MarketsandMarkets forecasts the pest control market to grow from USD 20.5 billion in 2019 to USD 27.5 billion by 2025, at a CAGR of 5% during the forecast period. The market is primarily driven by chemical pest control techniques due to the high demand for insecticide solutions across the globe by service providers. The increasing awareness of public health has compelled the people to adopt pest control services on a regular basis at residential and commercial levels. The objective of the report is to define, describe, and forecast the pest control market size based on pest type, control method, mode of application, application, and region.

Chemical pesticides, which are toxic or poisonous to the pests, are used for pest control in Asia Pacific. The use of chemical pesticides is widespread due to their relatively low cost, simplicity of application, effectiveness, availability, and stability. These factors, coupled with the growing economic conditions across Asia, encourage the adoption of chemicals to a larger extent. Chemical pesticides are generally fast-acting, which helps minimize their impact on the surrounding environment. Local agencies are adopting new technologies in deploying chemical solutions, including the use of drone-based sprays, to maximize the area to be covered.

Download PDF Brochure:

Insects are the major pest type driving the growth in the Asia Pacific pest control market during the forecast

The climate across the Asia Pacific, especially in Southeast and Western Asia, is conducive for the breeding of many insects. Warmer temperatures are generally the breeding grounds for insects, supporting their faster development and prolonged survival. Termites and mosquitoes are among the major pests in the Asia Pacific region and are expected to fuel the demand for insect pest control products and services during the forecast period. The demand for rodent control in Asia Pacific is also gaining prominence in the wake of the stringent regulations and safety standards in the commercial sector. Rodents are also a major problem in the Asia Pacific market. Countries such as China, India, and Japan are witnessing large-scale rodent infestation in the urban and rural areas. The rodent infestation in the region can be traced to a multitude of factors such as flooding, urban expansion, lack of hygiene conditions and open drains.

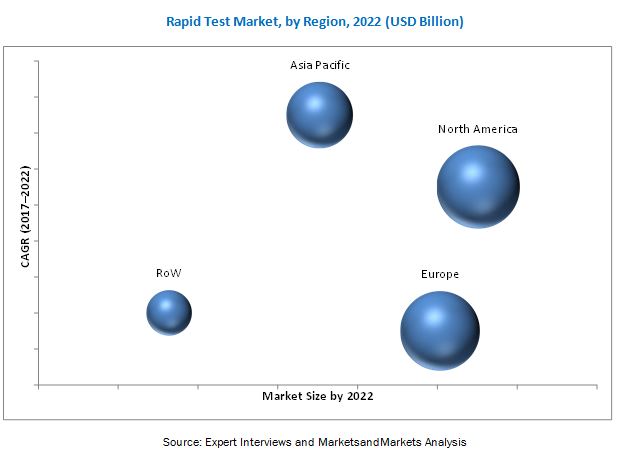

Asia Pacific region is projected to witness the highest growth in the pest control market by 2025.

The Asia Pacific region is among the fastest-growing regions for pest control. The region’s high concentration of urban population and urbanization poses a strong potential for pest control service providers. The effects of climate change and in certain cases, the negligence toward sanitary conditions in urban slums has resulted in multiple disease outbreaks. Improvements in legislation and policies surrounding the requirement of pest control have benefitted pest control service providers in the Asia Pacific region. Additionally, the region has also been susceptible to many pest-borne disease outbreaks in the last two decades. From the last quarter of 2015, there has been a significant number of cases related to Zika virus in the region. Zika virus is a mosquito-transmitted Flavivirus and has been detected in several countries in the Asia Pacific region, which include Thailand, the Philippines, Malaysia, Vietnam, and Indonesia. According to a WHO report (October 2016), the Asia Pacific region is highly likely to continue to report new cases and possibly new outbreaks of Zika virus. Thus, with increasing outbreaks of diseases due to insects, the demand for pest control services is projected to increase in the region.

The key service providers in this market include Terminix (US), Ecolab (US), Atalian Servest (France), Truly Nolen (US), Rollins Inc. (US), Rentokil Initial Plc (UK), and Ecolab (US). The pesticide suppliers in the pest control market include Bayer CropScience (Germany), BASF (Germany), Syngenta AG (Switzerland), Sumitomo Chemicals Co. Ltd. (Japan), Adama (Israel), FMC Corporation (US), DowDuPont (US), PelGar International (UK), and Bell Laboratories (US).

Speak to Analyst:

Recent Developments:

- In March 2019, DowDuPont confirmed the completion of the required clearances for the spin-off for Corteva Agrisciences (US) which would operate as a separate company under the conglomerate.

- In January 2019, Control Solutions Inc. (US), a wholly owned subsidiary of Adama, acquired Bondie Products Inc. (US). The acquisition is expected to benefit CSI through the access of Bondie’s portfolio of pest control products and customer base.

- In October 2018, Bell Laboratories launched Contrac Soft bait 4lb pails, for the US market following the success of its 16lb pails. The new product is expected to ease mobility concerns for service technicians on the field as well as ease inventory management for service providers.