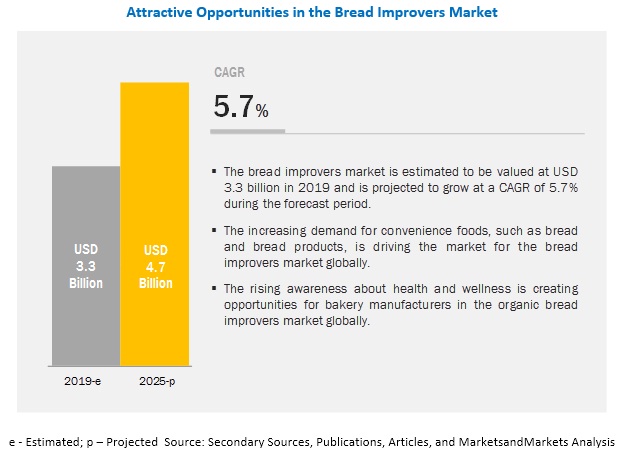

According to MarketsandMarkets, the global bread improvers market is estimated to be valued at USD 3.3 billion in 2019 and is projected to reach USD 4.7 billion by 2025, recording a CAGR of 5.7%, in terms of value. The rising consumption of bread and bread products has led to the growth of bread improvers market. Also, the increasing awareness about health and food safety is fueling the demand for whole wheat and multigrain breads, which is helping market growth. Bakery manufacturers are innovating their products to meet the changing functional requirements of the consumers. All these factors are contributing to the growth of bread improvers market.

Report Objectives:

- To describe and forecast the bread improvers market, in terms of type, form, application, ingredient, and region

- To describe and forecast the bread improvers market, in terms of value, by region–North America, Europe, Asia Pacific, South America and the Rest of the World—along with their respective countries

- To provide detailed information regarding the major factors influencing market growth (drivers, restraints, opportunities, and challenges)

- To strategically analyze micro-markets with respect to individual growth trends, prospects, and contributions to the overall market

- To study the complete value chain of the bread improvers market

- To analyze opportunities in the market for stakeholders by identifying the high-growth segments of the bread improvers market

By ingredient, the emulsifiers segment is projected to account for the largest share in the bread improvers market during the forecast period

The emulsifiers segment, by ingredient, is projected to dominate the market during the forecast period. Emulsifiers are used in the manufacturing of bakery products to reduce the fat content in baked goods. Some of the emulsifiers used in the production of bread improvers are DATEM, diglycerides, lecithin, and monoglycerides. Emulsifiers are easily available at lower costs. Also, emulsifiers, such as lecithin, are being used for the manufacturing of clean-label products, which substantiates the increased dominance of the emulsifiers segment.

Download PDF Brochure:

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=29099697

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=29099697

By application, the bread segment accounted for the largest market size in the bread improvers market during the forecast period

The demand for bread improvers is increasing significantly due to the rising demand for different forms of bread. Bread is a prominent food globally, and in many regions, its market has matured. Manufacturers are coming up with fortified and flavored breads for these matured markets. In addition, emerging regions such as Asia Pacific are witnessing a rise in demand for on-the-go breakfast products, which is also driving the market of bread. This is ultimately contributing to the growth of the bread improvers market.

The Asia Pacific region is projected to witness the fastest growth during the forecast period

The bread improvers market in Asia Pacific is projected to witness the highest growth due to the increasing demand for convenience foods due to the busy lifestyles of consumers. There is increasing consumption of on-the-go and ready-to-eat breakfast meals, as a result of urbanization, hectic lifestyles, and high disposable income. This trend is expected to fuel the growth of bread improvers in the region, as the increasing amount of bread and bread products are expected to be consumed. This region also offers scope for product innovation in the bakery industry, as consumers have varied tastes and preferences and look for a variety in rolls and breads. This has offered manufacturers the opportunity to expand their product portfolios. Such market potential is anticipated to impact the bread improvers market positively during the forecast period.

This report includes a study on the marketing and development strategies, along with the product portfolios of the leading companies. It consists of profiles of leading companies such as Archer Daniels Midland Company (US), Associated British Foods plc (US), Ireks GmbH (Germany), Oriental Yeast Co., Ltd. (Japan), Fazer Group (Finland), Corbion N.V. (Netherlands), Nutrex N.V. (Belgium), Group Soufflet (France), Puratos Group (Belgium), Lallemand Inc. (Canada), Pak Group (US), InVivo (France), Bakels Worldwide, (Switzerland), Lesaffre (France), and John Watson-Inc (US).

To speak to our analyst for a discussion on the above findings, click Speak to Analyst