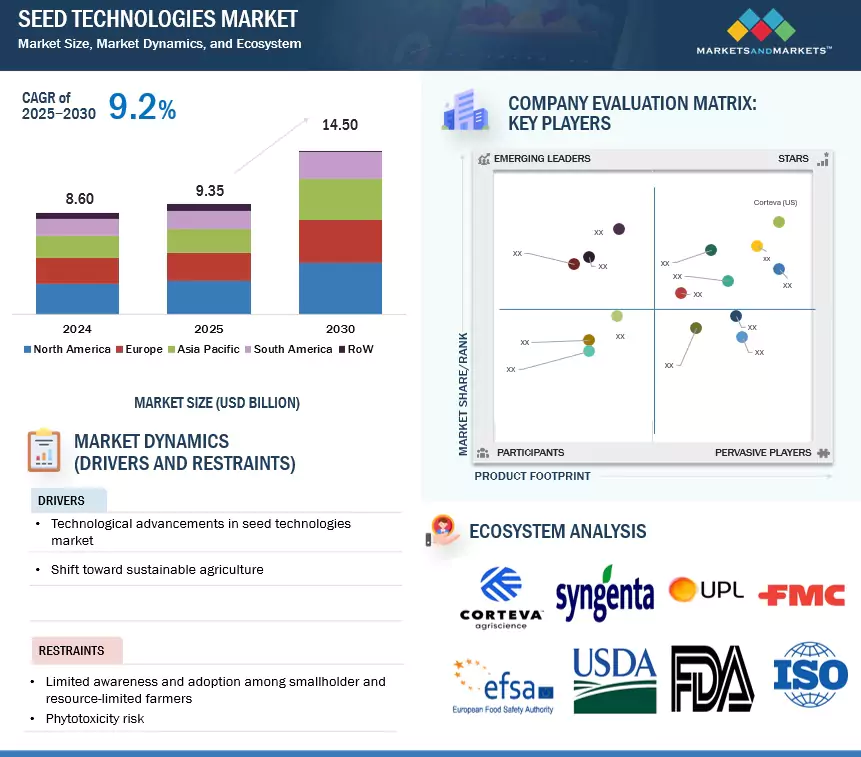

The global seed technologies market is projected to grow from USD 9.35 billion in 2025 to USD 14.50 billion by 2030, registering a CAGR of 9.2% during the forecast period. Growth is fueled by the rising adoption of high-value hybrid and genetically modified seeds and the increasing need for early-stage crop protection.

Shifts in agricultural practices—such as restrictions on foliar pesticide use and the global move toward sustainable farming systems—are accelerating the demand for seed-applied solutions. At the same time, advancements in treatment formulations and integration with precision farming technologies are improving efficiency and outcomes. Supportive government policies and rising farmer awareness, particularly in emerging markets, are further propelling market expansion.

Download PDF Brochure:

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=25852111

Market Insights by Function

Biological seed protection represents a significant share of the seed technologies market. This segment is gaining momentum as farmers and seed companies embrace eco-friendly crop protection solutions. Beneficial microbes, fungi, and bacteria are being deployed to defend seeds against soil-borne pathogens and pests, while also enhancing plant health and resilience.

Adoption is supported by growing regulatory pressure to limit synthetic chemicals and reduce residue levels. These biological treatments offer multiple mechanisms—such as pathogen suppression, systemic resistance induction, and nutrient solubilization—making them versatile complements or alternatives to conventional chemicals. The increasing emphasis on regenerative agriculture, organic farming, and soil health has reinforced demand. With continuous innovation and wider regulatory approvals, biological seed protection is becoming a mainstream component of seed treatment portfolios.

Market Insights by Crop Type

The oilseeds segment holds a notable share of the global seed technologies market. Crops such as soybean, canola, and sunflower are highly valued but also vulnerable to early-stage pests and diseases, driving demand for effective seed protection.

The rising adoption of hybrid and genetically modified oilseed varieties has further strengthened the role of seed treatments. Both chemical and biological solutions are being applied to safeguard yield potential. In addition, the push toward sustainable agriculture and advancements in treatment formulations continue to expand the adoption of seed-applied technologies in oilseed farming.

Request Sample Pages:

https://www.marketsandmarkets.com/requestsampleNew.asp?id=25852111

Market Insights by Region

North America leads the global seed technologies market, supported by the extensive use of genetically modified and hybrid seeds in crops like corn, soybean, and canola. Farmers in the region rely heavily on seed treatments to protect high-value seeds from pests and diseases at the earliest growth stages.

The market benefits from strong agricultural infrastructure, advanced crop protection practices, and regulatory shifts away from foliar pesticides in the US and Canada, which favor targeted seed treatments. The demand for biological solutions is also increasing, driven by soil health concerns and consumer preference for residue-free produce.

North America’s leadership is reinforced by:

- Strong presence of global seed technology companies

- Ongoing R&D in next-generation formulations

- Integration with precision farming and conservation tillage practices

This combination positions North America as both the largest market and a global innovation hub for seed technologies.

Leading Seed Technologies Companies:

The report profiles key players such as BASF SE (Germany), Bayer AG (Germany), UPL (India), Corteva (US), Croda (UK), FMC (US), Nufarm (Australia), Syngenta (US), Germains Seed (UK), and Sumitomo Chemicals (Japan).