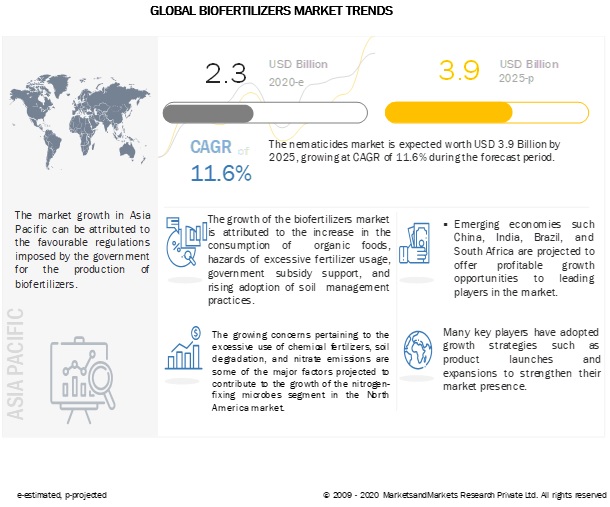

The global nematicides market size is estimated to account for a value of USD 1.3 billion in 2020 and is projected to grow at a CAGR of 3.4% from 2020, to reach a value of USD 1.6 billion by 2025. The growing demand for high-value crops alongside the increasing infestation of nematodes on crops are some of the factors driving the growth in the market.

Driver: Strong demand for high-value crops

High-value agricultural products are generally defined as agricultural products with a high economic value per kilogram (or pound), per hectare, or per calorie, which includes fruits, vegetables, meat, eggs, milk, and fishes. The key factors driving the demand for high-value crops (fruits, vegetables, and plantation crops) are the rise in the income of consumers, rapid urbanization, and the increase in awareness about health benefits associated with fruits & vegetables. Besides, an increase in foreign direct investment (FDI) has led to a surge in the production of high-value crops. The demand for nematodes is mostly found in high-value crops, such as pome fruits, grapes, cotton, tomato, maize, cotton, and other vegetable and ornamental crops, as they improve the crop quality and yield.

Download PDF Brochure:

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=193252005

Challenge: Lack of awareness and low utilization of biologicals

Awareness about biologicals, such as bionematicides among farmers, is very low. Farmers are not aware of the method of use and the cost-effective benefits of these crop protection products. In developing countries, they are not aware of integrated pest management (IPM) solutions. As the market is highly fragmented at the regional level, awareness regarding various brands is low. Despite considerable efforts by agronomists, agricultural universities, companies, and governments across the globe in recent years, the majority of the farmers are unaware of biological products and their benefits in increasing cost-yield sustainability.

By type, bionematicides are projected to be the fastest-growing segment in the nematicides market during the forecast period

With the increasing awareness among consumers about the importance of organic foods, the adoption of sustainable agriculture and integrated pest management solutions has increased. This has led to the demand for biocontrol products such as pheromones, biofungicides, biopesticides, and bionematicides. A number of major players in the market such as Marrone Bio Innovations (US) and Valent BioSciences (US) are introducing bionematicide solutions for seed treatment. These factors have paved the way for the high growth rate in the bionematicides market.

Asia Pacific is projected to grow at the highest CAGR during the forecast period

The market for nematicides is projected to grow at the highest CAGR in the Asia Pacific region owing to the growing nematode infestation in vegetables such as tomatoes, potatoes, carrots, peas, and cauliflower in the major vegetable-growing countries such as China and India. The regulatory scenario in the Asia Pacific region is comparatively more favorable for the launch of nematicides as compared to that of Europe and North America. There is also growing awareness among farmers about the use of bionematicides since the market for organic farming, and sustainable agriculture is growing with more consumers demanding organic fruits & vegetables.

Request for Customization:

https://www.marketsandmarkets.com/requestCustomizationNew.asp?id=193252005

This report includes a study on the marketing and development strategies, along with a study on the product portfolios of the leading companies operating in the nematicides market. It consists of the profiles of leading companies such as Bayer AG (Germany), Syngenta Crop Protection AG (Switzerland), Corteva Agriscience (US), BASF SE (Germany), Adama Agricultural Solutions Ltd (Israel), FMC Corporation (US), Nufarm (Australia), UPL Limited (India), Isagro Group (Italy), Valent USA (US), Chr. Hansen (Denmark), Certis USA LLC (US), Marrone Bio Innovations (US), American Vanguard Corporation (US), Crop IQ Technology (UK), Real IPM Kenya (Kenya), Horizon Group (India), Agri Life (India), and T. Stanes & Company Limited (India).

Recent Developments:

- In August 2018, BASF SE acquired a wide range of businesses and assets from Bayer CropScience (Germany). This acquisition would complement crop protection, biotech, and digital farming activities. This acquisition also allowed the company to enter the non-selective herbicide and nematicide seed treatment markets.

- In October 2018, Corteva Agriscience launched Reklemel, a novel sulfonamide nematicide, which has a unique mode of action against plant-parasitic nematodes. This product is set to be launched by 2021 across North America and Asia Pacific.

- In August 2017, Syngenta Crop Protection AG launched Clariva, the only available biological seed treatment, which controls nematodes on contact in Brazil.