The report "Pesticide Residue Testing Market by Type (Herbicides, Insecticides, Fungicides), Technology (LC-MS/GC-MS, HPLC, Gas Chromatography), Class (Organochlorines, Organophosphates, Organonitrogens & Carbamates), Food Tested, and Region - Global Forecast to 2022", The pesticide residue testing market is projected to reach USD 1.63 Billion by 2022, at a CAGR of 7.0% from 2016 to 2022. The market is driven by the implementation of food regulatory laws, advancements in testing technologies, global movement of organic revolution, and international trade of food materials.

The objectives of the Pesticide Residue Testing Market report:

- To define, segment, and project the size of the global market on the basis of type, technology, food tested, and class

- To understand the structure of the market for pesticide residue testing by identifying its various subsegments

- To provide detailed information about the key factors influencing the growth of the market (drivers, restraints, opportunities, and industry-specific challenges)

- To strategically analyze micromarkets with respect to individual growth trends, future prospects, and their contribution to the total market

- To analyze the opportunities in the market for stakeholders and provide a competitive landscape of market trends

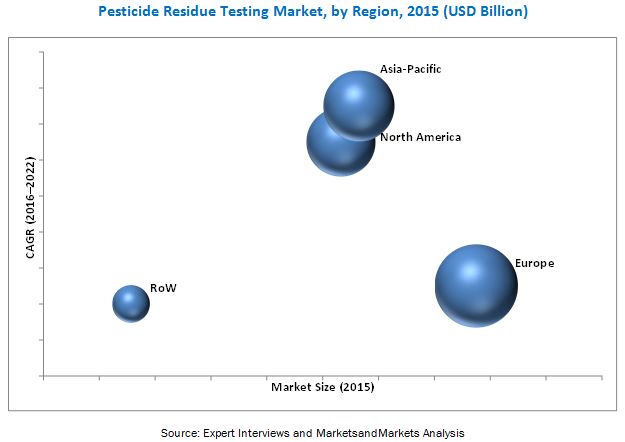

- To project the size of the market and its submarkets, in terms of value, with respect to four regions (along with their respective key countries): North America, Europe, Asia-Pacific, and the Rest of the World (RoW)

Download PDF Brochure:

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=195216043

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=195216043

The global market, on the basis of technology, is segmented into LC-MS/GC-MS, HPLC, gas chromatography, and others such as immunoassay and other test kits. The LC-MS/GC-MS and HPLC are the two largest technologies used in the pesticide residue testing. LC-MS, which is a combination of liquid chromatography with mass spectrometry, is a powerful technique that has very high sensitivity, making it useful in many applications. HPLC is the second largest technology used to detect residues in the food. The increase in the convenience and ease of use of chromatography devices is increasing the adoption rate of chromatography instruments in food safety testing.

The global market, based on class, is categorized into organochlorines, organophosphates, organonitrogens & carbamates, and others which include pyrethroids and fumigants. The organochlorines segment is projected to be the largest and the fastest growing class of pesticide residues in the pesticide residue testing market. Organochlorine pesticides include heptachlor, endosulfan, chlordane, and mirex. These pesticides are applied on fruits & vegetables to interfere with the ion channel receptors in insect neurons. The fruits & vegetables segment, based on food tested, is the fastest growing segment for this market.

Request for Customization:

https://www.marketsandmarkets.com/requestCustomizationNew.asp?id=195216043

https://www.marketsandmarkets.com/requestCustomizationNew.asp?id=195216043

The Asia-Pacific region is projected to be the fastest growing market through 2022 due to the increasing food safety concerns among the consumers and the growing market for processed food. The region is a significant trading partner with the developed regions such as Europe and North America. China is projected to be fastest growing country in the Asia-Pacific region. The country is required to follow stringent regulations imposed by the importing countries for the food safety testing for pesticide residue. As the country is the largest pesticide producer and exporter in the world, increasing instances of pesticide contamination in the air, water bodies, and soil, and pesticide-induced deaths have also become a serious concern which results in an increase in demand for pesticide residue testing.

This report includes a study of marketing and development strategies, along with the product portfolios of leading companies. It includes the profiles of leading companies such as Eurofins Scientific SE (Luxembourg), Bureau Veritas S.A. (France), SGS S.A. (Switzerland), Intertek Group plc (U.K.), and Silliker, Inc. (U.S.). Other players include ALS Limited (Australia), AsureQuality Ltd (New Zealand), SCS Global Services (U.S.), Microbac Laboratories, Inc (U.S.), and Symbio Laboratories (Australia).

Target Audience

- The stakeholders for the report are as follows:

- Pesticide residue testing service providers

- Pesticide residue testing laboratories

- Food processors

- Food manufacturers

- Government and research organizations

- Trade associations and industry bodies