deployed for herds ranging from hundreds to thousands. Automated drafting is particularly beneficial for managing seasonal breeding cycles and herd health.

Request Sample Pages:

https://www.marketsandmarkets.com/requestsampleNew.asp?id=265039621

Asia Pacific as the Fastest-Growing Market

The Asia Pacific region is expected to record the highest growth from 2025 to 2030. Rising milk consumption, dietary shifts toward protein, greenfield investments, and modernization policies are accelerating adoption. China is driving growth through mega-dairy projects and vertical integration of data platforms. India is advancing more gradually, with cooperative models and selective adoption of parlors and robotic pilots in commercially active states. Australia and New Zealand represent mature adopters, optimizing pasture-based systems with automation. Meanwhile, Japan and South Korea lead in high-tech dairy adoption, and Southeast Asia is experiencing gradual growth with semi-automation, sensor-based monitoring, and financial models supporting adoption.

Key Market Players:

The report profiles key players such as DeLaval (Sweden), Afimilk Ltd. (Israel), GEA Group (Germany), Nedap N.V. (Netherlands), Allflex Livestock Intelligence (US), BouMatic (US), Waikato Milking Systems (New Zealand), Dairymaster (Ireland), and BECO Dairy Automation Inc. (US).