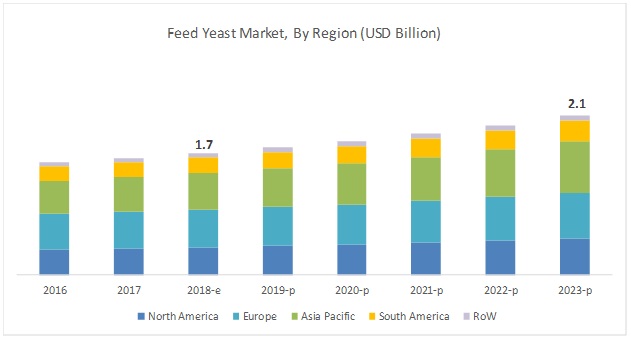

The report "Feed Yeast Market by Type (Probiotic Yeast, Brewer’s Yeast, Specialty Yeast, and Yeast Derivatives), Livestock (Cattle, Swine, Poultry, Aquatic Animals, and Pets), Genus (Saccharomyces spp. and Kluyveromyces spp.), and Region - Global Forecast to 2023", The feed yeast market is projected to reach USD 2.1 billion by 2023, from USD 1.7 billion in 2018, at a CAGR of 5.27% during the forecast period. The market is driven by factors such as ban on the use of antibiotics in feed and increasing use of yeast as a nutritional supplement for livestock.

Report Objectives:

Report Objectives:

- Determining and projecting the size of the feed yeast market with respect to type, livestock, genus, and region over a five-year period from 2018 to 2023

- Identifying attractive opportunities in the market by determining the largest and fastest-growing segments across regions

- Analyzing the demand-side factors on the basis of the following:

- Impact of macro- and microeconomic factors on the market

- Shifts in demand patterns across different subsegments and regions

- Understanding the competitive landscape for a comparative analysis of market leaders and identifying the key market shareholders across the industry.

- Analyzing regulatory frameworks across regions and their impact on prominent market players

- Providing insights on key investments in technology innovations

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=108142106

The use of yeast derivatives for feed production is projected to remain high during the forecast period.

Beta-glucans, nucleotides, and mannooligosaccharides are the major yeast derivatives that exhibit efficient pathogen binding capacity, which restricts the growth of pathogens in the animal body. In addition, beta-glucans are the type of yeast derivatives that trigger the immune response in the animal body. The health benefits associated with the use of yeast derivatives as a feed additive increases its demand in the feed industry. Thus, the yeast derivative segment is projected to record the highest CAGR from 2018 to 2023.

The Saccharomyces Spp. segment is estimated to dominate the feed yeast market in 2018.

Saccharomyces Spp. such as Saccharomyces cerevisiae and Saccharomyces boulardii are majorly used for yeast production and is used as one of the most important ingredients in feed. With the increasing demand for natural growth promoters for animals, the preference for Saccharomyces Spp. has increased as it is considered to be one of the best sources for nutritional yeast. The Saccharomyces Spp. segment accounted for the highest share in the feed yeast market in 2017 and witnessed high demand for use in feed yeast production.

Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=108142106

With the introduction of stringent regulations, Europe is estimated to dominate the feed yeast market in 2018.

The feed yeast market in Europe is driven by the introduction of stringent regulations pertaining to the use of antibiotics in feed. Increasing awareness about the benefits of feed yeast is projected to contribute to the market growth. The high demand for quality and nutrient-rich feed in the European countries has led to the high demand for feed yeast among farmers. Moreover, the European legislators are also concerned about food and animal safety and thus have implemented many safety laws for the same. With high concerns related to animal health, the EU government has put a ban on the use of antibiotic growth promoters in feed due to its negative impact on animal health as well as on the health of human consumers. For the replacement of those antibiotics, naturally-sourced feed ingredients that have antibiotic properties such as feed yeast were developed by manufacturers.

This report includes a study of the development strategies of leading companies. The scope of this report includes a detailed study of feed yeast manufacturers such as Associated British Foods PLC. (UK), Archer Daniels Midland Company (US), Alltech Inc. (US), Cargill (US), Lesaffre (France), Angel Yeast Co. Ltd. (China), and Lallemand Inc. (Canada).