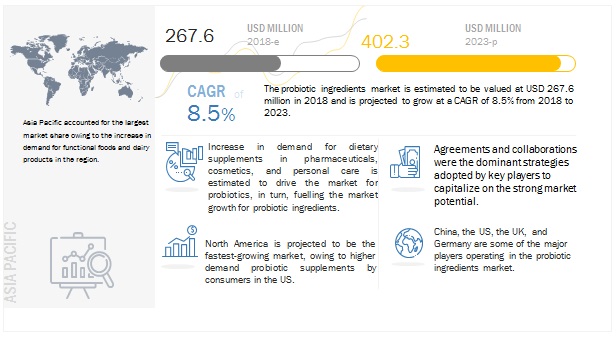

The report "Probiotic Ingredients Market by Application (Functional Foods & Beverages, Pharmaceuticals, and Animal Nutrition), Source (Bacteria and Yeast), Form (Dry and Liquid), End-User (Human and Animal), and Region - Global Forecast to 2023", is estimated at USD 268 million in 2018 and is projected to reach USD 402 million by 2023, growing at a CAGR of 8.5% during the forecast period. The market is driven by factors such as the increasing popularity of probiotic dietary supplements and the participation of government bodies in the R&D of probiotics.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=238635114

By application, the market has been segmented into functional food & beverages, pharmaceuticals, animal nutrition, and others which include cosmetics & personal care products. The pharmaceuticals segment is growing at the highest rate owing to a spike in the number of diseases such as antibiotic-associated diarrhea, inflammatory bowel disease, lactose intolerance, irritable bowel syndrome, vaginal infections, rheumatoid arthritis, liver cirrhosis, and immune enhancement. The intake of dietary supplements for overall improvement in health among consumers would drive the growth of the segment during the forecast period.

By form, the market has been segmented into dry and liquid. The dry form is projected to dominate the market during the forecast period owing to lower costs in transportation when compared with liquid form. The dry form of probiotic ingredients has a higher shelf-life, due to which it is preferred by manufacturers and suppliers.

By end use, the probiotic ingredients market has been segmented into animal and human use. While human use accounts for a larger market share during the forecast period, the usage of probiotic strains in the animal nutrition industry is growing. Probiotic strains are used in feed to enhance the effectiveness of nutrients and show their effects on the gut by aiding in better digestion and reducing the impact of pathogenic bacteria, which causes various diseases in animals. The animals can grow better as the feed is altered in terms of quality and palatability due to its added probiotic content. The aim of probiotic strains is to take care of deficiencies of the natural microflora and provide animals with better resistance against diseases.

Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=238635114

Probiotics are gaining popularity in the Asia Pacific market particularly in the animal nutrition segment due to the growing concerns about their health and productivity. The application of probiotic strains is projected to increase due to the consumer demand for application in functional foods and pharmaceutical end products. India offers a huge potential in this region due to the increasing number of pharmaceutical companies involving themselves in the licensing and development of probiotic drugs. China’s growth in terms of sales is attributed to the growing application of probiotics in the infant formula business.

This report includes a study on the marketing and development strategies, along with a study on the product portfolios of the leading companies. It includes the profiles of leading companies such as Kerry (Ireland), DowDuPont (US), Chr. Hansen (Denmark), Biogaia (Sweden), Probi (Sweden), Glac Biotech (Taiwan), Bifodan (Denmark), Lallemand (Canada), UAS Laboratories (US), and Biena (US).