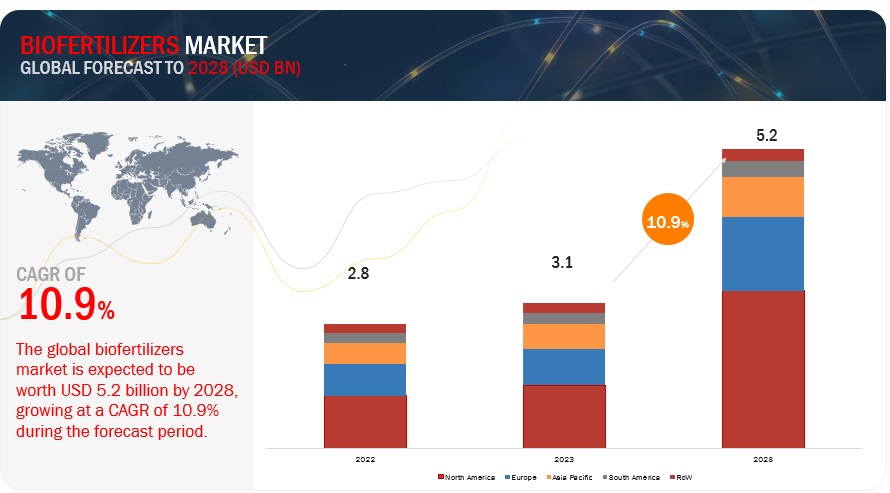

According to a research report "Biofertilizers Market by Type (Nitrogen-Fixing, Phosphate Solubilizing & Mobilizing, Potassium Solubilizing & Mobilizing), Mode of Application (Soil Treatment, Seed Treatment), Form, Crop Type and Region - Global Forecast to 2028" published by MarketsandMarkets, the biofertilizers market is estimated at USD 3.1 billion in 2023 and is projected to reach USD 5.2 billion by 2028, at a CAGR of 10.9% from 2023 to 2028. The market was valued to be 2.8 billion in 2022. Due to the rise in the modern agriculture techniques, precision farming and protected agriculture the global biofertilizers market is projected to grow at robust growth rate. Increasing demand for packaged organic and sustainably sourced food products, especially in urban areas, is further fueling the growth of the market.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=856

Phosphate solubilizing and mobilizing biofertilizers is estimated to be the fastest segment during the forecast period.

Phosphorus is considered as the most essential element for higher crop productivity. Phosphorous helps into the better growth of crops which helps in enhancing the quality and yield of plants. It is also responsible for improving the root growth, improving seed and flower formations, and makes the plants resistant to the various pests and diseases. Better results are seen in the crops such as sugarcane, rice, fruits, and vegetables etc. These are also being utilized in the modern agricultural methods such as Hydroponics, Aquaponics and protected cultivation. These are the factors which are considered to drive the market for the phosphate solubilizing and mobilizing biofertiilizers.

Pulses and oilseeds segment is projected as the fastest growing segment during the research period.

Pulses and oilseeds is the fastest growing segment during the forecasted period. This is due to the increase in the importance of the pulses in international trade. Pulses also contribute significantly to financial advantages by accounting for a big part of exports. Crops like chickpeas and pigeon peas sometimes require a lot of soil nutrients to develop properly. Rhizobium inoculation is frequently advised to boost nitrogen availability from the soil. Rhizobium and Azotobacter are usually suited for producing pulses and oilseeds. These are the factors that are considered to propel the growth of biofertilizers market.

Seed treatment is estimated to be the fastest-growing segment during the review period.

Seed treatment aids in the encapsulation of small amounts of functional microbes, allowing the plant to deliver nitrogen for the roots to absorb nutrients. Seed treatment for nitrogen fixation is widely used for legume seeds. This process is less expensive and simpler than soil treatment since it involves less work to combine the seeds with biofertilizers. Moreover, seed treatment raises agricultural yields by 20% to 30%, increasing farmers' profit margins with the same crop output. The benefits of seed treatment include better crop quality, enhanced plant stress tolerance, and improved water and nutrient absorption. These are the factors which are driving the growth of the segment.

Make an Inquiry @ https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=856

Europe is estimated to be the fastest growing region during the study period.

Europe is the fastest growing region in biofertilizers market. This is due to increase in the use of technologies and machineries in agricultural sector. The expansion of the agricultural industry in this area has made it possible for it to be a major producer and exporter of important agricultural goods. The region's market for biofertilizers has expanded significantly as a result of a developing economy and customer demand. Europe is one of the leading consumers of fertilizers and hence it is projected to foster at higher rate in biofertilizers market.

Eminent players operating in the biofertilizers market are Novozymes (Denmark), UPL (India), Chr. Hansen Holding A/S (Denmark), Syngenta (Switzerland), IPL Biologicals Limited (India), T.Stanes and Company Limited (India), Lallemand Inc (Canada), Rizobacter Argentina S.A. (Argentina), Vegalab SA (Switzerland), and Kiwa Bio-tech Product Group Cooperation (China).