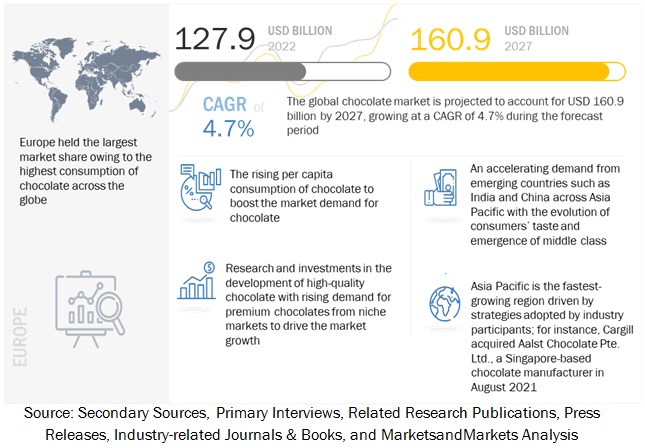

The global agricultural sprayers market is estimated at USD 2.5 billion in 2022. It is projected to reach USD 3.5 billion by 2027, recording a CAGR of 6.8% during the forecast period. With the growing world s population and the decreasing amount of arable land, the focus has shifted towards usage of modern agricultural techniques, like agricultural sprayers, to increase crop productivity. Increasing focus on farm efficiency and productivity, rising production of cereals & grains in Asian countries, and government support toward modern agricultural techniques are some of the major drivers driving the growth of the agricultural sprayers market.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=46851524

The self-propelled segment by type is projected to achieve the highest CAGR growth in the agricultural sprayers market.

Self-propelled sprayers are used to meet the large-scale productivity demand of crops. Although self-propelled sprayers have slightly higher initial costs, its lower application cost contributes to a higher ROI. Self-propelled sprayers can do the same job as pull-type machines for the same or less money, depending on the number of acres covered. A self-propelled sprayer becomes more cost-effective as the acres covered increases.

By capacity, the high-volume sprayers is projected to account for the highest CAGR 6.4% in the agricultural sprayers market.

The most common equipment for applying fertilizer and pesticides is high volume sprayers. The tanks capacity is significantly higher than that of other types of sprayers, which extends the spraying period by reducing the amount of time spent traveling and filling the tank. The benefit of using high volume sprayers is that they last longer and provide the crop with proper penetration and coverage of fertilizers, insecticides, and other chemicals.

The large farm segment by farm size is projected to account for the second largest market share in the agricultural sprayers market over the forecast period.

Farms larger than 200 hectares in size fall within the large farm segment. Considering economies of scale, self-propelled sprayers in agriculture are most suited for large types of farms. A distinguishing agronomic or economic advantage in agriculture is the ability to fully capitalize on planting or weed control opportunities. As a result large farms are able to produce grain yields that are significantly higher. Additionally, the revenue generated by these farms is more than double per unit of land area.

The other crop type segment is projected to observe the highest CAGR of 6.9% in the agricultural sprayers market during the forecast period.

Sprayers are among the most important agricultural tools required for crop production. Pest and weed infestation are serious issue in floriculture crops, turf, and ornamental plants, and there is a crucial need to prevent the infestations in fields which has led to increase in demand for agricultural sprayers. A major factor for the growth of agricultural sprayers in the other segment is the increasing application of plant regulators and herbicides in turf and ornamentals.

Speak to Analyst @

https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=46851524

Asia Pacific is projected to achieve the Highest CAGR of 6.8% in the agricultural sprayers market.

India, Australia, Japan, and other nations in the Asia-Pacific region are traditional agricultural countries. Traditional agriculture relied primarily on human labor and draught animals. The majority of modern agricultural operations depends on machinery, particularly fast, potent tractors, combines, and implements. Tractors with mounted and trailed implements such as sprayers allow the mechanization of many agricultural operations. Due to the increasing average farm size, larger, more upgraded sprayers are being used to meet farm needs rather than older, less efficient ones. This will drive market growth in the Asia-Pacific region during the forecasted period.

The key players in this market include John Deere (US), CNH Industrial NV (UK), Kubota Corporation (Japan), Mahindra & Mahindra Ltd (India), STIHL AG (Germany), AGCO Corporation (US), YAMAHA Motor Corporation (Japan), Bucher Industries AG (Switzerland), DJI (China), Exel Industries (France), Amazonen Werke (Germany), B group Spa (Italy), Case IH (US), HD Hudson Manufacturing Co (US), and Buhler Industries Inc (Canada). These players in this market are focusing on increasing their presence through agreements and collaborations. These companies have a strong presence in North America, Asia Pacific and Europe. They also have manufacturing facilities along with strong distribution networks across these regions.