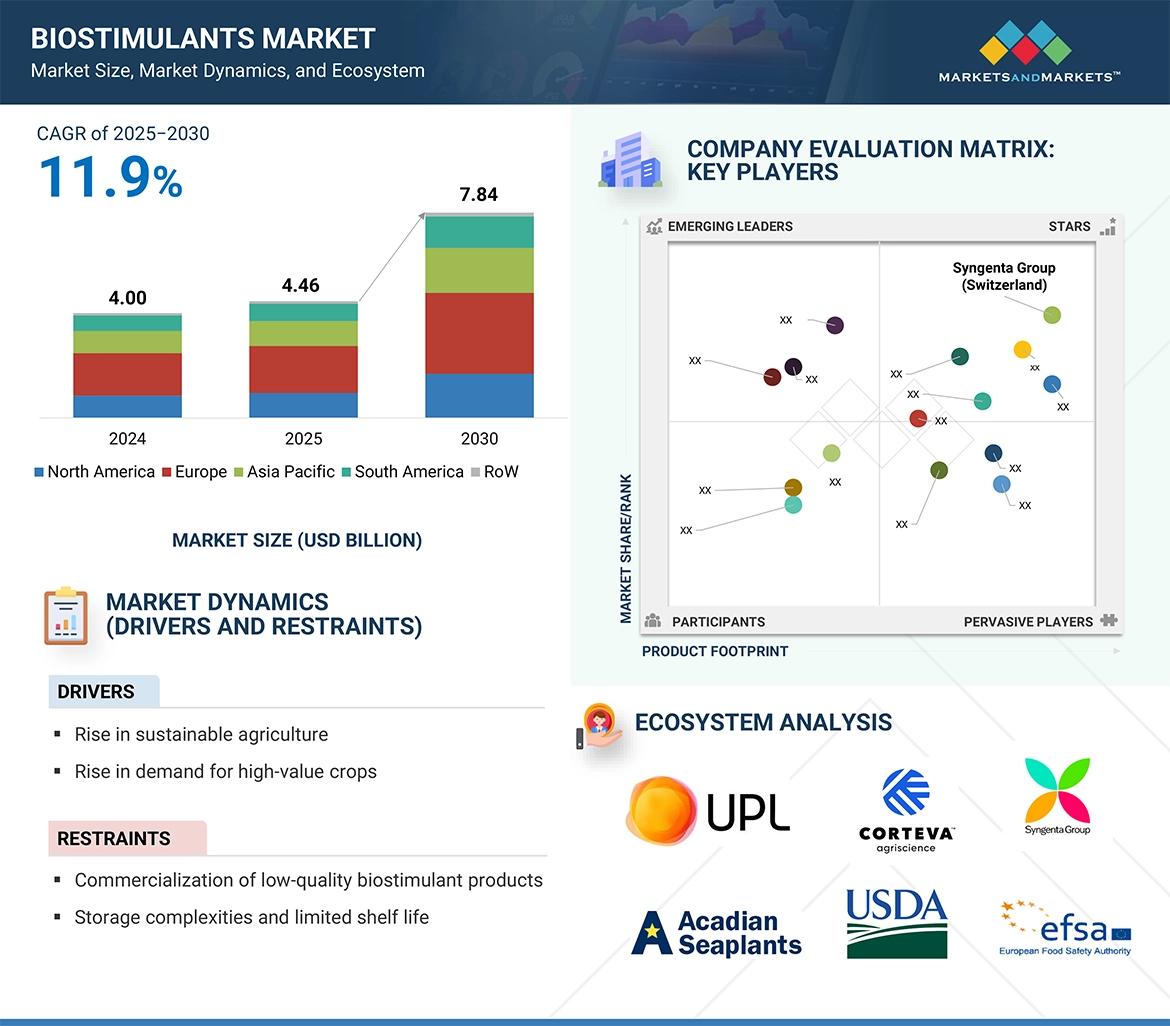

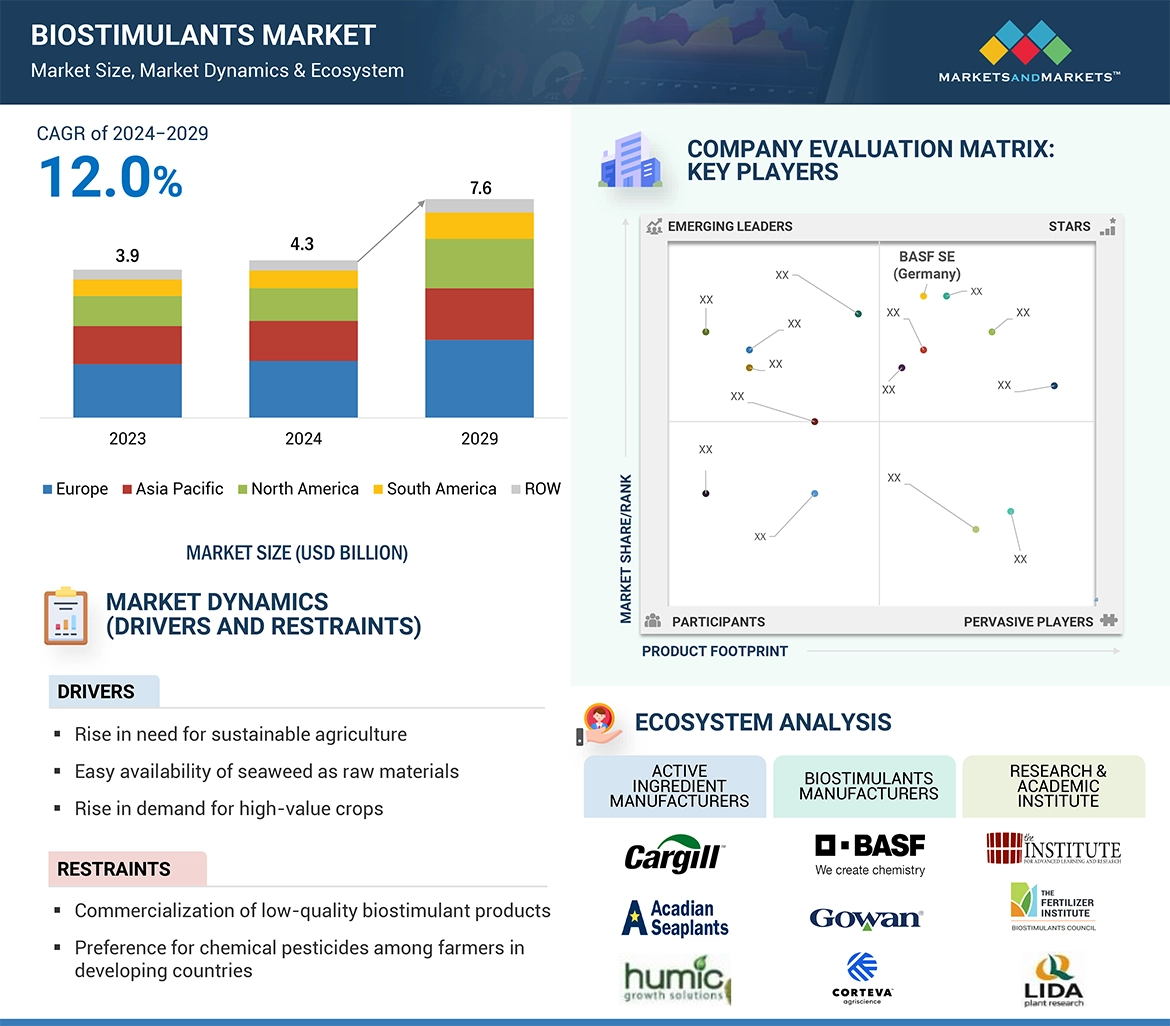

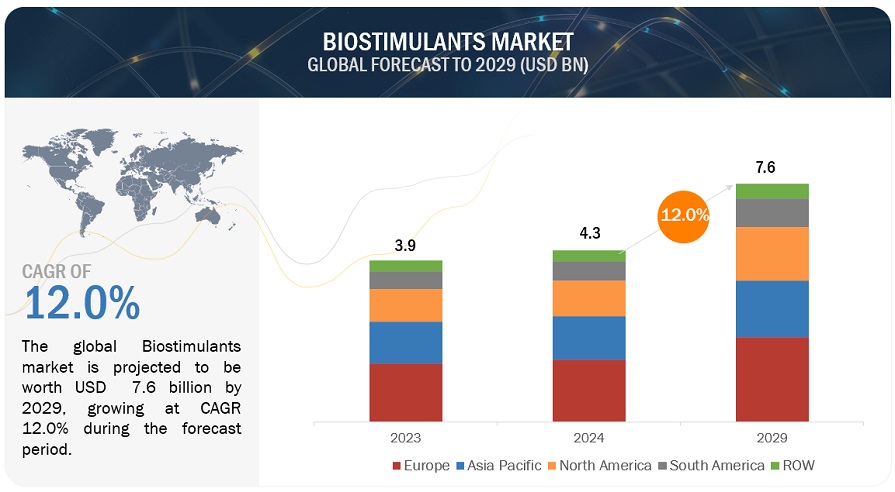

The global biostimulants market is projected to grow from USD 4.97 billion in 2026 to USD 8.77 billion by 2031, registering a Compound Annual Growth Rate (CAGR) of 12.0% during the forecast period. The market is experiencing robust expansion as farmers, agribusinesses, and commercial growers increasingly adopt biostimulants to improve crop productivity while promoting environmentally sustainable agricultural practices.

The growing emphasis on

improving nutrient efficiency, enhancing plant resilience to environmental

stresses, and maintaining long-term soil health has significantly accelerated

the adoption of biostimulants worldwide. Europe and North America continue to lead

market adoption, particularly in cereal, horticultural, and high-value crop

production, where biostimulants play a critical role in improving crop

performance and yield stability.

The rising demand for

microbial-based products, seaweed extracts, amino acid formulations, and other

natural biostimulant solutions is further strengthening market growth. In

addition, advancements in precision agriculture, digital farming technologies, agritech

platforms, and expanding distribution networks are making these products more

accessible to both commercial and smallholder farmers across global

agricultural markets.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=1081

Liquid Form Segment

Dominates the Market

