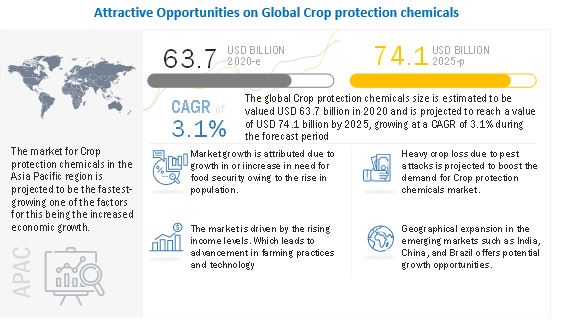

The report "Crop Protection Chemicals Market by Type (Herbicides, Insecticides, Fungicides & Bactericides), Origin (Synthetic, Biopesticides), Form (Liquid, Solid), Mode of Application (Foliar, Seed Treatment, Soil Treatment), Crop Type and Region - Global Forecast to 2025" The global Crop protection chemicals size is estimated to be valued USD 63.7 billion in 2020 and is projected to reach a value of USD 74.1 billion by 2025, growing at a CAGR of 3.1% during the forecast period. The growth of this market is attributed to an increasing need for food security of the growing population.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=380

Driver: Increase in need for food security owing to the rise in population

According to the International Food Policy Research Institute, almost 690 million people went hungry around the world in 2019, an increase of 10 million over 2018, and the COVID-19 pandemic could push an additional 83 milllion-132 million into chronic hunger in 2020, according to the 2020 State of Food Security and Nutrition in the World (SOFI) report, released July 13. The report provides the latest authoritative estimates on global hunger, malnutrition, and food insecurity.

State of Food Security and Nutrition in the World (SOFI) 2020 projects that 841.4 million people will be hungry globally by 2030 if these trends continue, and the world will not achieve its 2025 and 2030 targets of defeating malnutrition. According to the FAO Chief Economist, attributed these alarming findings to the unaffordability of healthy diets, noting that globally, 3 billion people lack the means and access to good nutrition. In order to transform food systems to reduce these costs, policy makers must look at both supply and demand. Policies should enhance the efficiencies of the food supply chain and subsidize production of nutritious foods; at the same time, expanding social safety nets and policies that encourage behavioral change can promote healthier diets.

Opportunity: Rapid growth in the biopesticides market and organic agriculture

Biopesticides are pesticides produced naturally, with minimum usage of chemicals. Since growing environmental considerations and the pollution potential and health hazards from many conventional pesticides are on an increase, the demand for biopesticides has been rising steadily in all parts of the world. Biopesticides are growing in popularity, due to their less or non-toxic nature as compared to synthetic pesticides. Moreover, biopesticides provide more targeted activity to desired pests, unlike conventional pesticides that often affect a broad spectrum of insects, birds, and mammalian species. Further, biopesticides can be very effective in small quantities, offering lower exposure and are quickly decomposable; they leave virtually no harmful residue after application.

The synthetic segment dominated the market for Crop protection chemicals by source.

Synthetic crop protection chemicals are manufactured in laboratories and are mixtures of chemicals that intend to avert, kill, repel, or destroy any pests. Synthetic crop protection chemicals are perceived to be toxic and dangerous if proper chemicals are not used. However, since the past 60 years, various innovative synthetic crop protection chemicals have been developed which are less toxic and more effective on crops. Due to innovative product development by the leading crop protection chemical manufacturing companies such as BASF SE (Germany), various new and more pest-specific synthetic crop protection chemicals are being developed, which cause less damage to the environment.

Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=380

Asia Pacific is the fastest-growing market during the forecast period in the global Crop protection chemicals

The key markets in the Asia Pacific region include China, India, Japan, and the Rest of Asia Pacific. The Asia-Pacific, a region where agricultural systems and technologies vary from one country to another, consists of about 40%, that is, 600 million hectares of the global crop area. Rice cultivation and the predominance of small-scale manufacturers are widely seen across all the countries of the Asia-Pacific region.

The increasing awareness about pesticides and continuous technological advancements are factors contributing to the growth of this market. In addition to this, the growing demand for crops and rising cultivation in the countries of Asia-Pacific have forced agribusiness companies to expand their supplier and manufacturing base in the region.