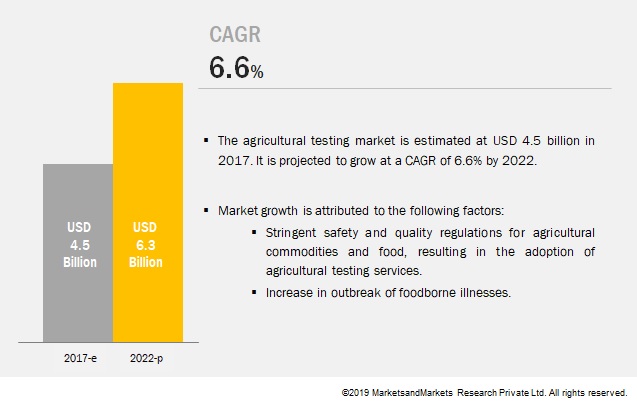

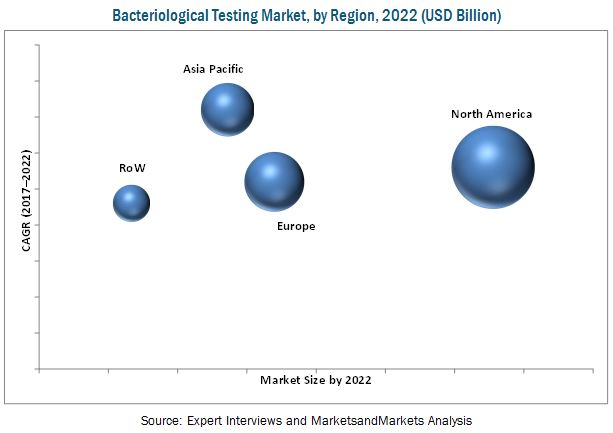

The report “Bacteriological Testing Market by Bacteria (Coliform, Salmonella, Campylobacter, Legionella, Listeria), Technology (Traditional, Rapid), End-use Industry (Food & Beverage, Water, Pharmaceutical, Cosmetics), Component, and Region – Global Forecast 2022″, The bacteriological testing market, by services, is estimated to be valued at USD 9.58 Billion in 2017, and is projected to reach USD 13.98 Billion by 2022, at a CAGR of 7.8%. The market is driven by a globally observed increase in outbreaks of foodborne illnesses, implementation of stringent food safety regulations in developed economies, and rise in incidences of microbial contamination in water reservoirs, due to increased urban & industrial waste. Lack of food control systems, technologies, infrastructure, and resources in developing countries and reluctance of municipal bodies to adopt new technologies are the main factors restraining the growth of this market.

The objectives of the report:

- To define, segment, and project the global market size for bacteriological testing

- To define, segment, and forecast the size of the bacteriological testing market with respect to bacteria, end-use industry, technology, component, and region

- To analyze the market structure by identifying various subsegments of the global bacteriological testing market

- To provide detailed information about the crucial factors that are influencing the growth of the market (drivers, restraints, opportunities, and challenges)

- To analyze the opportunities in the market for stakeholders and provide details of a competitive landscape for market leaders

- To forecast the size of the global bacteriological testing market and its various submarkets with respect to four main regions, namely, North America, Europe, Asia Pacific, and the Rest of the World (RoW), along with their respective key countries

- To strategically profile the key players and comprehensively analyze their core competencies

- To analyze the competitive developments such as mergers & acquisitions, expansions & investments, and new service & product launches in the bacteriological testing market

Download PDF Brochure:

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=238062451

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=238062451

The bacteriological testing services market, based on bacteria, has been segmented into Coliforms, Salmonella, Campylobacter, Legionella, Listeria, and others. The market for testing for Salmonella dominated in 2016, and is also projected to be fastest-growing segment during the forecast period. The severity of infection by this pathogen is generating demand for Salmonella testing in food and water samples, which in turn is driving the market for bacteriological testing.

The bacteriological testing services market, by technology, has been segmented into traditional and rapid. The rapid technology segment dominated the market in 2016, and is projected to grow at a higher CAGR by 2022. This is due to low turnaround time, higher accuracy, sensitivity, and ability to test a wide range of bacteria in comparison to traditional technological methods.

The bacteriological testing market, by end-use industry, has been segmented into food & beverage, water, pharmaceutical, and cosmetics. Testing for bacterial contamination in food & beverages is conducted for monitoring and assessment of food quality, and validation of food safety, in order to eliminate the risk of bacterial contamination. Bacteriological testing is performed across the food & beverage industry due to the rising incidence of food spoilage, foodborne illnesses, or food-related intoxication for the detection of various bacterial contaminations. The pharmaceutical segment is projected to grow at the highest CAGR in the overall bacteriological testing market during the study period. This is attributed to key factors such as the presence of well-established & globally accepted regulations that govern the evaluation of bacterial contamination during pharmaceutical manufacturing and raw material sourcing (coupled with the increasing volume of pharmaceutical drugs sold every year), increase in safety concerns related to pharmaceutical manufacturing in emerging countries, rise in market demand for safer drugs for disease treatment, and expansion of the drug development pipeline of key pharmaceutical manufacturers.

The bacteriological testing equipment market, by component, has been segmented into instruments, test kits, and consumables & reagents. This market was dominated by the instruments segment in 2016. The dominance of instruments is attributable to the introduction of sophisticated & improved technologies, increased effectiveness of instruments, and high price of such instruments compared to other components. The market for consumables & reagents is projected to be the fastest-growing during the forecast period. Consumables & reagents are vital components to be used to follow the set compliances of equipment. Therefore, increasing technical and regulatory complexity and their wide use in different instruments is driving this market.

Request for Customization:

The market in the Asia Pacific region is driven by the growing consumer awareness and increasing health consciousness, coupled with growing investments by testing companies in the region. Also, countries such as China, Australia, and those in Southeast Asia are becoming more aware of food safety and are implementing regulations for their testing, consequently driving the market in the region.

This report includes a study of marketing and development strategies, along with the services & product portfolios of leading companies. It includes the profiles of leading service companies such as SGS (Switzerland), Bureau Veritas (France), Intertek (UK), Eurofins (Luxembourg), TÜV SÜD (Germany), and ALS Limited (Australia). It also includes profiles of leading equipment providing companies such as 3M (US), Thermo Fisher (US), Merck (Germany), Agilent Technologies (US), Bio-Rad (US), and Romer Labs (Austria).