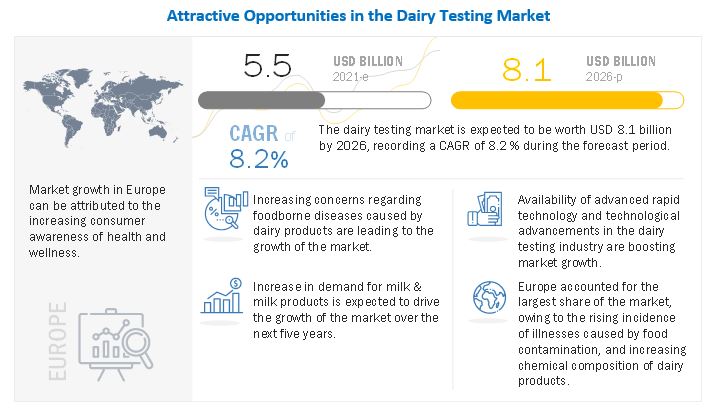

The report "Dairy Testing Market by Type (Safety (Pathogens, Adulterants, Pesticides), Quality), Technology (Traditional, Rapid), Product (Milk & Milk Powder, Cheese, Butter & Spreads, Infant Foods, ICE Cream & Desserts, Yogurt), and by Region - Global Forecast to 2026" The global dairy testing market is estimated to be valued at USD 5.5 billion in 2021 and is projected to reach a value of USD 8.1 billion by 2026, growing at a CAGR of 8.2% during the forecast period. Increase in consumer awareness regarding the safety and quality of food products, stringent regulations imposed by the regulatory bodies, and increase in the global dairy trade, have been driving the global dairy testing market.

Download PDF Brochure @

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=240885146

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=240885146

Impact of Covid-19 on Dairy Testing Market

The COVID-19 pandemic is projected to have a significant impact on the food (dairy) market, as it has highlighted the significance of safe, healthy, and nutritive eating. Food security, food safety, and food sustainability have been considerably affected during the Covid-19 pandemic. The use of e-commerce to order deliveries of groceries and restaurant meals has risen sharply. Restaurant operators with established drive-thru and pick-up operations have fared much better than those without. Consumer behavior related to the food consumed saw sharp shifts, with a higher preference for safety and quality. These have further propelled the manufacturers to assess the safety parameters of their food products to be able to sustain their product values in the market.

Opportunities: Technological advancements in the testing industry

The focus on reducing lead time, sample utilization, cost of testing, and drawbacks associated with several technologies have resulted in the development of new technologies in spectrometry and chromatography. The wide-scale adoption of these technologies provides an opportunity for medium- and small-scale laboratories to expand their service offerings and compete with large market players in the industry, as these technologies offer benefits such as higher sensitivity, accurate results, reliability, multi-contaminant, and non-targeted screening with low turnaround time. The dairy testing market is witnessing several technological innovations with major players offering newer, faster, and more accurate technologies such as LC (Liquid Chromatography), HPLC (High-Performance Liquid Chromatography), and ICP-MS (Inductively Coupled Plasma Mass Spectrometry).

By technology, the rapid technology segment is projected to dominate the dairy testing market during the forecast period.

The rapid technology segment is estimated to dominate the dairy testing market in 2021 and is projected to record higher growth during the forecast period. Rapid technology offers low turnaround time, higher accuracy and sensitivity, and the capacity to test a wide range of contaminants as compared to traditional technology; this is driving the dairy testing market for rapid technology.

Request for Customization @ https://www.marketsandmarkets.com/requestCustomizationNew.asp?id=240885146

The rising demand for dairy testing in the European markets has created opportunities for dairy testing service providers.

The Europe region is the dominant market for dairy testing and is expected to experience the fastest growth only second to Asia-Pacific. The major producers of milk in the EU region are Germany, France, Poland, the Netherlands, Italy, and Spain. Together these countries account for around 70% of the total milk production. Globalization has increased the international trade of milk and dairy products and has had a major impact on global dairy supply. However, the increase in trade has resulted in higher risk of contaminated milk and dairy products reaching dairy producers and processors, and end consumers in distant markets due to instances of cross-contamination, exposure to toxins, microorganisms, and other contaminants. Manufacturers have been using dairy testing services to ensure safety and quality of their products and to comply to the international standards

This report includes a study on the marketing and development strategies, along with the product portfolios of the leading companies operating in the dairy testing market. It includes the profiles of leading companies such as SGS SA (Switzerland), Bureau Veritas (France), Eurofins (Luxembourg), Intertek (UK), TÜV SÜD (Germany), TÜV NORD GROUP (Germany), ALS Limited (Australia), Mérieux NutriSciences (US), Neogen Corporation (US), Romer Labs (Austria), Microbac Laboratories (US), AsureQuality (New Zealand).