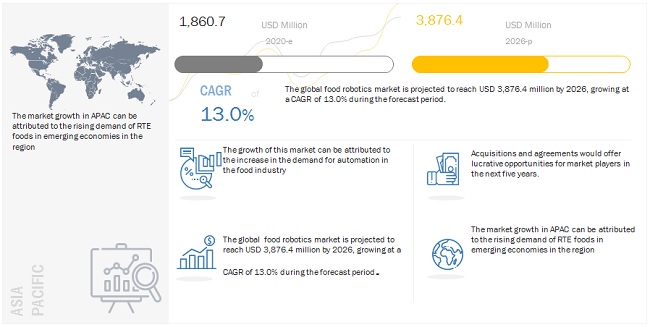

The global food robotics market size is estimated to be valued at USD 1.9 billion in 2020 and projected to reach USD 4.0 billion by 2026, recording a CAGR of 13.1% during the forecast period. The demand for food robotics is increasing significantly owing to surging demand for food with increasing population and increasing demand for enhanced productivity in food processing. Additionally, increasing investments in automation in the food industry is projected to provide growth opportunities for the food robotics market.

Download PDF Brochure @

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=205881873

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=205881873

Key players in this market include ABB Group (Switzerland), KUKA AG (Germany), Fanuc Corporation (Japan), Kawasaki Heavy Industries Ltd. (Japan), Rockwell Automation Inc. (U.S.), Mitsubishi Electric Corporation (Japan), Yasakawa Electric Corporation (Japan), Denso Corporation (Japan), Nachi-Fujikoshi Corporation (Japan), Universal Robots A/S (Denmark), Staubli International AG (Switzerland), Bastian Solutions LLC (U.S.), Schunk GmbH (Germany), Asic Robotics AG (Switzerland), Mayekawa Mfg. Co. Ltd. (Japan), Apex Automation & Robotics (Australia), Aurotek Corporation (Taiwan), Ellison Technologies Inc. (U.S.), Fuji Robotics (Japan), and Moley Robotics (U.K.).

Mitsubishi Electric Corporation (Japan) is primary involved in the manufacturing, development, and marketing of different equipment used in industries such as packaging/food and beverage, general manufacturing, automotive, semiconductor, heath care, and education. The company provides solutions for the packaging/ food and beverage segment such as packaging, picking and placing, material handling, and dispensing as robots have the capability to handle products quicker and safer than conventional applications.

The company operates through six business segments-energy and electric systems, industrial automation systems, home appliances, information and communication systems, electronic devices, and others. Mitsubishi Electric Corporation has its operations in Japan, Asia-Pacific, Europe, the Americas, and the Middle East & Africa. Some of the subsidiaries of Mitsubishi Electric include Mitsubishi Electric Automation Korea Co., Ltd (Korea), Mitsubishi Electric Europe B.V. German Branch, Mitsubishi Electric Australia Pty. Ltd. (Australia), and Mitsubishi Electric (China) Co., Ltd.

ABB Group (Switzerland) is a global leader in power and automation technologies enabling utility, industry, and transport and infrastructure sectors to improve their performance while lowering the environmental impact. Its operations are organized into five business segments, namely, power products, power systems, discrete automation and motion, low voltage products, and process automation. The company is a leading supplier of industrial robots and modular manufacturing systems and services. ABB has installed more than 250,000 robots worldwide. Its robotics solutions are used in industries such as automotive, metal fabrication, foundry, plastics, food & beverage, chemicals & pharmaceuticals, consumer electronics, solar, and wood. ABB’s robotic solutions are used in industry applications such as welding, material handling, painting, picking, packing, and palletizing. ABB operates in approximately 100 countries across four regions-Europe, the Americas, Asia, and the Middle East and Africa (MEA). Some of its major subsidiaries are ABB Holdings Limited, Warrington (UK), ABB Norden Holding AB (Sweden), ABB Group., Seoul (South Korea), ABB K.K., Tokyo (Japan), ABB (China) Ltd., Beijing, ABB Group, Osasco (Brazil), and ABB AG, Mannheim (Germany).

Speak to Analyst @ https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=205881873

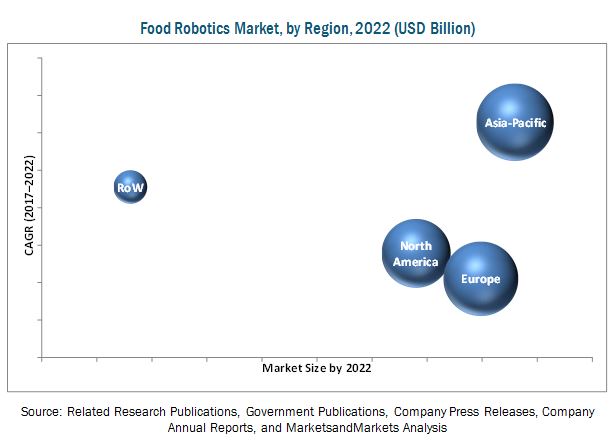

The European food robotics market is driven by high investment in research & development with regard to technology, along with the rise in demand for packed, ready-to-cook, and high-quality food products. The European Robotics Association started monitoring in European Union activities, policies, and funding in the new robot technology to strengthen the international market for food & beverage manufacturing, which is likely to impact the adoption of food robotics positively.