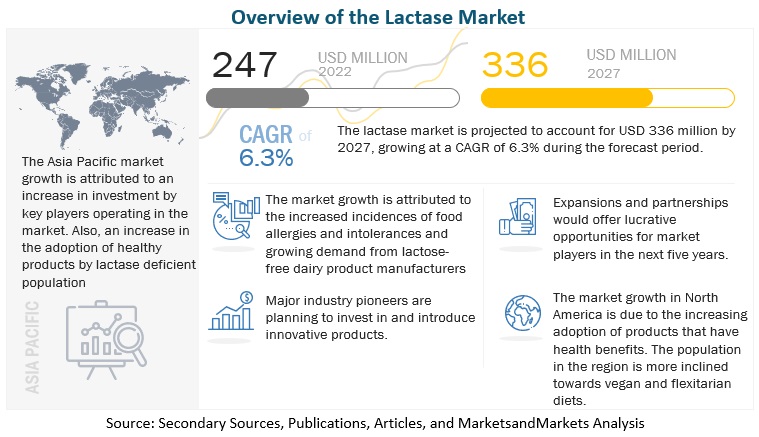

According to MarketsandMarkets, the lactase market is estimated to be valued at USD 217 million in 2020 and is projected to reach USD 298 million by 2025, recording a CAGR of 6.5 %, in terms of value. Factors such as rising cases of lactose-intolerant and growing demand from lactose-free dairy product manufacturers and increasing innovation and new product development in the application areas are projected to drive the growth of the lactase industry during the forecast period. However, the growth of the market is inhibited by factors, such as shifting preferences toward dairy-free alternatives and high processing cost and lack of technical expertise for lactase extraction.

Lactase is usually extracted from yeast. However, an extensive research & development is going on regarding the other sources of lactase enzymes, such as bacteria and fungi. Lactase enzymes extracted from bacterial sources have been used for lactose hydrolysis because of numerous benefits, such as their ease of fermentation, high activity, and the stability of the enzyme. Lactase enzymes sourced from a probiotic organism are used for food and food systems. Fungal sources of lactase enzymes possess optimal acidic pH range of 2.2 to 5.4. Owing to this, lactase sourced from fungi are more effective for the hydrolysis of lactose found in acidic substances, such as whey. These fungi-based enzymes are highly stable enzymes. The increasing research & developments about various sources of lactase enzymes gives opportunity to the lactase enzyme market to grow in the period forecasted.

Download PDF Brochure:

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=125332780

Challenges: High processing cost and lack of technical expertise for lactase extraction

Small & medium-sized enterprises have efficient cost management due to limited capital and resources. Many quality and productivity improvement techniques are generally not finding a place in SMEs (small-and medium-sized enterprises) due to the lack of knowledge and resources to implement the same. However, the high costs involved in adapting to new technologies, production, and extraction procedures have restricted SMEs from improving their operations. Moreover, the process of lactase extraction requires technical expertise and abundant knowledge, which is majorly not present with the SMEs. Thus, extraction of lactase enzymes with fully equipped knowledge and expertise is among the major challenges for the lactase enzyme market.

By form, liquid segment is projected to be the fastest growing segment in the lactase market during the forecast period

The liquid form of enzymes is generally less stable than the solid form, although it may have higher activity and better functionality than the powder form. It is directly used in the liquid form or sprayed and absorbed on a solid carrier. Among all applications, the liquid form of lactase enzyme is widely used in the food & beverage industry and pharmaceutical applications for products, such as syrups. Liquid lactase enzyme accelerates chemical, biological, and metabolic reactions by altering a reaction's efficiency and results in making the pharmaceutical product more efficient for human use.

The North America region dominated the lactase market with the largest share in 2019, whereas Asia-Pacific is expected to witness the highest growth rate.

The lactase market in North America is dominant due to the growing demand for different types of lactose-free products such as drinkable yogurt, ice-cream, and flavored milk. Increasing awareness about lactose intolerance among consumers and growing inclination towards health promoting dietary supplements are the key factors that are projected to drive the growth of the market in the North American region.

Speak to Analyst:

https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=125332780

The fastest growing market is Asia-Pacific for lactase. The increase in awareness and self-diagnosis among lactose intolerant population, also growing consumption of lactose-free products offers potential growth for the lactase manufactures in the region. The increase in health concerns and the growing trend of opting for reduced added sugar/no added sugar claims have created growth opportunities for lactase in the region. Major players such as Valio Ltd. (Finland), expanded its production facility in China to cater lactose-free products for lactose intolerant population.

This report includes a study on the marketing and development strategies, along with the product portfolios of leading companies. It consists of profiles of leading companies, such as Chr. Hansen Holdings A/S (Denmark), Kerry Group (Ireland), Koninklijke DSM N.V (the Netherlands), Novozymes (Denmark), Merck KGaA (Germany), DuPont (US), Senson (Finland), Amano Enzyme (Japan), Advanced Enzyme Technologies (India), Enmex (Mexico), Antozyme Biotech Pvt. Ltd. (US), Nature Bioscience Pvt. Ltd. (India), Aumgene Biosciences (India), Creative Enzymes (US), Biolaxi Corporation (India), Novact Corporation (US), Enzyme Bioscience (India), Infinita Biotech Private Limited (India), Rajvi Enterprise (India), and Mitushi Biopharma (India).