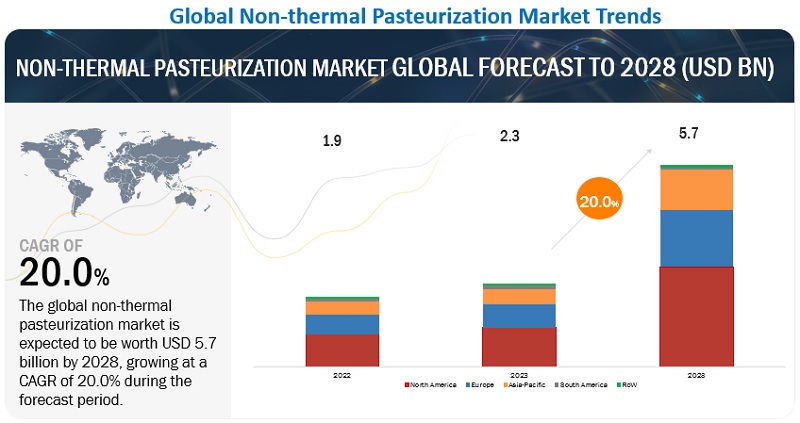

The report “Non-Thermal Pasteurization Market by Techniques (HPP, PEF, MVH, Irradiation, Ultrasonic), Application (Food, Beverages, Pharmaceuticals and Cosmetics), Form (Solid, Liquid), and Region (North America, Europe, Asia Pacific, Row) – Global Forecast to 2023″, The non-thermal pasteurization market is estimated to account for about USD 1.1 billion in 2018 and is projected to reach a value of nearly USD 2.7 billion by 2023, growing at a CAGR of 19.8% from 2018. The non-thermal pasteurization market is increasingly impacted by innovations, as manufacturers are always introducing new equipment ingredients and new variants to meet the increasing demand and cater to the increasing application industries. The global non-thermal pasteurization market is growing significantly in accordance with the commercialization; the increasing size of packaged foods market; and growth in the convenience food sector, which includes products such as frozen foods and ready-to-eat foods; and the growing demand for novel technologies.

Download PDF Brochure:

The beverages segment is estimated to grow at the highest CAGR during the forecast period in the non-thermal pasteurization market, due to increasing acceptance of non-thermal pasteurization techniques in processed fruit & vegetable juices, wine,sugar syrups, beer, milk, and processed coconut water

By application, the beverages segment is estimated to grow at the highest CAGR during the forecast period. Non-thermal processes such as PEF and HPP are increasingly preferred in the beverage industry, as they effectively increase the shelf life of beverages and prevent microbial development. Additionally, colors, flavors, and nutrients can be efficiently preserved with the help of this technology. This technology helps in preserving nutrient, color, and flavor in products; and also enables gentle preservation of beverages at ambient temperature. Thus, these factors are expected to fuel the market growth.

The solid segment is estimated to have a larger market share in the non-thermal pasteurization market during the forecast period

By food form, the solid segment is estimated to have a larger market share in the forecast period. This is due to the usage of non-thermal pasteurization techniques in food products such as cheese, jellies, jam, processed food, meat products, etc. However, various technologies such as HPP and PEF are used to enhance the extraction of several bioactive components and sugars to preserve the food for a longer period of time.

Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=119569840

North America is estimated to dominate the non-thermal pasteurization market in 2018.

North America is estimated to account for the largest market share in the non-thermal pasteurization in 2018. The region is projected to offer huge growth potential to the non-thermal pasteurization market. The use of non-thermal pasteurization techniques are increasing more rapidly in North America due to the demand for extended, safe, refrigerated shelf life; and favorable food preservation legislation. Food safety authorities have approved several non-thermal pasteurization technologies due to their efficiency and minimum effect on the products’ nutritional and textural characteristics. The market for non-thermally pasteurized food & beverage products in North America is also being driven by the demand for health and wellness products.

This report includes a study of marketing and development strategies, along with the product portfolios of the leading companies in the non-thermal pasteurization market. It includes the profiles of the leading companies such as Hiperbaric España (Spain), Avure Technologies (US), BOSCH (Germany), Thyssenkrupp Ag (Germany), and Kobe Steel Ltd (Japan), Chic Freshertech (US), Multivac SEPP Haggenmuller Se & Co. KG (Germany), Stansted Fluid Powder LTD (UK), Dukane Corporation (US), and Universal Pure (US).

Key Questions addressed by the report:

- What are the new trending technologies that non-thermal pasteurization companies are exploring?

- Which are the key players in the market and how intense is the competition?

- What are the upcoming growth trends that non-thermal pasteurization manufacturers are focusing on in the future?

- What are the high-growth opportunities in the non-thermal pasteurization market in each segment?

- What are the key growth strategies adopted by major market players in the non-thermal pasteurization market?