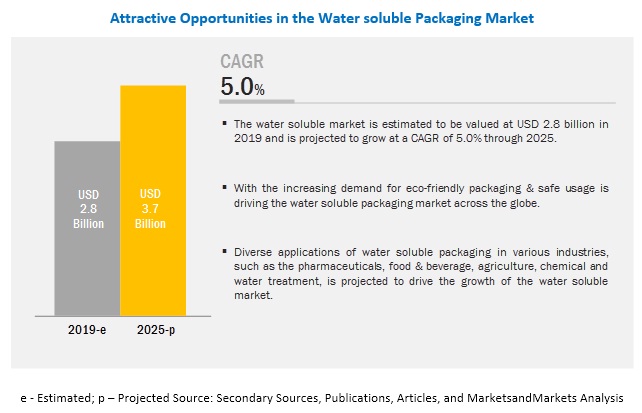

The water-soluble packaging market is estimated to be valued at USD 2.8 billion in 2019 and is projected to reach USD 3.7 billion by 2025, recording a CAGR of 5.0% during the forecast period. The increasing demand for sustainable and green packaging drives the market growth for water-soluble packaging.

Key players in this market include Lithey Inc. (India), Mondi Group (Austria), Sekisui Chemicals (Japan), Kuraray Co. Ltd. (Japan), Mitsubishi Chemical Holdings (Japan), Aicello Corporation (Japan), Aquapak Polymer Ltd (UK), Lactips (France), Cortec Corporation (US), Acedag Ltd. (UK), MSD Corporation (China), Prodotti Solutions (US), JRF Technology LLC (US), and Amtopak Inc. (US).

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=243293980

Kuraray Co. Ltd (Japan) is a key supplier, offering products in categories such as resins, chemicals, fibers, and textiles based on polymer and synthetic technologies. Its operations focus on becoming a specialty chemical company, which is growing sustainably by incorporating new foundational platforms into its own technologies. It is pursuing competitive superiority by creating new demand and by developing high-value-added and customized products and applications such as transfer printing technologies and dust abatement technologies based on client requirements. MonoSol, a subsidiary of Kuraray Co. Ltd., led the way with its unit dose technology, collaborating with marketers to develop laundry detergent products and created a new product category, water-soluble film-packaged products in the detergent industry. It encapsulates laundry and dishwasher pods or packs, which would eliminate the need to pour and measure liquids or powders.

In 2018, the company established a water-soluble film manufacturing facility in Indiana, US. The development helped the company to strengthen its market position in the US.

Aquapak Polymer Ltd (UK) is a privately held company headquartered in Birmingham and one of the leading developers, manufacturers, and distributors of biodegradable and marine safe polymer films for packaging. The company works in collaboration with the brands and retailers, and packaging manufacturers to design circular economy solutions to replace single-use plastic packaging.

Aquapak Polymer Ltd. offers polymer-based products under the brand, Hydropol. Product is categorized as water-soluble, stable & storable, heat-sealable, electrostatic-resistant, and ultraviolet-resistant.

In October 2019, the company launched garment packaging bags made from Aquapak polymer Ltd. in collaboration with Finisterre (UK), a garment company . The company aims to replace traditional packaging with soluble packaging.

Request for Customization:

https://www.marketsandmarkets.com/requestCustomizationNew.asp?id=243293980

https://www.marketsandmarkets.com/requestCustomizationNew.asp?id=243293980

The water soluble packaging market in Asia Pacific is projected to witness high growth due to the strong local and export demand. The rising population and growing number of manufacturing industries in Asia Pacific is the key factor driving the market for water soluble packaging. The manufactured product is used domestically as well as exported. China and Japan are the hubs for water soluble film production. In India, the population is increasing rapidly, and the country is striving for a safe, better, clean, and healthy lifestyle. The water soluble packaging market will grow in these regions at a high rate.

Key Questions Addressed by the Report:

- What are the growth opportunities in the water soluble packaging market?

- What are the major raw materials used for manufacturing water soluble packaging?

- What are the key factors affecting market dynamics?

- What are some of the significant challenges and restraints that the industry faces?