Among various product forms,

the liquid segment continues to account for a significant share of the global

biostimulants market. Liquid biostimulants are widely preferred due to their

ease of application, uniform crop coverage, and compatibility with foliar

spraying, fertigation, and seed treatment systems.

These formulations—including

microbial suspensions, seaweed extracts, amino acid blends, and nutrient-based

solutions—offer rapid absorption, efficient nutrient delivery, and enhanced

protection against abiotic stresses. Their ability to integrate seamlessly with

existing crop nutrition and crop protection programs has further increased

their popularity among growers seeking convenient, ready-to-use solutions for

improving crop performance.

Cereals & Grains Segment

Registers Strong Growth

Based on crop type, the

cereals & grains segment is expected to witness substantial growth

throughout the forecast period. Extensive cultivation of staple crops such as

wheat, rice, and maize continues to drive demand for biostimulants that enhance

nutrient uptake, stimulate root development, and improve tolerance to drought,

heat, and salinity.

Growing global demand for

food grains, supportive government initiatives promoting sustainable

agriculture, and increasing farmer awareness regarding yield optimization are

contributing significantly to segment growth. The widespread application of

microbial, seaweed-based, and amino acid biostimulants is helping improve crop

productivity while supporting sustainable farming objectives.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=1081

North America Holds a

Significant Market Share

North America represents a

significant share of the global biostimulants market, supported by advanced

farming practices, increasing investment in biological crop inputs, and

widespread adoption of sustainable agriculture technologies.

Farmers across the United

States and Canada are increasingly utilizing biostimulants to improve nutrient

use efficiency, strengthen plant resilience under environmental stress, and

preserve soil fertility while reducing dependence on conventional agrochemicals.

Favorable regulatory developments, continued research and innovation, and the

expansion of high-value crop cultivation—including fruits, vegetables, and

specialty crops—are expected to further support regional market growth.

Leading Biostimulants

Companies:

Major companies operating in

the global biostimulants market include UPL Limited (India), FMC Corporation

(US), Corteva Agriscience (US), Sumitomo Chemical Co., Ltd. (Japan), Nufarm

Limited (Australia), Novonesis (Denmark), BASF SE (Germany), Bayer AG (Germany),

PI Industries Ltd. (India), T. Stanes & Company Limited (India), J.M. Huber

Corporation (US), Gowan Company (US), Koppert Biological Systems (Netherlands),

Acadian Seaplants Limited (Canada), Qingdao Seawin Biotech Group Co., Ltd.

(China), OMEX Agriculture (UK), Seipasa S.A. (Spain), Aminocore (South Africa),

and Cascadia Seaweed Corp. (Canada).