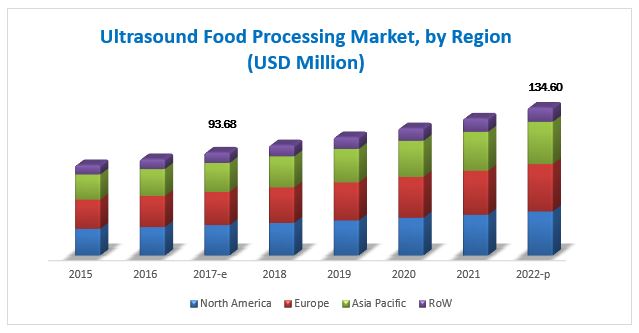

The food ultrasound market has grown exponentially in the last few years. The market was valued at USD 93.7 Million in 2017 and is projected to reach USD 134.6 Million by 2022, growing at a CAGR of 7.5% from 2017. Emerging economies such as India, China, Japan, South Africa, and Brazil are the potential primary markets of the industry. Concerns regarding food wastage and energy savings during food processing are prompting companies to adopt ultrasonic technology. The increasing R&D in the field of ultrasonic food processing to reduce wastage during processing and maintaining the quality of the food product is also one of the important drivers responsible for growth in this market.

The objectives of the study are:

- To define, segment, and forecast the size of the food ultrasound market with respect to frequency range, function, food product, and region

- To analyze the market structure by identifying various subsegments of the food ultrasound market

- To forecast the size of the food ultrasound market and its various submarkets with respect to four main regions, namely, North America, Asia Pacific, Europe, and the Rest of the World (RoW)

- To provide detailed information about the crucial factors that are influencing the growth of the market (drivers, restraints, opportunities, and challenges)

- To analyze the opportunities in the market for stakeholders and provide details of the competitive landscape for market leaders

- To strategically profile the key players and comprehensively analyze their market ranking and core competencies

- To analyze the competitive developments such as expansions, new product & technology launches, acquisitions, mergers, collaborations, and partnerships in the food ultrasound market

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=139070556

The meat & seafood segment is projected to grow at the highest CAGR, by food product, from 2017 to 2022.

Ultrasound increases the shelf-life and helps in the retention of natural flavor, texture and tenderness of the meat. It provides solutions for thawing, microbial inactivation, and packaging of meat products without affecting its quality.

The quality Assurance segment dominated the market, by function, from 2017 to 2022.

Ultrasound waves are used to detect the physical & chemical characteristics of products. Low-intensity high-frequency waves are applied to characterize the food components during pre, post, and inline processing. Ultrasound waves also monitor the physiochemical changes that the food undergoes after freezing, drying, thawing, and emulsifying. Quality assurance is a non-destructive function of ultrasound application.

Significant growth for food ultrasound is observed in the Asia Pacific region.

The growth in this region is driven by China, India, and Japan, which has led manufacturers to adopt strategies such as geographical expansions and product launches in these regions. Manufacturers are opting for technological advancements in their practices through R&D to expand their business offerings and increase their profit margins. The demand for ultrasonic food processing is high in food manufacturing-based economies due to the adoption of the latest techniques for food processing to meet the growing food demand.

This report includes a study of the business strategies, along with the product portfolios of leading companies. It includes the profiles of leading companies such as Bosch (Germany), Emerson (US), Bühler (Switzerland), Dukane (US), and Heilscher (Germany).

Target Audience:

- Manufacturers, importers & exporters, traders, distributors, and suppliers of ultrasonic food processing equipment

- Food processing companies

- Packaged food manufacturers

- Raw material suppliers

- Food technologists

- Government and research organizations

- Regulatory bodies

- End users