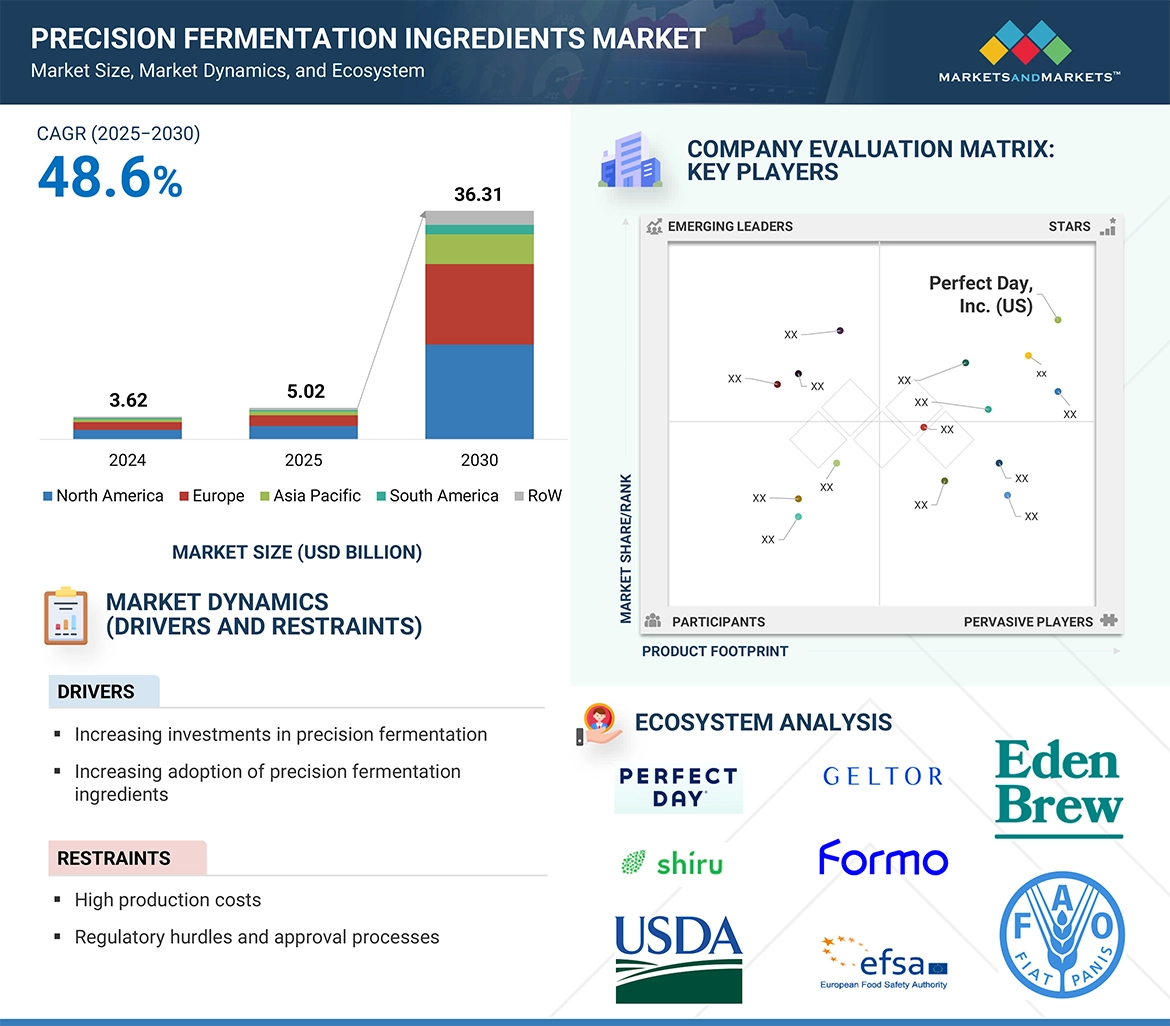

The precision fermentation ingredients market is projected to grow from USD 5.02 billion in 2025 to USD 36.31 billion by 2030, registering an impressive CAGR of 48.6% during the forecast period. This growth is largely driven by increasing demand for sustainable, animal-free alternatives across the food, pharmaceutical, and cosmetics sectors. Key market drivers include rising consumer awareness around ethical consumption, the need to reduce greenhouse gas emissions from traditional animal agriculture, and advancements in synthetic biology that enable scalable, cost-effective production of functional ingredients such as proteins, enzymes, and vitamins. Additionally, strong government support for novel food technologies and significant venture capital investment in food tech startups are propelling industry expansion.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=30824914

Yeast Segment Dominates by Microbe Type

Within the microbe type segment, yeast holds a dominant position due to its well-established role in producing a wide range of functional ingredients. Its advantages include ease of genetic modification, high yield potential, and the ability to grow on low-cost substrates—making it an ideal organism for commercial-scale production. Yeast's proven performance and stability have cemented its role in the manufacturing of precision-fermented proteins, enzymes, and vitamins for applications in the food, beverage, and pharmaceutical industries.

Whey & Casein Proteins Lead by Ingredient Type

By ingredient type, whey and casein proteins represent the leading segment in the market. These animal-identical dairy proteins offer exceptional nutritional value and functionality, making them ideal for applications such as dairy alternatives, sports nutrition, and functional food products. Precision fermentation enables the production of these proteins without the use of animals, providing a sustainable solution that appeals to environmentally conscious and lactose-intolerant consumers. Their versatility and alignment with the rising demand for clean-label, high-protein products continue to drive their market dominance.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=30824914

Europe Holds a Key Regional Market Share

Europe is expected to command a significant share of the global precision fermentation ingredients market, fueled by strong regulatory support for sustainable food innovation and a rapidly growing demand for plant-based and animal-free products. Countries like Germany, the Netherlands, and the UK have emerged as leading hubs for precision fermentation startups and research institutions.

The region’s well-developed food and beverage sector is increasingly adopting precision-fermented ingredients to meet evolving consumer preferences. Strategic collaborations between major food manufacturers and biotech firms, along with a broader push for clean-label formulations and climate goals, further bolster Europe's leadership in this market.

Leading Precision Fermentation Ingredients Companies:

The report profiles key players such as Perfect Day, Inc. (US), Geltor (US), The EVERY Company (US), Impossible Foods Inc. (US), ImaginDairy Ltd. (Israel), Shiru, Inc. (US), FORMO FOODS GMBH (Germany), EDEN BREW (Australia), Change Foods (US), New Culture (US), Helaina Inc. (US), Naplasol (Belgium), Myco Technology, Inc. (US), Remilk Ltd. (Israel), and Triton Algae Innovations (US).