The report “Nitrogenous Fertilizers Market by Type (Urea, Ammonium Nitrate, Ammonium Sulfate, and Calcium Ammonium Nitrate), Form (Liquid and Dry), Mode of Application (Soil, Foliar, and Fertigation), Crop Type, and Region – Global Forecast to 2022″, The nitrogenous fertilizers market is projected to reach a value of USD 127.00 Billion by 2022, at a CAGR of 2.33% from 2016. The market is driven by factors such as need to increase productivity and level yield and fertilizer intensity gaps across regions, and rise in awareness regarding soil profile and nutritional balance backed by state support.

The objectives of the report are as follows:

- To define, segment, measure, and project the nitrogenous fertilizers market with respect to fertilizer type, crop type, mode of application, form, and key regions

- To identify, analyze, and comment on crucial factors influencing the overall market (drivers, restraints, opportunities, and industry-specific challenges)

- To profile the key players to comprehensively analyze their core competencies and market strategies and provide an overall competitive landscape in the market

- Analyzing the demand-side factors based on the impact of macro and microeconomic factors on the market and shifts in the demand patterns across different subsegments and regions

Download PDF Brochure:

The ammonium nitrate segment is projected to be the fastest-growing from 2016 to 2022

The ammonium nitrate segment is projected to grow at the highest CAGR from 2016 to 2022.Ammonium nitrate is the most effective means of increasing crop yield and has major impact in the productivity of the crop. The increase in awareness with regard to ammonium nitrate in the soil is driving the demand for this segment.

The fruits & vegetables segment is projected to grow at a significant rate during the forecast period

Fruits & vegetables are highly sensitive to the deficiencies of nutrients in the soil. These crops are of high value. The increased demand for fruits & vegetables and their sensitivity toward nutrients is driving the fruits & vegetables segment.

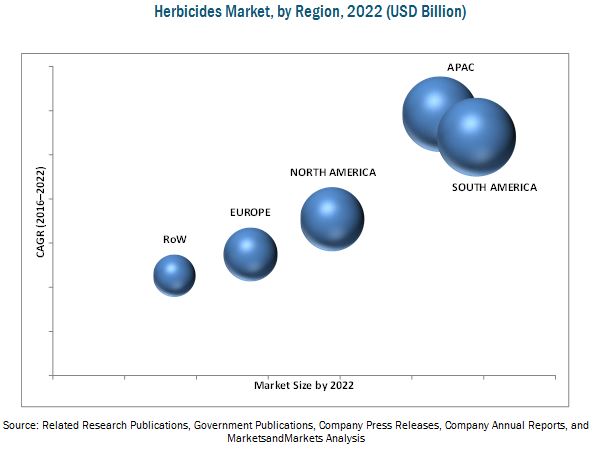

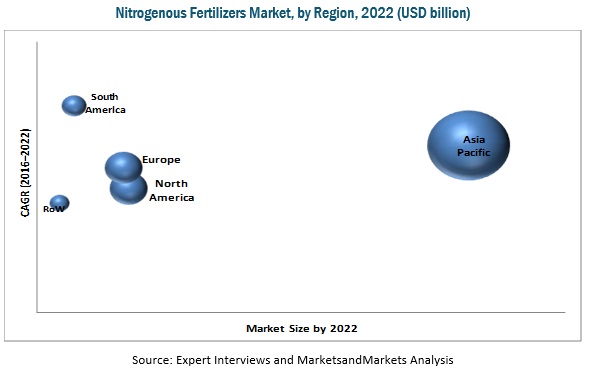

The South American region is projected to grow at a significant rate from 2016 to 2022

The South American region is projected to grow at the highest CAGR during the forecast period, owing to the factors such as growth in population, rise in disposable incomes, progressive urbanization, and increase in demand for nutritional food products that in turn drive the demand for agricultural products. Growth is majorly witnessed in China, India, and Japan owing to the increase in the purchasing power of the population.

This report includes a study of marketing and development strategies, along with the product portfolios of leading companies, such as Yara International ASA (Norway), Agrium Inc. (Canada), Coromandel International Limited (India), Potash Corp. of Saskatchewan Inc. (Canada), and Koch Industries Inc. (U.S.).

Request for Customization:

Target Audience:

- Supply-side stakeholders: fertilizer producers, suppliers, distributors, importers, and exporters

- Demand-side stakeholders: Large contract-scale farming companies, farmers and researchers

- Regulatory-side stakeholders: Concerned government authorities and other regulatory bodies

- Other related associations, research organizations and industry bodies: Food and Agriculture Organization (FAO), International Fertilizer Industry Association (IFA), International Fertilizer Society (IFS) and Organization for Economic Co-operation and Development (OECD)