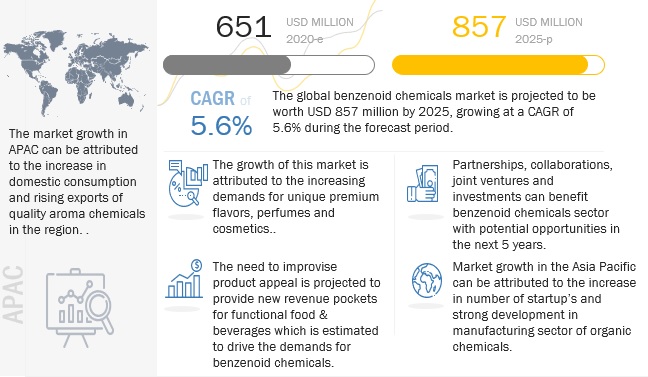

The report "Benzenoid Market by Type (Benzyl Acetate, Benzoate, Chloride, Salicylate, Benzaldehyde, Cinnamyl, Vanillin), Application (Soaps & Detergents, Food & Beverage, Household Products), and Region – Global forecast to 2025", size is estimated to be USD 651 million in 2020 and is projected to reach USD 857 million by 2025, at a CAGR of 5.6% during the forecast period. The market is being strongly driven by soaps & detergents industry, which is witnesses a high demand. With newer premium products coming up in the market and unique fragrance blends, their demand is projected to grow in the market in the near future.

Report Objectives:

- To describe and forecast the benzenoid chemicals market, in terms of type, application, and region

- To describe and forecast the benzenoid chemicals market, in terms of value and volume, by region-Asia Pacific, Europe, North America, South America and Middle East & Africa-along with their respective countries

- To provide detailed information regarding the major factors influencing the market growth (drivers, restraints, opportunities, and challenges)

- To strategically analyze micromarkets with respect to individual growth trends, prospects, and contributions to the overall market

- To study the complete value chain of benzenoid chemicals market.

- To analyze opportunities in the market for stakeholders by identifying the high-growth segments of the benzenoid chemicals market

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=18857610

Benzenoid Chemicals Market Dynamics

Driver: Shifting flavor & fragrance trends and preferences amongst populations globally

The global choices and preferences related to taste and aromas are changing rapidly with changing marketing trends, mindsets and increasing expenditure on lifestyle. As per the 2018 report of “Innova Market Insights” 64% of US consumers state that they “love to discover flavors from other cultures,” Dull flavors are being reinvented and more retail products and restaurants are highlighting ethnic flavors or street flavors. Unique scents and attractive designs have pushed the home fragrance market to its strongest position yet. While over the years traditionally rooted fragrances like jasmine and sandalwood have had a distinct contribution, especially for soaps, a combination of fruity-floral fragrances are now gaining traction with marketers wooing younger consumers.

Restraint: Potential health risks of synthetic chemicals affecting production growth

The genotoxicity and carcinogenicity are the key factors that are taken into consideration to determine the safety of the chemical use. Companies that manufacture perfume or cologne purchase fragrance mixtures from fragrance houses to develop their own proprietary blends. Benzenoids as food additives and fragrance ingredients are regulated as some of them pose potential risks to human health at defined concentrations. Organisation such as US FDA (US Food & Drug Administration), EU Commission, IFRA (International Fragrance Association) set standards and guideline for manufacturers in order to control the possible health risks due to overuse of aroma chemicals in food and fragrance products.

The benzyl benzoate sub-segment is estimated to account for the fastest growth in the by type segment for Benzenoid Chemicals market.

Benzyl benzoate is naturally found in cinnamon, apricots, honey cocoa, cloves, cranberries jasmine, and mushrooms. RIFM (Research Institute for Fragrance Materials) has identified the compounds as a very weak skin sensitizer and IFRA (International Fragrance Association) has set standards for acceptable concentrations of benzyl benzoate that can be used in variety of consumer goods. It serves a supporting role, helping to dissolve and blend together all the different scent substances.

By Application, the soaps & detergents sub-segment is estimated to observe the fastest growth in Benzenoid Chemicals market.

The aroma in soaps and detergent products is bought about by the use many natural and synthetic compounds. The generally used natural compounds include oregano oil, lemon oil, coconut oil, camellia oil, and coffee essential oil amongst others. During the spread of coronavirus pandemic, the significance of soaps and detergents for hygiene purposes grew tremendously giving a boost to the sales of the industry. With organizations such as American Centers for Disease Control and Prevention (CDC), promoting hand hygiene through use of soaps and clean running water the market grew faster in the pandemic time.

Asia Pacific is estimated to be the largest market.

The Asia Pacific region is estimated to account for the largest share of the global benzenoids market in 2020. The rising income, purchasing power, rapid growth of the middle-class population, and consumer demand for processed products present promising prospects for growth and diversification in the region’s benzenoids sector. The European aroma chemicals manufacturers are gradually losing their market share, failing to compete with products from Asia (mainly from China), where labor costs are much lower and the quality control is constantly growing, imitating western technologies. Further, countries such as China, Japan, South Korea, and Indonesia are witnessing significant growth in the cosmetics, beauty, and personal care products markets. These rae expected to drice the growth from benzenoid chemiclas in the region.

Key players in this market include include major players such as BASF (Germany), Firmenich (Switzerland), Emerald Kalama Chemical (US), International Flavors & Fragrances, Inc. (US), Eternis Fine Chemicals (India), Symrise (France), Tennants Fine Chemicals Ltd. (England), Jayshree Aromatics Pvt. Ltd. (India), and Valtris Specialty Chemicals (US. These major players in this market are focusing on increasing their presence through expansions & investments, mergers & acquisitions, partnerships, joint ventures, and agreements. These companies have a strong presence in North America, Asia Pacific and Europe. They also have manufacturing facilities along with strong distribution networks across these regions.