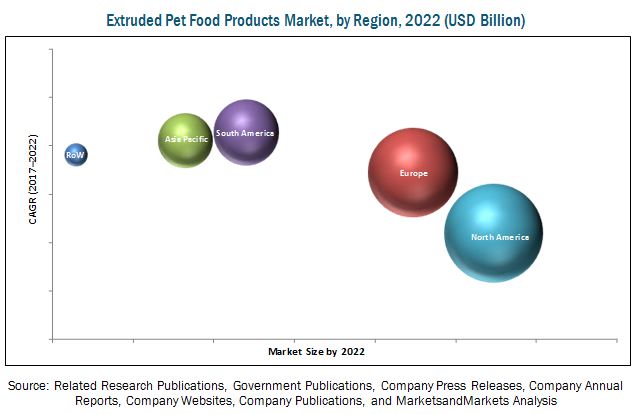

The report "Pet Food Extrusion Market by Extruded Pet Food Products (Type (Complete Diets and Treats), Animal Type (Dogs, Cats, Fish, and Birds), and Ingredient), by Pet Food Extruder Equipment (Type (Single and Twin Screw)), and Region - Global Forecast to 2022", The global pet food extrusion market is estimated to be valued at USD 55.21 Billion in 2017, and expected to grow at a CAGR of 5.6% to reach USD 72.64 Billion by 2022. The market for pet food extrusion is showing significant growth with a rise in the popularity of pet adoption, pet humanization, and rapid urbanization in developing economies such as China, India, Argentina, and Mexico. The growing pet population across the globe is one of the leading factors that contribute to the demand for extruded pet food products, worldwide. The need to fulfil the growing demand for pet food is simultaneously fueling the growth of the pet food equipment manufacturing industry.

- To define, segment, and project the global extruded pet food products market size based on type, ingredient, animal type, and region

- To define, segment, and project the global pet food extrusion equipment market size based on type, process, and region

- To provide detailed information about the key factors influencing the growth of the market (drivers, restraints, opportunities, and challenges)

- To analyze the opportunities in the market for stakeholders and provide the competitive landscape of the market leaders

- To project the size of the market and its submarkets, in terms of value and volume, with respect to the regions (along with the key countries)

- To strategically profile key players and comprehensively analyze their market position and core competencies

- To analyze the competitive developments such as expansions, acquisitions, collaborations, rebranding, and new product developments in the pet food extrusion market

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=264161682

- Extrusion machinery, technology, and equipment manufacturers and suppliers

- Extruded pet food product manufacturers, suppliers, and distributors

- Extrusion machinery spare part suppliers and distributors

- Regulatory and research organizations

- Food and agriculture organizations such as the FAO and USDA

- Associations and industry bodies such as the Pet Food Manufacturers Association (PFMA), and The Europe Pet Food Industry (FEDIAF), The Brazilian Association of Pet Products Industry (ABINPET), The Pet Food Industry Association of Australia (PFIAA), The Pet Food Manufacturers Association (PFMA), Russia, and The Europe Pet Food Industry (FEDIAF)

- Government agencies and NGOs

- Food safety agencies