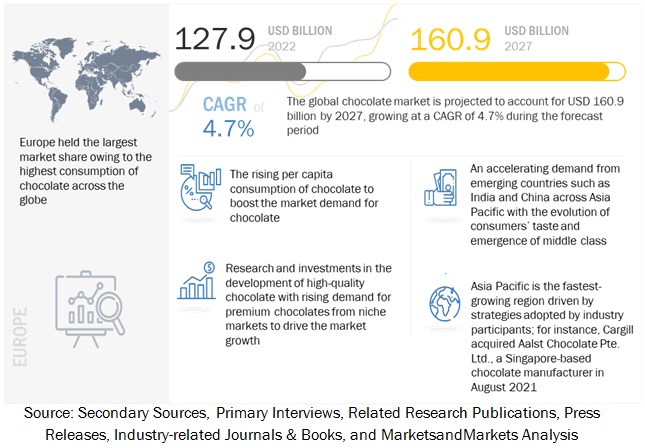

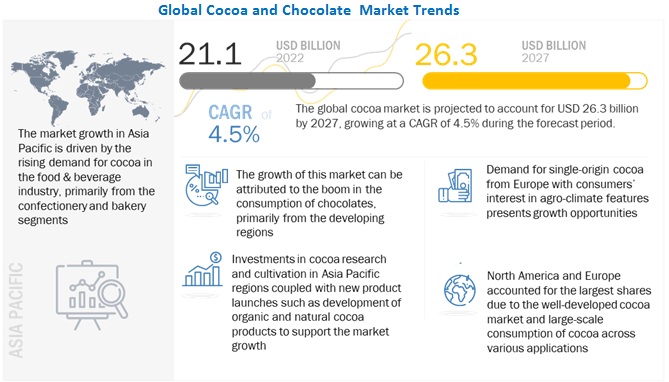

According to a research report "Cocoa and Chocolate Market by Type (Dark Chocolate, Milk Chocolate, Filled Chocolate, White Chocolate), Application (Food & Beverage, Cosmetics, Pharmaceuticals), Nature (Conventional, Organic), Distribution and Region - Global Forecast to 2027" published by MarketsandMarkets, the global cocoa market is projected to reach USD 26.3 billion by 2027, growing at a CAGR of 4.5% from 2022 to 2027. The global chocolate market is projected to reach USD 160.9 billion by 2027, growing at a CAGR of 4.7% from 2022 to 2027.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=226179290

With the growing awareness about health, an increasing number of consumers are prioritizing their health and following specific diets with specific needs. This propels the demand for dark chocolate with high cocoa and less sugar. Cocoa is the major raw material required to manufacture chocolate. The slightest turbulence in the cocoa market would lead to price fluctuations. According to the International Cocoa Organization, the world’s largest supplier of cocoa is Africa, which accounts for 72% of the global production of cocoa. Ivory Coast and Ghana are the major countries producing cocoa, but these countries are also facing certain issues such as fair trade discrepancies, environmental issues, spells of government unrest, and reducing labor force as more population is leaving farming as an occupation and opting other professions Therefore, measures such as implementation of National Cocoa Development Plan (NCDP) in the member countries of ICCO are being undertaken to improve the production of cocoa. Initiatives like these gives a promising outlook towards fulfilling the rising demand for cocoa globally. The cocoa & chocolate market players are showing trends of pursuing both organic as well as inorganic strategies for their expansion, consolidation, and sustainability in the market. Developments and new product launches in chocolate and rise in the use of cocoa for cosmetics and pharmaceuticals are driving the market and is leading to an increased demand for cocoa.

High Raw Material Prices

Chocolate prices are highly dependent on raw materials. Cocoa and sugar are the most important raw materials in chocolate manufacturing and constitute over 80% of the raw material cost for chocolate production. Hence, the rising cost of raw material will impact the market for chocolate. According to the International Cocoa Organization, the world largest supplier of cocoa is Africa, which accounts for 72% of the global production of cocoa. Ivory Coast and Ghana are the major countries producing cocoa, but these countries are also facing certain issues such as fair trade discrepancies, environmental issues, spells of government unrest, and reducing labor force as more population is leaving farming as an occupation and opting other professions.

Seasonal and Festive-related Sales

Chocolate is considered a traditional gift on special occasions and festivals such as Christmas, Easter, Halloween, and Valentine’s Day in American and European countries, a trend which is now adopted in some Asian countries such as India, China, and Japan. Chocolate sales shoot up during festive seasons. Keeping this seasonal effect of sales in mind, companies trying to venture into developing economies, such as India and China, are focusing on specialty products for traditional festivals such as the Chinese New Year, Raksha Bandhan, and Diwali in India.

Currently, the seasonal and festive sales of chocolate products highly impact the market as a large portion of chocolate products are consumed in this segment. Depending on the situation, they are produced in a variety of shapes, sizes, colors, and product materials. Thus, this high demand for chocolates and its products during festivals would enhance the market for cocoa and chocolate.

Make an Inquiry @ https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=226179290

North America dominated the Cocoa and chocolate market, and is projected to grow with a CAGR of 4.43% during the forecast period (2022 - 2027)

The key players in the North American Cocoa and chocolate market include Mondelez international (US), Blommer chocolate (US), Hershey (US) and Mars Inc. (US). The rising demand for chocolate in North America enhances the growth of cocoa simultaneously in the region as it is the key raw material used in the production of chocolate. Moreover, the increasing demand for chocolate among consumers triggers the demand for cocoa butter as it provides the chocolate with its melt-in-the-mouth texture.

The U.S. accounted for the highest chocolate consumption and production in the North American region. In Canada, chocolate is becoming more expensive due to the rising cost of raw materials, particularly sugar but the rising popularity of giving chocolates as gifts, Canada is likely to see a significant increase in the acceptability of pricey chocolates in the upcoming years. The Mexican chocolate market is expanding as a result of rising disposable income, booming foreign investment, and an increase in annual chocolate events like the Mexico Chocolate Expo.