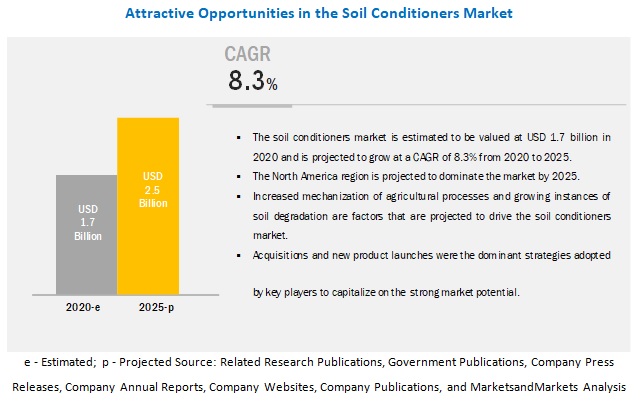

The carotenoids market size is projected to grow from USD 1.5 billion in 2019 to USD 2.0 billion by 2026, recording a compound annual growth rate (CAGR) of 4.2%, in terms of value, during the forecast period. Carotenoids are a group of yellow to red pigments, including the carotenes and the xanthophylls, found particularly in plants, algae, and photosynthetic bacteria and certain animal tissues. The increase in the usage of carotenoids as food colorants and the advancements end-user technologies are the major factors that are projected to drive the growth of the carotenoids market.

Download PDF Brochure:

The lutein segment is projected to grow at the highest rate during the forecast period

The lutein segment, on the basis of type, is projected to grow at the highest CAGR, in terms of value, during the forecast period. Lutein is synthesized by plants and found in some of the major food items, such as egg yolks, carrot, spinach, kale, squash, grapes, and pepper. It is used in both, human nutrition and animal nutrition products. Its wide acceptability due to its ability to treat age-related eye disorders, including cataracts and macular degeneration, is a key factor driving its demand.

By application, the feed segment is estimated to account for the largest market share in 2019 in the carotenoids market

Carotenoids are extensively used in animal nutrition products due to their coloring properties and are incorporated in feed to pigment the egg yolks, broiler skin, fishes, and crustaceans. These also help in increasing the immunity and improving the health of livestock by enhancing the quality of nutrition. The fertility of cattle, swine, and horses can be improved by feeding beta-carotene, whereas astaxanthin and canthaxanthin help in improving the growth of salmons and larval fishes.

Request for Customization:

The Asia Pacific region is projected to grow at the highest CAGR during the forecast period.

The Asia Pacific region is projected to grow at the highest CAGR in the carotenoids market during the forecast period. This is due to the growing application of carotenoids in the health supplements, as they are rich in protein, vitamin, iron, manganese, and antioxidants, which help in preventing cardiovascular diseases and maintaining weight. Asia Pacific offers profitable growth opportunities to manufacturers and suppliers of carotenoids as the processing of carotenoids is cheaper in this region and witnesses a high demand in this region.

The prominent vendors in the carotenoids market include Koninklijke DSM (Netherlands), BASF (Germany), Chr. Hansen (Denmark), Kemin Industries (US), Lycored Limited (Israel), Cyanotech Corporation (US), Fuji Chemical Industry Co Ltd. (Japan), Novus International (US), DDW The Color House (US), Dohler Group (Germany), Allied Biotech Corporation (Taiwan), E.I.D Parry (India), Farbest Brands (US), Excelvite Sdn. Bhd. (Malaysia), AlgaTechnologies Ltd. (Israel), Zhejiang NHU Co. Ltd (China), Dynadis SARL (France), Deinove SAS (France), Vidya Europe SAS (France), and Divi’s Laboratories (India).