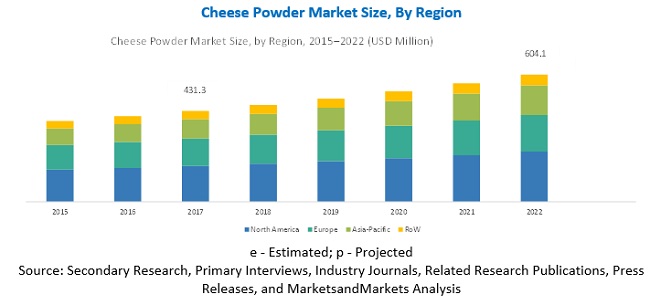

The report "Cheese Powder Market by Type (Cheddar, Mozzarella, Parmesan, American, and Blue), Application (Bakery & Confectionery, Sweet & Savory Snacks, Sauces, Dressings, Dips & Condiments, and Ready Meals), and Region – Global Forecast to 2022", The cheese powder market is projected to grow at a CAGR of 6.82% from 2016 to 2022, to reach USD 604.1 Million by 2022.

The increasing demand for convenience foods is one of the major drivers for the cheese powder market. The major industrial users of cheese powders include producers of snacks, soups, sauces, frozen products, and ready-to-eat meals. Snacks is the major application of cheese powder due to its easy handling and longer shelf life. Its usage in dry snacks has been largely contributing to the growth of the market.

Download PDF Brochure:

Rising awareness regarding the ill-health effects of cheese

The rising consumer awareness about the ill-health effects of cheese poses a great challenge to the growth of the global cheese powder market. Obesity, high cholesterol levels, and heart diseases are the major conditions associated with the consumption of processed cheese. Furthermore, studies suggest that the consumption of cheddar cheese may pose an increased risk of breast cancer by increasing the production of galactose from lactose.

The cheddar cheese segment is projected to dominate the market during the forecast period

The demand for cheddar cheese powder is mainly driven by its application as a flavorant in various convenience food products such as snacks, bakery products, confectioneries, ready meals, sauces, dressings, dips, and condiments. The demand for cheese powder is driven by increase in the fast food industry and the innovations in product offerings by cheese powder manufacturers.

Increased consumption of cheese powder in ready meals, owing to busy lifestyles and changing dietary habits

The market for application of cheese powder is led by ready meals, in terms of growth rate. The demand for ready meals is projected to increase due to the busy lifestyles and changing dietary habits of the consumers associated with it. Furthermore, cheese powder has a longer shelf life which makes it a preferred option for the packaged food manufacturers.

Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=103908380

Asia Pacific is projected to be the fastest-growing region in the cheese powder market, in terms of value.

Asia-Pacific is projected to be the fastest-growing region in the global cheese powder market due to rapidly growing fast-food industry and changing dietary preferences of people in countries like China, India, and Australia that has led to an increased demand for cheese powder in the region. Furthermore, key players in this market are focusing to establish their position in these developing nations.

This report includes a study of marketing and development strategies, along with the product portfolios of leading companies. It includes the profiles of leading companies such as Lactosan A/S (Denmark), Land O’Lakes, Inc. (U.S.), Kerry Group Plc (Ireland), and Kraft Foods Group, Inc. (U.S.).