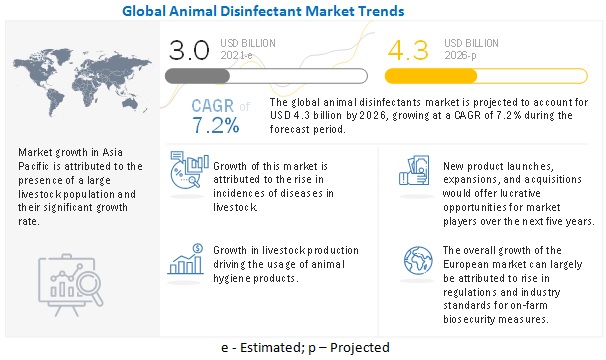

According to MarketsandMarkets "Animal Disinfectants Market by Application (Dairy Cleaning, Swine, Poultry, Equine, Dairy & Ruminants, and Aquaculture), Form (Liquid and Powder), Type (Iodine, Lactic Acid, Hydrogen Peroxide), and Region - Global Forecast to 2026", The global animal disinfectants market size is estimated to be valued at USD 3.0 billion in 2021. It is projected to reach USD 4.3 billion by 2026, recording a CAGR of 7.2% during the forecast period. The market has a promising growth potential due to several factors, including the rising awareness regarding hygiene and sanitation amidst this COVID-19 pandemic and increasing demand for meat and other animal products.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=38718363

COVID-19 Impact on the Animal Disinfectant Market

The impact of COVID-19 lockdown was tremendous in scale across the globe and profound especially in the key consumption markets for animal disinfectants. The demand for disinfectant products channelized for the livestock sector has remained high, with manufacturing plants for both disinfectants and water treatment being utilized at almost full capacity for companies such as Lanxess. However, the supply-chain disruptions in the key emerging markets, especially Mexico and Central America, negatively impacted the sales, albeit for a temporary period. The last mile connectivity to small and medium-scale livestock farms suffered a setback due to weakness in the distribution channels. Prominent players in the market such as Neogen expect a surge in demand with markets opening up gradually, and thus, capacity-building remains among the major focus areas. Key giants have also embarked on inorganic growth strategies by acquiring regionally-prominent disinfectant manufacturers and thereby strengthening their geographical outreach. Livestock disinfectant companies are also intensifying their efforts to develop a plethora of anti-bacterial, anti-fungal, and anti-viral solutions in the wake of growing concerns for zoonotic diseases.

Restraint: High entry barriers for players

The high costs associated with the development and registration of animal disinfectant products can result in small to medium-scale companies losing out to larger players. Another barrier for smaller players entering the market is the dynamic nature of the market itself, which has recently witnessed prominent players intensively seeking to consolidate their position through inorganic growth attempts such as acquiring smaller market players. New companies showing disruptive potential become the key targets for acquisitions by larger players such as Neogen Corp. and CID Lines.

Prominent players in the market are intensively seeking to increase their market share with the combination of inorganic and organic growth trajectories with former holding precedence in the form of growing number of acquisitions witnessed in recent years. The regulatory framework in the developed markets of North America and Western Europe is very stringent, with growing focus on good hygiene practices (GHP) which are cost-intensive thereby hindering the entry of small to medium-scale enterprises.

On the basis of application, dairy cleaning segment is expected to retain its dominance in the foreseeable period

Dairy cleaning is a terminal biosecurity measure, which is carried out at regular intervals. Due to the cost factor for larger cattle herds, the use of dairy cleaning has a greater significance in the developed markets. Countries in regions such as Europe and North America maintain large-scale farms and dairy farms required to maintain proper dairy cleaning measures to ensure the efficacy of the livestock and the equipment.

Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=38718363

Asia Pacific is projected to be the fastest-growing region in the animal disinfectant market.

The animal disinfectant market in Asia Pacific is driven by growing inclination towards animal-based food products that have prompted stakeholders in supply-chain to ramp up their production and intensify rearing leading to greater demand for cleaning and hygiene products, including disinfectants. The region has also witnessed growing regulatory focus on the Good Hygiene Practices (GHP) that are embedded as part of various mandatory regulations to be followed at dairy, poultry, swine, equine and aquaculture sectors. Markets in South East Asia such as Singapore and Malaysia are providing vital cues to improve hygiene infrastructure in animal husbandry and this trend is largely adopted by other countries in the region such as Thailand, Vietnam, Indonesia where there is a strong need to implement robust disinfection protocols.

Key Market Players

Key global market players offer wide range of animal disinfectant products to improve animal health and performance. Prominent livestock disinfectant manufacturers have strong presence in the European and North America countries. The key companies in the animal disinfectant market are Neogen Corporation (US), GEA (Germany), Lanxess AG (Germany), Zoetis (US), Kersia Group (France), and CID Lines (Belgium). Various strategies, such as expansions, mergers & acquisitions, and new product launches, were adopted by the key companies to remain competitive in the animal disinfectant market.