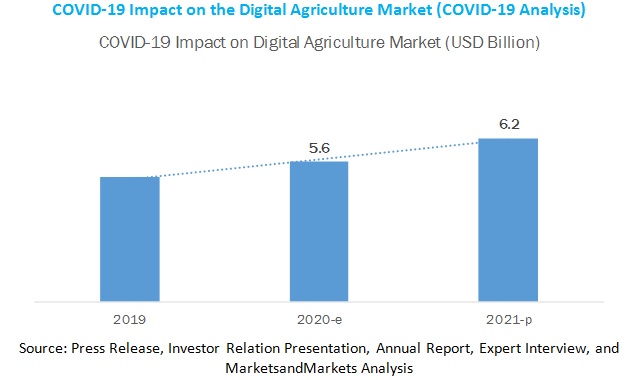

The report "COVID-19 Impact on Digital Agriculture Market by Smart Farming Systems (Livestock Monitoring, Yield Monitoring, Crop Scouting, Field Mapping, Real-Time Safety Testing, and Climate Smart), and Region - Global Forecast to 2021", Post COVID-19, the global digital agriculture market size is estimated to grow from USD 5.6 billion in 2020 and is projected to reach USD 6.2 billion by 2021, recording a CAGR of 9.9%.

Download PDF Brochure:

“Precision farming is the most attractive end-user industry in the digital agriculture market.”

The precision farming market is likely to increase in the long term after the COVID-19 outbreak, as precision farming makes it possible to monitor the state of the crops while not being physically present through the usage of automation, minimizing the need to contact other people, which is crucial during these times. This farming is an approach where inputs are utilized in precise amounts to get increased average yields, compared to traditional cultivation techniques. However, in the short term, COVID-19 would affect the market and the growth of the market would be relatively slower in the first and second quarters of the year 2020 due to economic slowdown and inflation.

These practices save time and costs: reduce fertilizer and chemical application costs, reduce pollution through less use of chemicals. Also, they help in monitoring the soil and plant physiochemical conditions: by placing sensors to measure parameters such as electrical conductivity, nitrates, temperature, evapotranspiration, radiation, and leaf and soil moisture, so that the optimal conditions required for plant growth can be achieved. These factors help to obtain a greater output with limited labor force during this pandemic situation where there is a shortage of labor and thus would help in a regular supply of food, thereby ensuring food security.

“Farm labor management remains the worst affected market during COVID-19.”

With the COVID-19 outbreak, farm labor management remains worst affected in the digital agriculture industry. The pandemic has a significant negative impact on the livelihoods of millions of workers engaged in export-oriented, labor-intensive agricultural production in developing countries. The pandemic may also have a serious impact on processing due to labor shortages and the temporary cessation of production. For example, according to International Labour Organization (ILO) 2020, Europe’s agricultural sector is facing dramatic labor shortages due to border closures that prevent hundreds of thousands of seasonal workers from reaching farms that rely on their labor during the harvest period. The impact on the sector is expected to be long term. Many major European agricultural producers, including France, Germany, Italy, Spain, and Poland, are particularly vulnerable. According to Coldiretti, the Italian organization representing farmers, over a quarter of the food produced in the country relies on approximately 370,000 regular seasonal migrant workers.

Request for Sample Pages of the Report:

https://www.marketsandmarkets.com/requestsampleNew.asp?id=222616344

https://www.marketsandmarkets.com/requestsampleNew.asp?id=222616344

“Asia Pacific to be the fastest-growing market in digital agriculture market during the forecast period”

The market for digital agriculture, by region, has been segmented into Asia Pacific, Europe, the US, and RoW. The Asia Pacific segment accounted for the fastest-growing market in 2021, by value, in the digital agriculture market. Asia Pacific comprises the most populated countries such as China and India, with increasing demand for agricultural products. These countries are also the most two of the most affected countries during COVID-19. The government policies supporting the digitization of farm processes and the need for efficient usage of natural resources, and decreasing availability of migrant labor are expected to increase the adoption of digital agriculture techniques.

Some of the major players in the market are DTN (US), Farmers Edge (Canada), Taranis (Israel), Eurofins (Luxembourg), and AgriWebb (Australia). DTN specializes in subscription-based services for the analysis and delivery of real-time weather, agricultural, energy, and commodity market information. The company mainly operates through four business segments, namely, agriculture, energy, weather, and financial analytics. The company offers different smart farming systems through the agriculture segment. Its agriculture segment provides an analysis of commodity markets; hyper-local weather and disease insights to guide planting, growing and harvesting operations to farmers and agribusinesses; and a real-time pulse on the industry so they are aware of the trends and how they may affect their operations