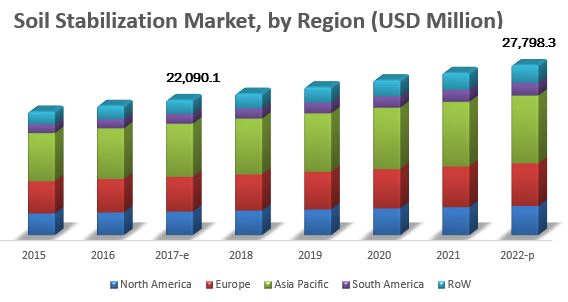

The report "Soil Stabilization Market by Method (Mechanical and Chemical), Application (Industrial, Non-agricultural, and Agricultural), Additive (Polymer and Mineral & Stabilizing Agents), and Region (APAC, North America, Europe) - Global Forecast to 2022", The global soil stabilization market is estimated at USD 22.09 Billion in 2017, and is projected to reach USD 27.80 Billion by 2022, at a CAGR of 4.70% during the forecast period. The market is driven by factors such as improved quality and properties of soil stabilization materials and urbanization. The use of different soil stabilization additives in the optimum quantities provides numerous benefits to the soil. Rapid urbanization, particularly in the developing regions, is driving the growth of the construction industry, thereby fueling the soil stabilization market growth.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=23555531

Based on application, the soil stabilization market has been segmented into industrial, non-agriculture, and agriculture. The industrial segment dominated the global market, and this trend is expected to continue through the forecast period. The rising technological advancements in machinery and additives help the industry players grow and capitalize on the existing opportunities. Soil stabilization finds industrial applications in roads, airfields, railroads, embankments, reservoirs, bank protection, canals, dams, and coastal engineering. With the infrastructure development across the globe, innovations are foreseen to drive the market for soil stabilization materials in the coming years.

The global market has been segmented, on the basis of method, into mechanical and chemical. The mechanical method segment dominated the global market with a majority of the share. The mechanical method includes various soil stabilization machines such as compactors, rollers, and pavers to improve the strength of the soil. The mechanical method helps in properly and consistently mixing the soil, which can be used in subgrades and design of foundations.

Speak to Analyst:

The South American market is projected to grow at the highest CAGR during the forecast period. The countries covered under the region include Brazil and Argentina. Rising demand for infrastructural development and increasing income levels in emerging economies such as Brazil and Argentina are the key factors that drive the growth of the soil stabilization market. The development and growth of various agricultural sectors drive the demand for soil stabilization in the region.

This report includes a study of various soil stabilization machines and additives, along with the product portfolios of leading companies. It includes the profiles of leading companies such as Caterpillar (US), AB VOLVO (Sweden), FAYAT (France), WIRTGEN GROUP (Germany), and CARMEUSE (US).