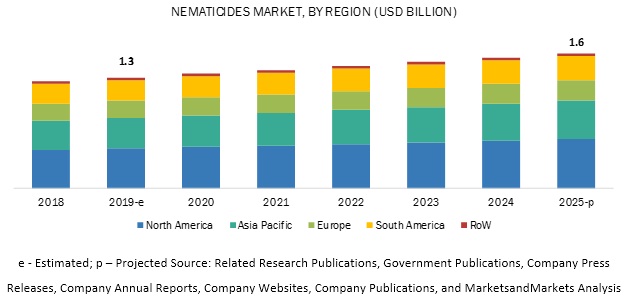

The report "Nematicides Market by Type (Fumigants, Carbamates, Organophosphates, Bionematicides), Mode of Application (Fumigation, Drenching, Soil Dressing, Seed Treatment), Nematode Type (Root Knot, Cyst), Crop Type, Form, and Region - Global Forecast to 2025", The global nematicides market size is estimated to be valued at USD 1.3 billion in 2019 and is expected to reach a value of USD 1.6 billion by 2025, growing at a CAGR of 3.4% during the forecast period. Factors such as the growing demand for biological products and increasing number of product launches catering to the requirement of crop-specific nematodes drive the growth of the market.

Download PDF Brochure:

By type, bionematicides are projected to be the fastest-growing segment in the nematicides market during the forecast period

With the increasing awareness among consumers about the importance of organic foods, the adoption of sustainable agriculture and integrated pest management solutions has increased. This has led to the demand for biocontrol products such as pheromones, biofungicides, biopesticides, and bionematicides. A number of major players in the market such as Marrone Bio Innovations (US) and Valent BioSciences (US) are introducing bionematicide solutions for seed treatment. These factors have paved the way for the high growth rate in the bionematicides market.

By crop type, vegetables are projected to dominate the nematicides market.

The vegetables segment is projected to hold the largest market share owing to the increasing cases of infestation on vegetables such as potatoes, tomatoes, peas, cauliflower, and carrots, by nematode species such as root-knot, lesion, and cyst nematodes. The increasing acreage being brought under vegetable cultivation and the growing demand for organic vegetables drive the growth of this segment.

Speak to Analyst:

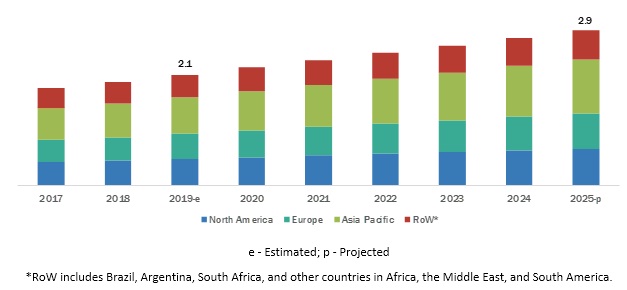

Asia Pacific is projected to grow at the highest CAGR during the forecast period

The market for nematicides is projected to grow at the highest CAGR in the Asia Pacific region owing to the growing nematode infestation in vegetables such as tomatoes, potatoes, carrots, peas, and cauliflower in the major vegetable-growing countries such as China and India. The regulatory scenario in the Asia Pacific region is comparatively more favorable for the launch of nematicides as compared to that of Europe and North America. There is also growing awareness among farmers about the use of bionematicides since the market for organic farming, and sustainable agriculture is growing with more consumers demanding organic fruits & vegetables.

This report includes a study on the marketing and development strategies, along with a study on the product portfolios of the leading companies operating in the nematicides market. It consists of the profiles of leading companies such as Bayer AG (Germany), Syngenta Crop Protection AG (Switzerland), Corteva Agriscience (US), BASF SE (Germany), Adama Agricultural Solutions Ltd (Israel), FMC Corporation (US), Nufarm (Australia), UPL Limited (India), Isagro Group (Italy), Valent USA (US), Chr. Hansen (Denmark), Certis USA LLC (US), Marrone Bio Innovations (US), American Vanguard Corporation (US), Crop IQ Technology (UK), Real IPM Kenya (Kenya), Horizon Group (India), Agri Life (India), and T. Stanes & Company Limited (India).