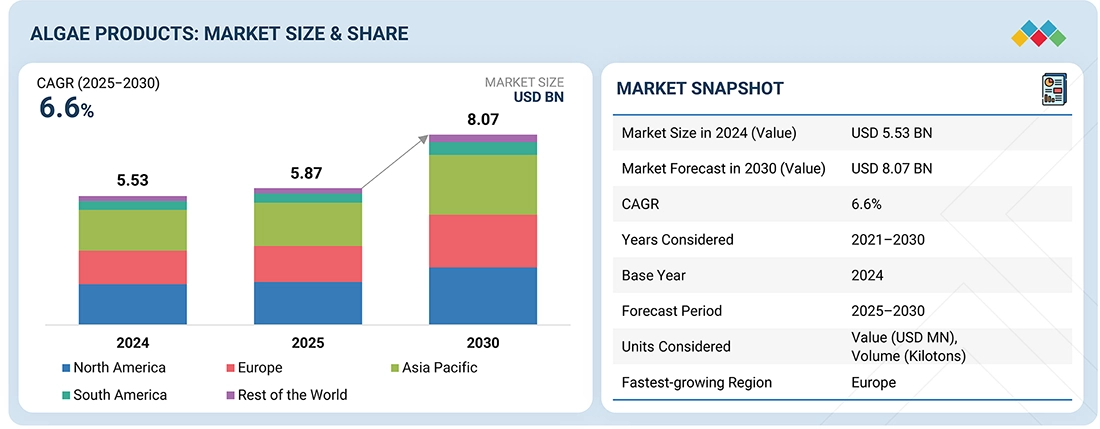

The algae products market is projected to grow from USD 5.87 billion in 2025 to USD 8.07 billion by 2030, registering a CAGR of 6.6% during the forecast period. Steady growth in the market is driven primarily by rising consumer awareness of the health benefits associated with algae. Increasing demand for natural, nutritious, and plant-based food options—alongside preferences for better taste and texture—continues to expand opportunities for algae-derived products. Algae provide valuable nutrients such as omega-3 fatty acids (including DHA) and algal proteins, making them especially attractive to vegetarian and vegan consumers. However, high production costs remain a key challenge, particularly for small-scale companies striving to meet quality standards, which may constrain overall market expansion.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=250538721

Red algae segment expected to grow significantly

Among algae product sources, red algae are poised for notable growth during the forecast period. Species such as Porphyra (47% protein by dry mass) and Palmaria palmata (35% protein by dry mass) are widely consumed in Asian and Western markets due to their high protein content and appealing flavor. Red algae also play a vital ecological role, contributing 40% to 60% of global oxygen production, supporting both terrestrial and aquatic ecosystems. Their commercial value is particularly significant in regions like Japan and the North Atlantic, where they are regarded as essential food sources.

Animal feed to hold a substantial market share

The use of algae in animal feed is rapidly increasing. Algae-based aquafeed has demonstrated both nutritional and economic benefits. Research published in the Journal of the Institute of Food Technology indicates that incorporating specific microalgae species into fish diets can reduce feed costs by up to 50% while enhancing nutrient density. Owing to their rich profiles—containing essential fatty acids, amino acids, carbohydrates, carotenoids, and vitamins—both microalgae and macroalgae have become sustainable and effective nutritional sources for livestock, poultry, and aquaculture.

Asia Pacific to record the highest CAGR

The Asia Pacific region is anticipated to witness the fastest growth in the algae products market during the forecast period. Major contributors include China, Japan, India, and Australia & New Zealand, all of which possess expansive coastlines ideal for cultivating marine and freshwater algae. The region’s tropical climate supports the world’s greatest diversity of algae species, driving production and market adoption.

Rising population levels across Asia Pacific are boosting demand across the food & beverage, pharmaceutical, and personal care sectors, further propelling market growth. Edible seaweeds—such as Kombu (Laminaria japonica), Nori (Porphyra sp.), and Wakame (Undaria pinnatifida)—are widely used in traditional Chinese and Japanese cuisines, including soups, salads, cooked dishes, and sushi.

Beyond food applications, seaweeds play a crucial role in producing hydrocolloids and phycocolloids and are extensively utilized in pharmaceuticals, cosmetics, agriculture, biofuels, and animal feed additives. Given their abundant primary and secondary metabolites, algae-derived products have strong potential in the food and nutraceutical industries, offering substantial growth prospects for the market across the region.

Leading Algae Products Companies:

The report profiles key players such as DSM-Firmenich (Netherlands), BASF (Germany), and Cyanotech Corporation (US), Cargill, Incorporated (US), CP Kelco U.S., Inc. (Tate & Lyle) (US), Corbion (Netherlands), E.I.D.-Parry (India), Kerry Group plc (Ireland), AlgaTech Ltd. (Israel), Algenol Biotech (US), Cellana Inc. (US), Fenchem (China), Fuji Chemical Industries Co., Ltd. (AstaReal Co., Ltd.) (Japan), Algea (Norway), KD Pharma Group SA (Switzerland), and others.