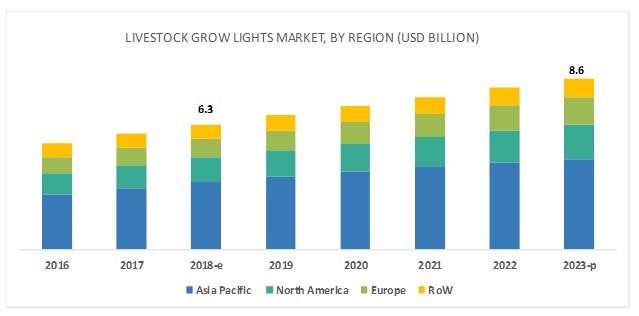

The report "Livestock Grow Lights Market by Type (Fluorescent, Light-Emitting Diode (LED), Incandescent, and Hid), Livestock (Cattle, Poultry, Swine, and Others), Installation Type (Retrofit and New Installation), and Region - Global Forecast to 2023", The livestock grow lights market is projected to grow from USD 6.3 billion in 2018 to USD 8.6 billion by 2023, at a CAGR of 6.4% during the forecast period. The major factors driving the livestock grow lights market include the increasing demand and consumption of animal-based products such as meat, milk, and eggs. Further, rising focus on livestock welfare and growth along with technological innovation for smart farming practices is projected to drive the market.

By type, the LED segment is projected to witness the fastest growth in the livestock grow lights market during the forecast period.

The LED segment is projected to witness the fastest growth due to its significant energy savings and longer durability properties. In addition, it is more energy-efficient with one-fifth of the power consumption of incandescent bulbs. LED grow lights provide a wide range of spectrum from blue to red that can be customized to the desired spectrum as per the spectral sensitivity of the livestock. By optimizing different spectrum levels and radiation, farmers could create lighting environment that is best suited for their livestock's wellbeing.

Download PDF Brochure:

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=77298993

The cattle segment is projected to account for the largest market share during the forecast period

Based on the livestock segment, the market is estimated to be dominated by the cattle segment in 2018. In dairy farms, grow lights help in improving the output of milk production from dairy cattle; whereas in beef cattle, grow lights are used to stimulate muscle growth to increase meat production. Further, the constantly rising demand for dairy & dairy-based products including milk, cheese, yogurt, and butter in both, developed and developing economies are projected to drive the demand for grow lights in cattle farms.

Asia Pacific is projected to hold the largest market share during the forecast period.

Asia Pacific is estimated to account for the largest share of the market in 2018. The market in the region is driven by the presence of a large livestock population and their rising growth. Furthermore, the increasing number of livestock farms and the growing size of existing farms are also projected to contribute to the large market of the Asia Pacific region. Adoption of smart technologies for farms to reduce input cost along with energy consumption, and focus on the growth and development of the livestock population by farmers also drives the demand for livestock grow lights in this region.

Major vendors in the livestock grow lights market include OSRAM (Germany), Signify Holding (Netherlands), DeLaval (Sweden), Big Dutchman (Germany), Uni-light LED (Sweden), Once Inc. (US), AGRILIGHT BV (Netherlands ), Aruna Lighting (Netherlands), HATO BV (Netherlands), Shenzhen Hontech-Wins (China), CBM Lighting (Canada), Fienhage Poultry Solutions (Germany), SUNBIRD (South Africa), ENIM UAB (Lithuania), and Greengage Lighting (UK).

Speak to Analyst:

https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=77298993

Key Questions addressed by the report:

By type, the LED segment is projected to witness the fastest growth in the livestock grow lights market during the forecast period.

The LED segment is projected to witness the fastest growth due to its significant energy savings and longer durability properties. In addition, it is more energy-efficient with one-fifth of the power consumption of incandescent bulbs. LED grow lights provide a wide range of spectrum from blue to red that can be customized to the desired spectrum as per the spectral sensitivity of the livestock. By optimizing different spectrum levels and radiation, farmers could create lighting environment that is best suited for their livestock's wellbeing.

Download PDF Brochure:

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=77298993

The cattle segment is projected to account for the largest market share during the forecast period

Based on the livestock segment, the market is estimated to be dominated by the cattle segment in 2018. In dairy farms, grow lights help in improving the output of milk production from dairy cattle; whereas in beef cattle, grow lights are used to stimulate muscle growth to increase meat production. Further, the constantly rising demand for dairy & dairy-based products including milk, cheese, yogurt, and butter in both, developed and developing economies are projected to drive the demand for grow lights in cattle farms.

Asia Pacific is projected to hold the largest market share during the forecast period.

Asia Pacific is estimated to account for the largest share of the market in 2018. The market in the region is driven by the presence of a large livestock population and their rising growth. Furthermore, the increasing number of livestock farms and the growing size of existing farms are also projected to contribute to the large market of the Asia Pacific region. Adoption of smart technologies for farms to reduce input cost along with energy consumption, and focus on the growth and development of the livestock population by farmers also drives the demand for livestock grow lights in this region.

Major vendors in the livestock grow lights market include OSRAM (Germany), Signify Holding (Netherlands), DeLaval (Sweden), Big Dutchman (Germany), Uni-light LED (Sweden), Once Inc. (US), AGRILIGHT BV (Netherlands ), Aruna Lighting (Netherlands), HATO BV (Netherlands), Shenzhen Hontech-Wins (China), CBM Lighting (Canada), Fienhage Poultry Solutions (Germany), SUNBIRD (South Africa), ENIM UAB (Lithuania), and Greengage Lighting (UK).

Speak to Analyst:

https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=77298993

Key Questions addressed by the report:

- Who are the major market players in livestock grow lights market?

- What are the regional growth trends and the largest revenue-generating regions for livestock grow lights?

- Which are the major regions that are projected to witness a significant growth for livestock grow lights?

- What are the major types of livestock grow lights that are projected to gain maximum market revenue and share during the forecast period?

- Which is the major type of livestock where grow lights are used that will be accounting for majority of the revenue over the forecast period?