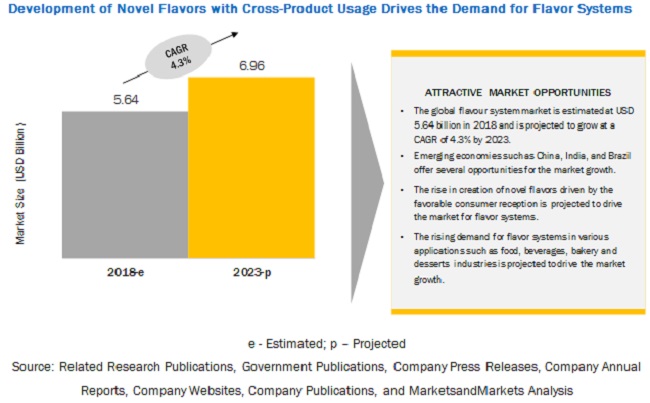

The report "Flavor Systems Market by Type (Brown, Dairy, Herbs & Botanicals, Fruits & Vegetables), Application (Beverages, Savories & Snacks, Bakery & Confectionery Products, Dairy & Frozen Desserts), Source, Form, and Region - Global Forecast to 2023", is estimated to be valued at USD 5.64 billion in 2018 and is projected to reach a value of USD 6.96 billion by 2023, growing at a CAGR of 4.3% during the forecast period. Factors such as the Creation of novel flavors driven by favorable consumer reception and cross product usage of flavors are driving the growth of this market.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=237716072

The brown segment by type, is

estimated to account for a larger market share, in 2018

The brown segment dominated the

market for flavor systems. This is attributed to the fact that brown flavors

are the most commonly used flavor variant and used across a number of

applications. There has been an increase in the number of areas such as

beverages, and dairy, in which brown finds applications. Due to these factors,

the market is projected to witness significant growth.

The nature-identical segment by

source is estimated to be the fastest growing segment in the flavor systems

market, during the forecast period

They are chemically identical to

substances that are naturally present in materials of plant and animal origins.

Although nature-identical substances are formulated in a laboratory, the human

body cannot distinguish between natural and nature-identical substances.

Therefore, nature-identical flavoring substances, having molecular structures

that mimic the chemical structures of natural ingredients, enjoy a higher

preference among consumers, especially because these substances have no

artificial flavoring. Thus, this segment is projected to witness fastest growth

in coming years.

The beverages segment, by

application, is estimated to account for the largest market share, by value, in

2018

The market for beverages held the

largest share in 2017 in the flavor systems market and is also projected to be

the fastest-growing segment during the forecast period. The use of various

types of flavors in this application is largely attributed to the introduction

and combination of different flavors to create an elegant and aromatic taste.

The liquid segment, by form, is

estimated to account for the largest market share, in 2018 and is projected to

be the fastest growing segment during the forecast period

Liquid form of flavoring systems is

made available in oil as well as water-based textures. A common form of using

liquid flavor systems is via flavor microemulsions. Flavor microemulsions which

find its usage in clear beverages and other consumer products, are defined as a

clear, thermodynamically stable dispersion of two immiscible

liquids—oil-in-water or water-in-oil. Flavor enhancers can easily be mixed in

various application and therefor has higher demand.

Mass customization of flavor systems

has created opportunities for manufacturers

Mass customization majorly refers to

the entire process of providing a wide variety of goods or services that are

then modified and customized to suit major consumer group requirements. Mass

customization is mostly used as a marketing and manufacturing technique wherein

the products offered ensure a certain level of flexibility and personalization.

This technique also ensures manufacturers with low unit costs, thereby

improving operational efficiencies. The technique of mass customization has

gained a high degree of traction in recent times due to consumers being

increasingly inclined toward highly customized options. While consumers earlier

focused on efficient and reasonable products, they are willing a slightly

premium price for customized or quality products today. Owing to such factors,

opportunities pertaining to customized solutions have started to gain pace and

significance in the market.

Request for

Customization:

https://www.marketsandmarkets.com/requestCustomizationNew.asp?id=237716072

Europe is projected to grow at the

highest CAGR of 5.0% during the forecast period

In Europe, growing consumption of

bakery & confectionery products and savories & snack products, and the

demand for their product variety has resulted in intensifying demand for flavor

systems in these food products. Moreover, several innovations in food &

beverages industry happening in this region that also accommodate flavor

systems have been driving the growth of flavor systems market in this region.

This report includes a study on the

marketing and development strategies, along with a study on the product

portfolios of the leading companies operating in the flavor systems market.

Givaudan (Switzerland), International Flavors & Fragrances (IFF) (US),

Firmenich (Switzerland), Symrise (Germany), and Mane SA (France) are the

leading players in the flavor systems market. Some of the other players in the

flavor systems market include Frutarom (Israel), Sensient (US), Takasago

(Japan), Robertet (France), Tate & Lyle (France), T. Hasegawa (Japan),

Kerry Group (Ireland).