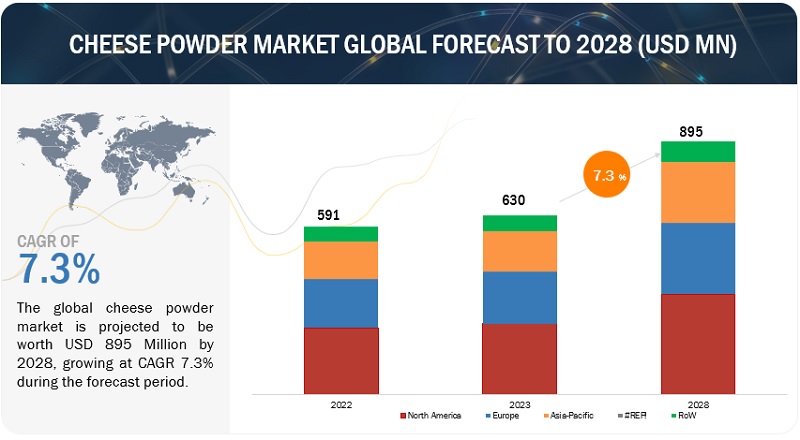

According to MarketsandMarkets, the cheese powder market size is projected to reach USD 895 million by 2028 from USD 630 million by 2023, at a CAGR of 7.3% during the forecast period in terms of value. The demand for cheese powder is expected to grow owing to the growth of the fast-food industry, globally. The changing dietary preferences of people have led to a significant rise in the consumption of convenience and fast food worldwide, which in turn is expected to increase the demand for cheese powder.

The modern food landscape has witnessed a significant shift in consumer preferences, with snack foods emerging as a dominant and evolving segment. This transformation can be attributed to changing lifestyles, urbanization, busier routines, and a growing penchant for convenience. Among the plethora of snack options available, there has been a notable surge in the consumption of flavoured popcorn, chips, and other Savory snacks, which have become staple indulgences for people of all ages. The versatility of cheese powder has enabled manufacturers to explore a wide array of creative combinations and fusion Flavors. This flexibility allows snack producers to continually innovate and introduce new taste sensations to captivate ever-evolving consumer palates. As a result, the rising demand for snack foods has been intrinsically linked to the imaginative use of cheese powder, showcasing its capacity to be both a foundational element and a catalyst for culinary ingenuity.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=103908380

Thus, the demand for cheese powder is increasing to fulfill the growing demand for cheese flavorants by giant fast-food chains such as Domino's Pizza, Inc. (US), Pizza Hut of Yum! Brands (US), and Papa John's International, Inc. (US). Changing lifestyles such as increasing dependence on ready-made or ready-to-eat meals due to busier schedules, and increased demand for packaged foods, globally, have increased the demand for fast food products and ultimately fueled the demand for cheese powder products. Furthermore, above-the-line sales promotion activities such as advertisements through television, print media, and the Internet have also increased awareness regarding cheese-based fast-food products among people.

The cheese powder market is highly impacted with the increasing size of the convenience & fast-food industry and innovative offerings by cheese powder manufacturers. The growth rate of the fast-food industry is significant owing to the changing lifestyles of people around the globe. The U.S. is the dominant market in the fast-food industry and this trend is expected to continue. The emerging economies of the Asia-Pacific region are the major markets for cheese powders and are increasingly contributing to their demand, owing to the rising disposable income, rapidly increasing population, and an increase in the demand for processed foods in these countries.

The widespread impact of Western cuisines on developing regions such as Asia-Pacific and Latin America has led to a tremendous increase in demand for cheese-based fast-food products. Moreover, constant innovations offer investment opportunities to cheese powder manufacturers. On the other hand, rising awareness about the ill-health effects of cheese such as obesity, high cholesterol levels, and heart problems, and stringent government regulations for labeling cheese-based products act as challenges to the cheese powder market.

Make an Inquiry: https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=103908380

The Asia Pacific region is projected to be the fastest growing in the global cheese powder market. Presently, most developing nations such as China, India, Indonesia, and Malaysia are dependent on exports from North America and Europe for cheese powder. Countries such as Australia and New Zealand produce cheese powder on a large scale.

India and Australia are the largest producers of milk in the region, wherein the socio-economic conditions of these countries offer growth opportunities to cheese powder manufacturers. Key players in the market are focusing on establishing their position in developing nations and are strengthening their distribution networks through mergers & acquisitions, partnerships, joint ventures, and collaborations.

The demand for cheese powder in the Asia Pacific region is driven by changing food preferences, increasing demand for convenient and processed foods, and the popularity of Western-style cuisines.

Request for Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=103908380

Land O'Lakes, Inc. (US), Kerry Group Plc (Ireland), Fonterra Co-operative Group Limited (New Zealand), Archer Daniels Midland (US), and Lactosan A/S (Denmark) are among the key players in the global cheese powder market. These players in this market are focusing on increasing their presence through partnership and collaborations. These companies have a strong presence in North America, Asia Pacific and Europe.