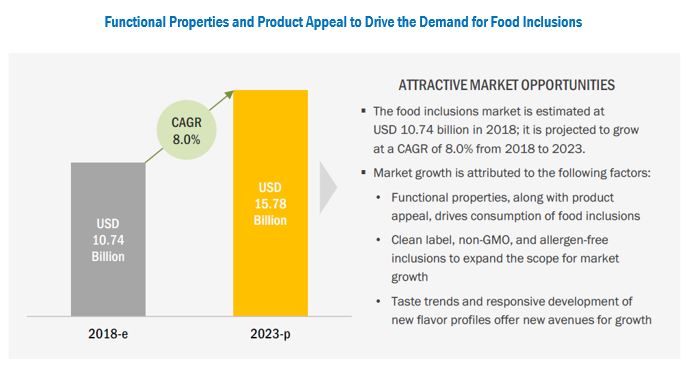

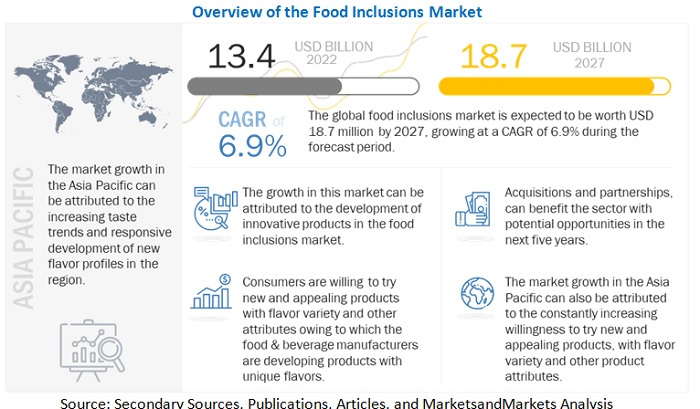

The food inclusions market is projected to reach of USD 18.7 billion by 2027, recording at a CAGR of 6.9%. It was estimated to be valued at USD 13.4 billion in 2022. The changing dynamics, owing to the factors such as the changing consumer requirements, industrial investments, R&D, increasing stringency of food regulations, and greater urge among industry players to attain the market leadership position, have led to continuous innovations in product offerings by market players, which are aligned with consumer demand.

Food inclusions have enabled food & beverage manufacturers to improve organoleptic properties, especially in terms of flavor, taste, texture, and appearance. As a result, mass-marketed products and products such as oats and cereal specifically targeted at health-conscious consumers are gaining significant demand from consumers, owing to their inclusion content. The use of inclusion has also aided product manufacturers in adopting and continuing with their marketing strategies and positioning their products as "healthy" without violating the prevailing norms of food labeling.

Download PDF Brochure:

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=43206052

Drivers: Functional properties along with product appeal drive consumption of food inclusions

In the constantly changing dynamics of the food industry, where consumer demands are ever-changing and manufacturers are increasingly shifting their attention from offering actual products to augmented products, the introduction of novel ingredients, such as food inclusions, is gaining global significance. Their usage in food & beverage products has enabled manufacturers to overcome some of the challenges faced with products and their formulations in terms of flavor enhancement, appearance & visual appeal, flavor masking, thickening, and textural issues.

Along with the enhancement of these attributes, the addition of food inclusions has added new aspects to food & beverage products that have aligned well with consumer tastes and preferences, resulting in their growing popularity. In response, manufacturers of food & beverage products are focusing and investing significantly in developing products that will enable innovative usage of food inclusions with other ingredients and additives to make their products more appealing to consumers. This has, in turn, encouraged manufacturers of food inclusions to develop their products in a wide variety, functionality, and customized manner to enable their introduction in end products.

By application, the cereals products, snacks & bars segment is projected to dominate the food inclusions market in the forecasted period.

Food inclusions, with their ability to enhance organoleptic properties and nutritional profile, are ideal ingredients for addition in cereal products, snacks & bars, as they enhance product appeal. Consequently, inclusions are significantly consumed for use in products in this category, as their content has become the Unique Selling Proposition (USP) and core factor of product marketing.

Request Sample Pages:

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=43206052

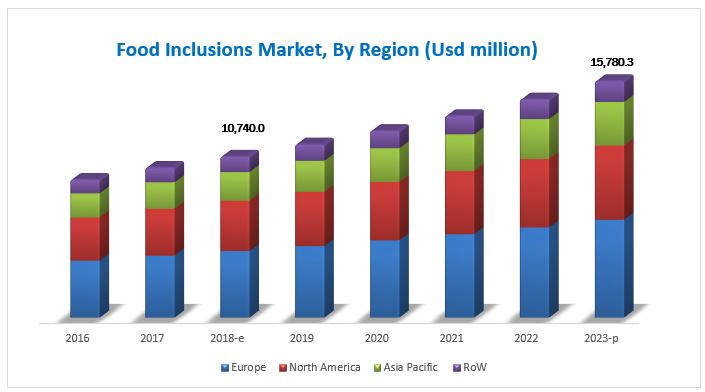

By region, Europe was the largest regional market for the food inclusions industry

The European market accounted for the largest share in 2021. The largest market share of Europe can primarily be attributed to factors such as the region's large-scale production and domestic consumption of food inclusions. Moreover, food & beverage manufacturers urge product innovation with the use of novel ingredients to cater to consumer indulgence. The market in the Asia Pacific is projected to grow at the highest CAGR of 9.5%, owing to the rising consumption of inclusions and their innovative usage in line with the flavor profile and other consumer requirements, along with the westernization of diets.