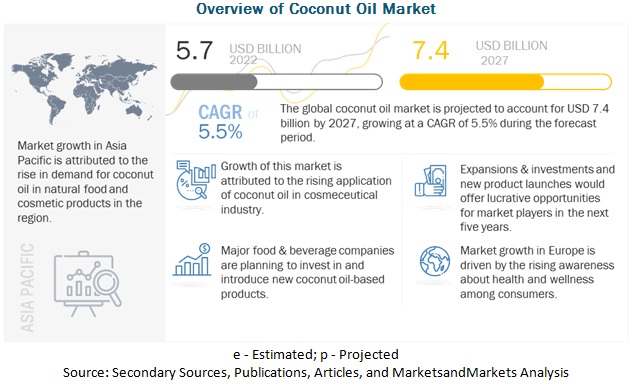

The global Coconut Oil Market size is estimated to be valued at USD 5.7 billion in 2022 and is projected to reach USD 7.4 billion by 2027, recording a CAGR of 5.5% during the forecast period in terms of value. The demand for coconut oil is increasing moderately due to increasing demand for natural ingredients.

Key players in this market include Cargill Incorporated (US), ADM (US), Bunge Limited (US), Mangga Dua (Indonesia), Greenville Agro Corporation (Philippines), Royce Food Corporation (Philippines), Novel Nutrients Pvt. Ltd. (India), Aromaax International (India), Adams Group (US), and Connoils LLC (US).

Download PDF Brochure @

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=78320975

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=78320975

Impact of COVID-19 on Coconut Oil Market

The COVID-19 pandemic significantly impacted the overall food & beverage industry. At one end, lockdowns imposed by various countries affected the import and export activities, leading to the disruption in the supply chain. However, as restrictions were lifted, companies came back on track with their businesses. On the other hand, consumers became more aware of the food products they consumed in the wake of the pandemic. Consumers are shifting toward products containing ingredients that are beneficial for their health. This is anticipated to boost the demand for coconut oil during the review period. Moreover, the demand for cosmetic products containing organic natural ingredients is rising, which is further forecasted to drive the market.

The key players are fixated upon improving their market shares, while their newer start-ups are being established rapidly in the market. The coconut oil market can be classified as a competitive market as it has the presence of a large number of organized players, accounting for a major part of the market share, present at the global level, as well as unorganized players present at the local level in several countries. There are numerous existing and emerging companies, particularly in the Asian markets.

Cargill is engaged in the manufacturing and marketing food ingredients, risk management, agricultural products, financial and industrial products, and services worldwide. The company covers 75 businesses under its four major categories: food ingredients & application, animal nutrition & protein, origination & processing, and industrial & financial services. The company offers coconut oil under the food ingredients & application segment.

Request for Customization @

https://www.marketsandmarkets.com/requestCustomizationNew.asp?id=78320975

https://www.marketsandmarkets.com/requestCustomizationNew.asp?id=78320975

Archer Daniels Midland Company (ADM) is primarily engaged in producing food ingredients, animal feed & feed ingredients, biofuels, and naturally derived alternatives to industrial chemicals. The company operates through four business segments: agriculture services and oilseeds, carbohydrate solutions, nutrition, and others. ADM offers coconut oils under its food & beverage solutions segment. Coconut oil from ADM offers a great-tasting, fast melting option with various uses as it contains medium-chain fatty acids found in medium-chain triglycerides (MCT).