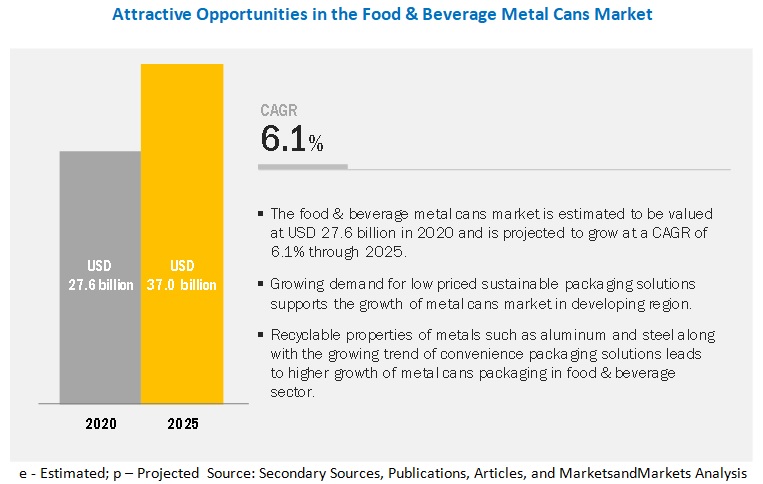

The food & beverage metal cans market is estimated to be valued at USD 27.6 billion in 2020 and is projected to reach USD 37.0 billion by 2025, recording a CAGR of 6.1% during the forecast period. The increasing demand for sustainable packaging drives the growth of the food & beverage metal cans market.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=251

Key players in this market include Crown Holdings, Inc (US), Ball Corporation (US), Silgan Holdings Inc. (US), Ardagh Group (Luxembourg), CAN-PACK S.A. (Poland), Kian Joo Group (Malaysia), CPMC Holdings Limited (China), Huber Packaging Group GmbH (Germany), CCL Industries (US), Toyo Seikan Group Holdings Ltd (Japan), Universal Can Corporation (Japan), Independent Can Company (US), Mauser Packaging Solution LLC (Germany), Visy (Australia), Lageen Food Packaging (Israel), Massilly Holding S.A.S (France), P. Wilkinson Containers Ltd. (UK), Unimpack (The Netherlands), Müller und Bauer GmbH (Germany), and Allied Cans (Canada).

Crown Holdings, Inc (US) is a key supplier, offering products for food & beverage metal packaging. Its operations focus on making it a specialty metal packaging company, which is growing sustainably by incorporating new foundational platforms into its own technologies. It is pursuing competitive superiority by creating demand and by developing high-value-added and customized products based on client requirements.

In 2018, the company acquired Signode Industrial Group Holdings (Illinois) Ltd., a leading global provider of transit packaging systems and solutions. This acquisition helped the company to strengthen its geographic reach and market position in the US.

Ball Corporation (US) is a public registered company headquartered in the US and one of the leading developers, manufacturers, and distributors of metal packaging. The company works in collaboration with the brands and retailers, and packaging manufacturers to design circular economy solutions to maintain its market position.

Ball Corporation offers products for metal packaging of beverage cans such as standard cans and specialty cans. In October 2019, the company expanded its manufacturing plants in Rome, Georgia to cater to the growing demand for beverage packaging in the US.

Speak to Analyst @ https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=251

The Asia Pacific food & beverage metal cans market is projected to have higher growth potential in the coming years. A large consumer market and increasing disposable income in India and China are driving the growth of the demand for high-quality metal packaging. Also, China is the hub for the manufacture of metal cans and has sufficient manufacturing plants to meet the demand for food & beverage metal packaging. Moreover, rapid urbanization in countries such as India and China are expected to result in high growth of the food & beverage metal cans market in Southeast Asia during the forecast period.