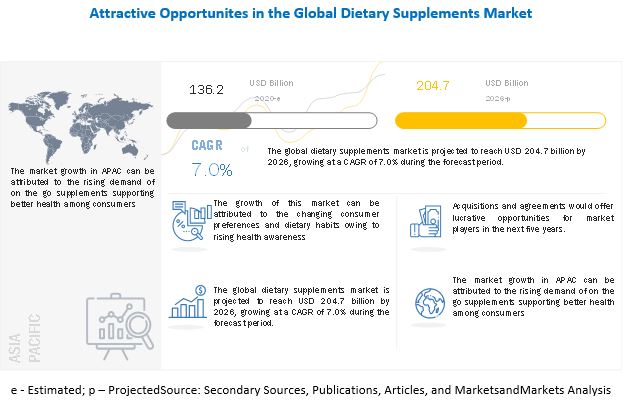

The report "Dietary Supplements Market by Type (Vitamins, Minerals, Botanicals, Amino acids, Enzymes, Probiotics), Function (Additional, Medicinal, Sports Nutrition), Mode of Application (Capsules, Tablets, Liquid), Target Customer and Region - Global Forecast to 2026", According to MarketsandMarkets, the global dietary supplements market size is estimated to be valued at USD 136.2 billion in 2020 and projected to reach USD 204.7 billion by 2026, recording a CAGR of 7.0% during the forecast period.

The demand for dietary supplements is increasing significantly owing to the rising prevalence of chronic diseases and changing dietary habits of consumers. Increasing consumer health awareness and rising disposable income across regions are factors that have encouraged people to shift to dietary supplements. The elderly population is focusing on adapting to nutritional supplements specifically tailored to their needs to maintain their good health and quality of life.

Download PDF Brochure:

https://www.marketsandmarkets.com/Images/dietary-supplements-market8.jpg

https://www.marketsandmarkets.com/Images/dietary-supplements-market8.jpg

Drivers: Aging population to drive the market growth

Consumers across regions have become more health-conscious, which is driving the growth of the dietary supplements market. The aging population of some countries, such as Japan, Italy, Portugal, and Germany, is another key factor that is projected to drive the overall market.

The elderly population is focusing on adapting to nutritional supplements specifically tailored to their needs to maintain their good health and quality of life. The process of aging results in various changes in an individual, including psychological, physiological, and social, which affect their dietary and food choices. ging population increasingly relies on habitual food choices and tailored dietary consumption patterns. The rising aging population in some countries, over the years, has increased the demand for developing age-friendly food alternatives with enhanced nutritional value to support their overall health, which has led to an increased demand for dietary supplements that further support the market growth. With increasing bone health and mobility concerns, consumers have become more aware of healthy aging and disease prevention. Thus, there is an increased demand for supplemental nutrition solutions that align with the nutritional needs of aging consumers.

Restraints: High cost of dietary supplements

Science and technology are helping people identify foods that will help people manage their weight and overall health. Dietary supplements involve significantly high costs, which could act as a restraint for the growth of the market. Few players, such as Amway, offer supplements under the brand Nutrilite, which is significantly expensive. Dietary supplements also involve the high cost of research and customization. These supplements being less economic might restrict the growth of the dietary supplements market, particularly in price-sensitive countries such as South Africa and India. Asian countries are yet to adapt to the growing trend of nutrition-specific supplements.

With the increasing concerns of poor health and changes in lifestyle, consumers have shifted to dietary supplements to build their core strength and for biological benefits. Although these dietary supplements are comparatively less economical, which, in turn, is projected to restrict the market growth.

North America is projected to account for the largest market during the forecast period

North America is projected to dominate the market during the forecast period owing to the high prevalence of chronic diseases in countries such as the US. Vitamins and multivitamins are gaining traction as consumers are shifting to dietary supplements for the prevention of chronic diseases. Emerging markets in economies such as the Asia Pacific and South American countries are going to be potential markets for dietary supplement manufacturers.

Key Market Players:

Key players in this market include Amway (US), Herbalife Nutrition (US), ADM (US), Pfizer (US), Abbott Laboratories (US), Arkopharma Laboratories (France), Bayer (Germany), Glanbia (Ireland), Nature’s Sunshine Products (US), FANCL (Japan), Danisco (Denmark), Bionova Lifesciences (India), XanGo (US), Ekomir (Russia), American Health (US), Pure Encapsulations (US), UST Manufacturing (US), Capstone Nutrition (US), Anona GmBH (Germany), Plantafood Medical GmBH (Germany), Carlyle Group (US), Bio-Botanica Inc. (US), GlaxoSmithKline (UK), Nu Skin Enterprises (US), and Nutraceutics (US).

{kind=link}