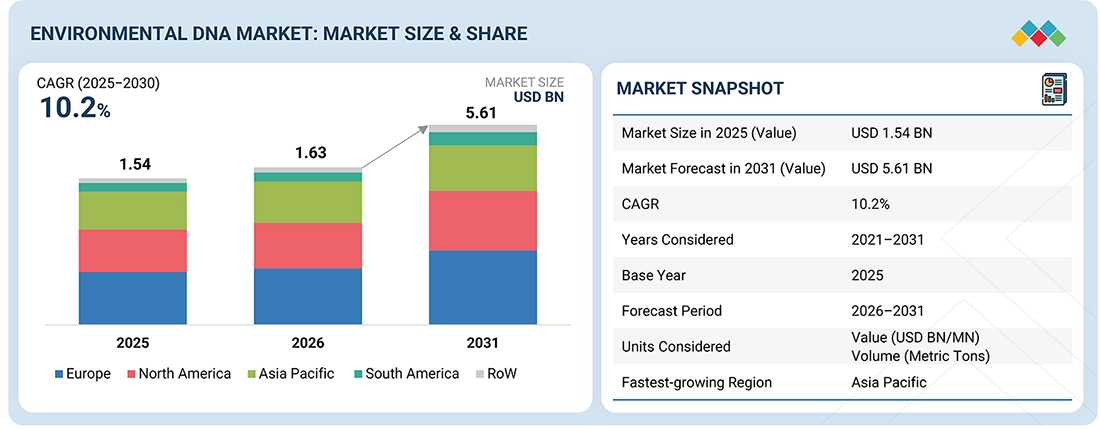

The environmental DNA market is expected to expand from USD 1.63 billion in 2026 to USD 5.61 billion by 2031, registering a Compound Annual Growth Rate (CAGR) of 10.2% over the forecast period. This growth reflects the increasing adoption of molecular-based techniques for efficient and accurate environmental monitoring across multiple sectors. eDNA is widely applied in biodiversity assessment, invasive species detection, conservation programs, water quality evaluation, and climate impact research. Its demand is accelerating as it provides a cost-effective, non-invasive alternative to conventional survey methods by detecting species from trace DNA present in water, soil, and sediment samples. Adoption is increasing among research institutions, environmental agencies, and industries such as aquaculture. Continuous advancements in PCR technologies, next-generation sequencing, and bioinformatics are further strengthening market growth. In addition, stricter environmental regulations and rising biodiversity conservation funding are supporting broader implementation. Standardized workflows are also improving scalability and operational efficiency. As competition intensifies, market focus is shifting toward delivering high-accuracy data, faster processing times, and integrated end-to-end solutions spanning sample collection to final reporting.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=87204702

By type of solution, the services segment accounts for a significant share.

The services segment, encompassing sample collection, field operations, laboratory testing, sequencing, bioinformatics analysis, data interpretation, and end-to-end project management, holds a notable share of the environmental DNA market. This dominance is driven by the demand for comprehensive, turnkey solutions. Many end users—including environmental agencies, research organizations, and commercial enterprises—prefer outsourced services as they eliminate the need for in-house technical infrastructure and specialized expertise. These service offerings cover the entire workflow, beginning with field sampling and progressing through laboratory processing and sequencing, ultimately delivering structured reports and actionable insights. This integrated approach enables the execution of large-scale and complex environmental monitoring initiatives. Laboratory and sequencing services ensure high detection accuracy, while bioinformatics converts raw genetic data into meaningful ecological interpretations. End-to-end services further streamline project execution and improve efficiency. Growing requirements for biodiversity monitoring, regulatory compliance, and environmental impact assessments are further driving demand. Additionally, service providers offer standardized methodologies, consistency, and faster turnaround times, which are critical for time-sensitive applications.

By detection method, the metabarcoding segment is estimated to maintain strong growth.

The metabarcoding segment is projected to sustain strong growth in the environmental DNA market due to its capability to identify multiple species simultaneously from a single environmental sample. In contrast to targeted methods such as qPCR, which detect individual species, metabarcoding utilizes high-throughput sequencing to analyze mixed DNA samples and provide a comprehensive overview of biodiversity. This makes it highly suitable for large-scale ecological assessments across aquatic and terrestrial environments. It is extensively used in biodiversity monitoring, ecosystem evaluation, and environmental impact studies where understanding species diversity and community structure is essential. The method enables simultaneous detection of fish, plants, microorganisms, and other taxa, offering a holistic view of ecosystems. Market growth is supported by continuous improvements in sequencing technologies, declining sequencing costs, and the expansion of reference genetic databases. Furthermore, advancements in bioinformatics tools and the development of standardized analytical workflows are improving data reliability and reproducibility.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=87204702

Based on region, Europe holds a substantial share.

Europe represents a significant share of the environmental DNA market, driven by strong environmental regulations and structured ecological monitoring frameworks. Regulatory initiatives such as the EU Water Framework Directive and the EU Biodiversity Strategy mandate continuous monitoring of aquatic and terrestrial ecosystems, which has accelerated the adoption of eDNA-based approaches. The technology is widely utilized by governmental agencies, academic institutions, and environmental service providers for applications including freshwater monitoring, invasive species detection, and ecosystem health assessments. Key countries such as the UK, Germany, France, and Nordic nations demonstrate consistent adoption, supported by well-established research infrastructure and collaborative environmental programs. Steady funding for environmental research further strengthens market development, with universities, regulators, and private organizations working together on monitoring initiatives. This collaboration has contributed to greater standardization of methodologies and improved data reliability. Additionally, the region benefits from advanced laboratory networks and experienced service providers, enabling efficient execution of large-scale and complex environmental studies.

Top Environmental DNA Companies:

The market landscape includes leading players such as Thermo Fisher Scientific Inc. (US), QIAGEN (Netherlands), Illumina, Inc. (US), Eurofins Scientific (Luxembourg), SGS Société Générale de Surveillance SA (Switzerland), NatureMetrics (UK), EnviroDNA (Australia), EDNAtec (Canada), SPYGEN (France), ID-GENE ecodiagnostics Ltd. (France), Takara Bio Inc. (Japan), Stantec (Canada), Applied Genomics (UK), AllGenetics (Spain), and Jonah Ventures (US).