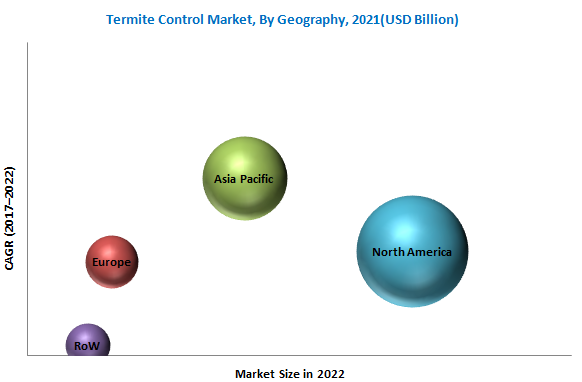

The global termite control market is estimated at USD 3.13 billion in 2017 and is projected to reach USD 4.12 billion by 2022, at a CAGR of 5.62% during the forecast period. The primary factors that drive the market has been the growing presence of termite control service providers in developing economies, and many instances of insect pest attacks with respect to climate change.

Unhygienic conditions, increasing population in various countries, and improper waste management cause termite infestations. Termites are small insects, similar to ants, and eat dead plants and trees or other wooden materials. There are over 2,300 species of termites across the world. The termite control market, by species, has been segmented into subterranean termites, dampwood termites, drywood termites, and others, such as conehead termites and desert termites. Subterranean termites are found in all the regions and thus occupy major share for market. The termite control market, by control method, has been segmented into chemical, mechanical & physical, biological, and other methods, which include environmental control services and radiation. The chemical segment dominated the market in 2016, where insect growth regulators and various larvicides, such as diflubenzuron and noviflumuron are projected to gain significant market growth over the coming years. Various types of insect growth regulators (IGRs) such as anti-juvenile hormone agents are also used along with attractants in the physical and mechanical control methods, such as termite bait systems and barriers.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=90550477

The termite control market, by application, was dominated by the commercial & industrial sectors. The high demand from the commercial & industrial sectors is attributed to the strict regulatory requirements to fulfil the need for keeping the threat of termites under control. Audits are mandatory by many government authorities for certifications such as ISO 9001 and ISO 22000 in commercial and industrial organizations, particularly in the food service and pharmaceutical industries. These certifications have a mandatory clause of termite control to be carried out yearly, half-yearly, or on a quarterly basis; companies that do not comply with these mandates are faced with penalties and shutdowns. Hence, the demand for termite control services is increasing globally.

North America dominated the global termite control market in 2016. According to a global property guide article dated September 2016, the housing market in North America is witnessing an upward trend. This has led to an increased demand for termite control services in the region, as these houses are generally made of wood. Additionally, leading companies in North America are engaged in launching new products and expanding their presence across the globe to sustain their lead in the market.

The global termite control market is highly concentrated, with few of the multinational companies, accounting for a major share in the market in 2016. The market in developed countries has become saturated, and the demand is mainly accounted for by the developing countries. The key players identified have a strong presence in the global termite control market. The leading players in the market include BASF SE (Germany), Syngenta AG (Switzerland), Dow Chemical Company (US), Sumitomo Chemicals (Japan), and FMC Corporation (US).

Request for Customization:

Target Audience:

- Termiticide manufacturers, suppliers, and formulators

- Professional pest control service providers

- Termiticide traders, distributors, importers, exporters, and suppliers

- Public health contractors

- Commercial research & development (R&D) institutions and financial institutions

- Trade associations and industry bodies

- Government health authorities and regulatory bodies such as World Health Organization (WHO), Environmental Protection Agency (EPA), and Pest Management Regulatory Agency (PMRA)