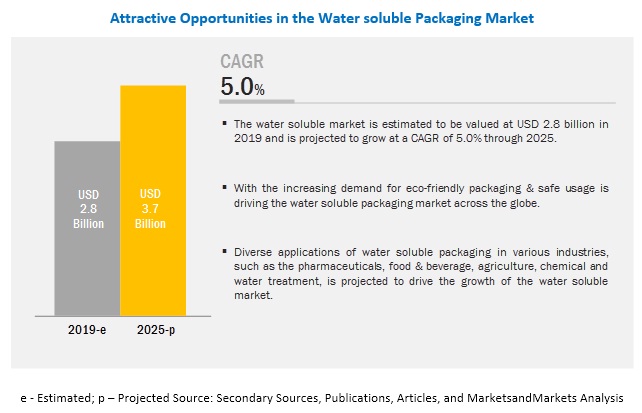

The report "Water Soluble Packaging Market by Raw Material (Polymer, Surfactant, and Fiber), End Use (Industrial, and Residential), Solubility Type (Cold Water Soluble and Hot Water Soluble), Packaging Type, and Region - Global Forecast to 2025" According to MarketsandMarkets, the water soluble packaging market is estimated to be valued at USD 2.8 billion in 2019 and is projected to reach USD 3.7 billion by 2025, recording a CAGR of 5.0%. The rapidly growing environmental and sustainability concerns across the globe and government initiatives to reduce the use of plastics are driving the market for water soluble packaging.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=243293980

Water Soluble Packaging Market Key Drivers, Restraint & Challenge:

Water soluble packaging is an innovative package type that is used in place of the traditional plastic ones. The usage of plastic or plastic-based products is growing at a fast pace, however, governments across the world are working on curbing its usage. Plastics have become a crucial part of our lives through their applications and strength. The growth in the usage of single use plastics has affected the overall environmental sustainability and has, therefore, been quite a huge challenge for governments to work on.

Key Drivers:

- Growing environmental and sustainability concerns

- Usage of water soluble packaging in multiple applications

- Ban on single-use plastics

Key Restraint and Challenge:

- Secondary packaging requirements

- Higher acceptability of bioplastics

Solubility Type in Water Soluble Packaging:

Water soluble packaging solutions are packaging solutions with water soluble and biodegradable characteristics and specifications based on the packaging material solubility. The classification is based on the applications majorly considering agricultural, chemical, and water treatment industries. Due to rise in consumer awareness of the safe usage of hazardous and environment-friendly materials by eliminating non-biodegradable materials for packaging and water-soluble packaging in many countries is gaining traction.

- Cold Water

- Hot Water

Request for Customization:

Top 10 players in Water Soluble Packaging industry:

The competitive landscape provides an overview of the relative market position of the key players operating in the water soluble packaging market, based on the strength of their project offerings and business strategies, analyzed based on a proprietary model. Key players in the market have majorly adopted strategies such as new product launches, agreements, collaborations, and joint ventures, expansions, and acquisitions.

Some of the major players in the market are:

- Lithey

- Mondi Group

- Sekisui Chemicals

- Kuraray Co Ltd

- Mitsubishi Chemical Holdings

- Aicello Corporation

- AquapaK Polymers

- Lactips

- Cortec Corporation