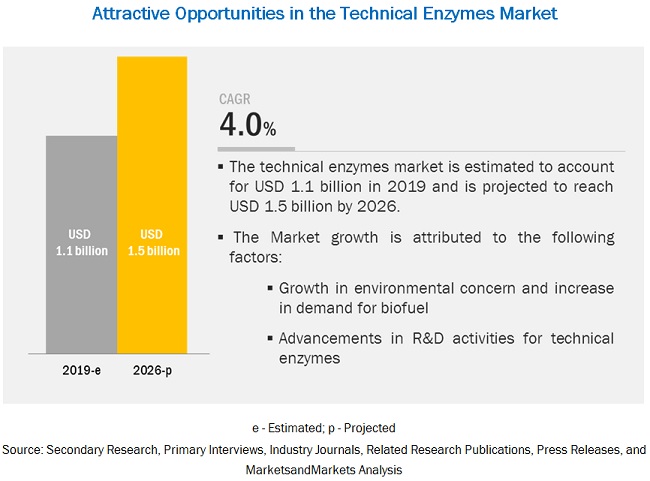

The global technical enzymes market size is projected to grow from USD 1.1 billion in 2019 to USD 1.5 billion by 2026, recording a compound annual growth rate (CAGR) of 4.0% during the forecast period, in terms of value. The increasing trend of environmental concerns in developing countries and advancements of R&D activities for technical enzymes are the major factors that are projected to drive the growth of the technical enzymes market. However, the cost of enzymes usage in various industrial applications remains high during the formulation process of technical enzymes, which is projected to inhibit the growth of the market.

Download PDF Brochure @

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=72989187

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=72989187

Key technical enzymes players include BASF (Germany), DuPont (US), Associated British Foods (UK), Novozymes (Denmark), DSM (Netherlands), Dyadic International (US), Advanced Enzymes Technologies (India), Maps Enzymes (India), Epygen Labs (India), Megazyme (Ireland), Aumgene Biosciences (India), Enzymatic Deinking Technologies (US), Tex Biosciences (India), Denykem (UK), MetGen (Finland), Creative Enzymes (US), Sunson Industry Group (China), Transbiodiesel (Israel), Enzyme Supplies (UK), and Enzyme Solutions (US). New product launches and expansions were the dominant strategies adopted by major players, followed by collaborations. These strategies have helped them to increase their presence in different regions.

Novozymes (Denmark) is a major bio-innovation company providing biological solutions, which involve various applications of enzymes and microbes. The company catered to industries such as household care, food & beverages, bioenergy, agriculture & feed, and technical & pharmaceutical. However, the bioenergy segment of the company delivered strong growth since 2017. The company offers products for bioenergy, which converts plant materials and waste to biofuels. Using these biofuels, the company’s objective is to reduce carbon dioxide emissions by 50%–90% compared with conventional gasoline. For instance, in May 2019, Novozymes (Denmark) has partnered with Alibaba’s 1688 platform to offer industrial biotechnology products in China.

DuPont (US) is a global chemical company that has been focusing on technology-driven innovations in providing products and solutions to various industries. DuPont Nutrition & Biosciences (Denmark) is the subsidiary of DuPont, which offers enzymes under the industrial biosciences. The company has segregated its business segments as animal nutrition, food & beverage, personal care, bioenergy, fabric & home care, textile processing, biomaterials, and microbial controls. The company has been focusing on enhancing its market presence in the Asia Pacific and North American regions. For instance, in February 2019, DuPont Nutrition & Biosciences extended its collaboration with Essential Ingredients (US) to distribute DuPont’s personal care portfolio. Additionally, Essential Ingredients would also distribute the company’s cleaning enzyme solutions in the North American region.

Speak to Analyst @ https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=72989187

The Asia Pacific region projected to grow at the highest CAGR between 2019 and 2026. The increasing demand for technical enzymes in starch and textile & leather industries is projected to create lucrative growth opportunities for manufacturers in the market in the Asia Pacific region. This dominance is majorly due to the change in technological innovations in machinery, synthetic fibers, logistics, and globalization of business. Furthermore, the shift of industrial operations such as textile & leather production from developed nations in North America and Western Europe into the Asia Pacific region over the past decade has boosted the market for technical enzymes.