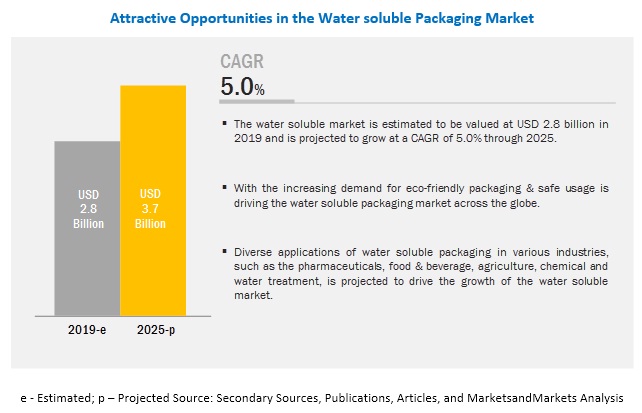

The report "Water Soluble Packaging Market by Raw Material (Polymer, Surfactant, and Fiber), End Use (Industrial, and Residential), Solubility Type (Cold Water Soluble and Hot Water Soluble), Packaging Type, and Region - Global Forecast to 2025" According to MarketsandMarkets, the water soluble packaging market is estimated to be valued at USD 2.8 billion in 2019 and is projected to reach USD 3.7 billion by 2025, recording a CAGR of 5.0%. The rapidly growing environmental and sustainability concerns across the globe and government initiatives to reduce the use of plastics are driving the market for water soluble packaging.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=243293980

The food & beverage and agriculture in industrial segment are

projected to witness the significant growth during the forecast

Based on end use, the water soluble packaging market is segmented into industrial and residential, wherein industrial segment is sub-divided into pharmaceuticals, food & beverages, agriculture, chemicals, and water treatment. The food & beverages and agriculture segments are projected to witness significant growth during the forecast period due to the increasing concerns toward waste production due to high use of non-biodegradable plastics and their harmful effects on packaged food & beverages.

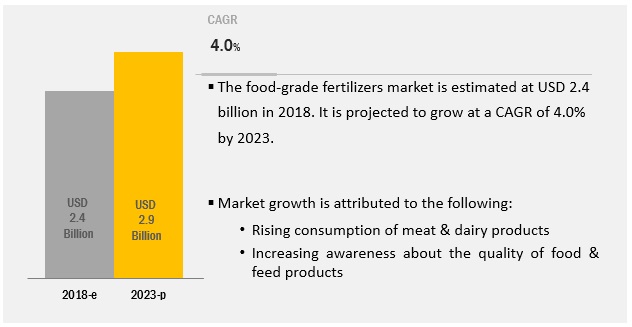

In the agriculture industry, chemical fertilizers wrapped with water soluble packets ease out the handling process. Also, dissolved packaging of the fertilizers cut down the packaging waste generation and leads to reduced cleaning costs.

The pouches segment is accounted to have the major share in the water

soluble packaging market during the forecast period

By packaging type, the water soluble packaging market is segmented into pouches, bags, and pods & capsules. The pouches segment is estimated to account for the major share in the water soluble packaging market due to the high usage of water soluble packaging in the chemical industries. In the current scenario, most of the packaging is made of plastic for safe and secure handling and usage of detergent; water soluble packaging of detergent serves the purpose better. Detergent wastage can be minimized as water soluble packets or sachets can be made available to consumers for household and industrial cleaning. The water soluble packaging avoids direct contact with detergent as the product can be used without removing the package, which will ensure safe usage.

Make an Inquiry @ https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=243293980

The Asia Pacific region is projected to witness the fastest growth

during the forecast period

The water soluble packaging market in Asia Pacific is projected to witness high growth due to the strong local and export demand. The rising population and growing number of manufacturing industries in Asia Pacific is the key factor driving the market for water soluble packaging. The manufactured product is used domestically as well as exported. China and Japan are the hubs for water soluble film production. In India, the population is increasing rapidly, and the country is striving for safe, better, clean, and healthy lifestyle. The water soluble packaging market will grow in these regions at a high rate.

This report includes a study on the marketing and development strategies, along with the product portfolios of the leading companies. It consists of the profiles of leading companies such as Lithey Inc. (India), Mondi Group (Austria), Sekisui Chemicals (Japan), Kuraray Co. Ltd. (Japan), Mitsubishi Chemical Holdings (Japan), Aicello Corporation (Japan), Aquapak Polymer Ltd (UK), Lactips (France), Cortec Corporation (US), Acedag Ltd. (UK), MSD Corporation (China), Prodotti Solutions (US), JRF Technology LLC (US), and Amtopak Inc. (US).