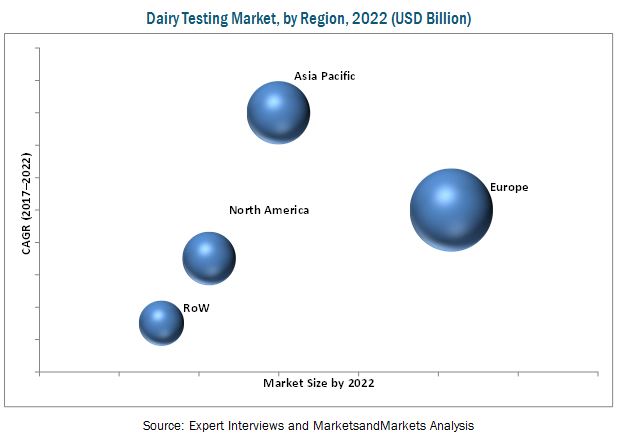

The report “Dairy Testing Market by Type (Safety (Pathogens, Adulterants, Pesticides), Quality), Technology (Traditional, Rapid), Product (Milk & Milk Powder, Cheese, Butter & Spreads, Infant Foods, Ice Cream & Desserts, Yogurt), and Region – Forecast to 2022″, The dairy testing market is projected to reach USD 5.90 Billion by 2022 from USD 4.13 Billion in 2017, at a CAGR of 7.4% from 2017. The market is driven by the increase in outbreaks of foodborne illnesses, globalization of dairy trade, and stringent safety & quality regulations for food. Lack of coordination among market stakeholders and improper enforcement of regulatory laws & supporting infrastructure in developing economies are the major restraints for this market.

The dairy testing market, based on type, has been segmented into safety testing & quality analysis. The safety testing segment dominated this market in 2016 and is also projected to be fastest-growing during the forecast period. This is attributable to the significant emphasis being laid on safety testing of food output with regulatory authorities focusing on addressing regulatory loopholes, preventing adulteration, malpractices, and labeling mandates.

Download PDF Brochure:

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=240885146

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=240885146

The dairy testing market, by technology, has been segmented into traditional and rapid. The rapid technology segment dominated the market in 2016 and is projected to be the fastest growing by 2022. Low turnaround time, higher accuracy, sensitivity, and the ability to test a wide range of contaminants in comparison to traditional technology are the reasons for the growth of the rapid technology segment.

The dairy testing market, by product, has been segmented into milk & milk powder, cheese butter & spreads, infant food, ice cream & desserts, yoghurt, and others. The milk & milk powder dominated the market in 2016 and is projected to be the fastest growing by 2022. This is due to economically motivated adulteration, poor hygiene of storage, faulty supply chains, and contaminated equipment, which have led to milk being contaminated, which upon consumption can cause serious health problems to humans.

The market in the Asia Pacific region is driven by the growing consumer awareness and increasing health consciousness coupled with growing investments by testing companies in the region. Also, Asia Pacific is home to major dairy producing countries such as China, Australia & New Zealand, and India as these countries are becoming more aware of food safety and are implementing regulations for their testing.

This report includes a study of marketing and development strategies, along with the service portfolios of leading companies. It also includes the profiles of leading companies such as SGS, Bureau Veritas, Intertek, Eurofins, TÜV SÜD, and ALS Limited, among others.

Request for Customization:

Target Audience:

- Manufacturers, importers & exporters, traders, distributors, and suppliers of dairy testing kits, equipment, reagents, chemicals, and other related consumables

- Dairy testing service providers

- Dairy producers, processors, and manufacturers of dairy products

- Government and research organizations

- Trade associations and industry bodies

- Regulatory bodies such as the Food and Drug Organization (FDA), European Food Safety Authority (EFSA), Food Standards Australia New Zealand (FSANZ), and Food Safety Commission of Japan