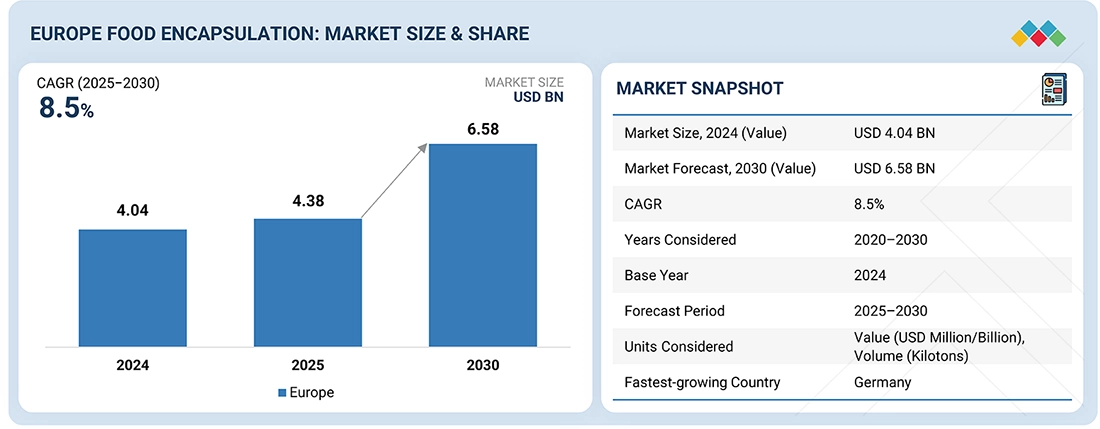

According to MarketsandMarkets™, The Europe Food Encapsulation Market is projected to grow from USD 4.38 billion in 2025 to USD 6.58 billion by 2030, registering a Compound Annual Growth Rate (CAGR) of 8.5% during the forecast period. The market is witnessing steady expansion as food and ingredient manufacturers across Europe increasingly prioritize product stability, shelf life, and quality.

Food encapsulation has emerged as a critical technology for protecting sensitive ingredients such as vitamins, minerals, probiotics, and antioxidants. By coating these actives with protective layers, encapsulation shields them from heat, moisture, and oxygen, ensuring consistent performance during processing, storage, and consumption. As a result, the technology has become integral to the food, nutrition, and pharmaceutical industries.

Key European markets contributing to demand include Germany, France, the United Kingdom, Italy, Spain, and the Nordic countries. Clean-label requirements, enhanced product quality, and extended shelf life remain top priorities for manufacturers in the region. Market growth is further supported by advancements in encapsulation technologies such as spray drying, coacervation, extrusion, and lipid-based systems, which enable controlled release, improved absorption, and better ingredient stability. Rising consumer interest in functional and fortified foods continues to strengthen adoption across applications.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=220568560

Nanoencapsulation Emerges as the Fastest-Growing Technology Segment

By technology, nanoencapsulation is projected to grow at the fastest rate in the Europe food encapsulation market. This growth is driven by its superior ability to protect sensitive ingredients and enhance bioavailability. Nanoencapsulation enables precise control over the release of flavors, vitamins, enzymes, antioxidants, and probiotics, making it particularly suitable for functional and fortified food products.

The technology aligns well with Europe’s clean-label and premium product trends, while also helping to reduce taste challenges and improve shelf life. Although nanoencapsulation currently involves higher costs than traditional methods, ongoing process optimization and scaling are steadily narrowing this gap. With Europe’s strong focus on functional nutrition, advanced food research, and collaboration between food brands and technology providers, nanoencapsulation is gaining rapid traction.

Functional Foods Lead Application Demand

By application, functional food products account for a significant share of the Europe food encapsulation market. Encapsulation allows manufacturers to incorporate health-promoting ingredients—such as vitamins, minerals, probiotics, enzymes, and omega fatty acids—into everyday foods without compromising quality or stability.

European consumers increasingly seek foods that support health, immunity, digestion, and energy, driving demand for fortified dairy products, cereals, bakery items, and nutrition bars. Encapsulation helps food brands meet both performance and clean-label expectations, while Europe’s strong retail infrastructure and harmonized food standards further support widespread adoption. As functional foods become a routine part of daily diets, this segment continues to dominate the market.

Germany Holds a Leading Market Position

Based on country, Germany accounts for a significant share of the Europe food encapsulation market. The country hosts one of the largest food and beverage industries in the region and widely applies encapsulation technologies in functional foods, dairy products, bakery items, and nutritional offerings.

Germany benefits from advanced food processing infrastructure, sustained investment in food research, and close collaboration between manufacturers, ingredient suppliers, and research institutions. High consumer awareness around health, product quality, and transparent labeling, combined with strict food safety regulations and efficient supply chains, continues to drive demand for encapsulated ingredients. As a result, Germany remains a key contributor to the overall growth of the European market.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=220568560

Leading Europe Food Encapsulation Companies:

The Europe food encapsulation market features the presence of several prominent players, including BASF SE (Germany), Kerry Group plc (Ireland), DSM-Firmenich (Switzerland), Givaudan (Switzerland), Symrise (Germany), Lonza (Switzerland), Evonik (Germany), Lallemand Inc. (Canada), Firmenich SA (Switzerland), and Sensient Technologies Corporation (US).

As the European food industry increasingly shifts toward value-added, performance-driven products, food encapsulation is expected to remain a vital technology supporting innovation and market growth across the region.