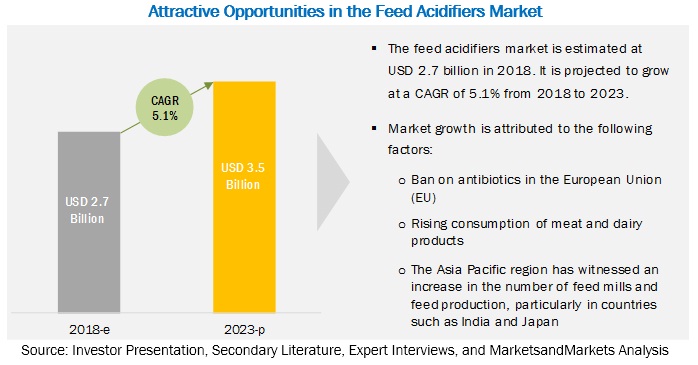

The report "Feed Acidifiers Market by Type (Propionic Acid, Formic Acid, Lactic Acid, Citric Acid, Sorbic Acid, Malic Acid), Form (Dry, Liquid), Compound (Blended, Single), Livestock (Poultry, Swine, Ruminants, Aquaculture), and Region - Global Forecast to 2023" Over the years, the production pattern in the feed industry has transformed in tandem with the health requirements of livestock. For improved growth and efficiency of livestock, rearers included antibiotics as additives in feed. However, the use of antibiotics as feed additives impacts the health of animals, which, in turn, affects the health of consumers adversely. Due to the adverse effects on the health of consumers, the EU has imposed a ban on the use of antibiotics. This ban has encouraged rearers to opt for cost-effective and health-enriching alternatives such as feed acidifiers. According to MarketsandMarkets, the feed acidifiers market is projected to account for a value of USD 3.5 billion by 2023, recording a CAGR of 5.1%.

Download

PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=163262152

The Propionic Segment Is

Projected To Hold the Largest Share in the Feed Acidifiers Market

As consumers become more sensitive to food safety, rearers

are focusing on investing in feed additives that enhance the quality of meat

and prevent diseases in livestock. Rearers prefer propionic acid as feed

additives as they are a rich source of nutrients and are generally recognized

as safe (GRAS) substances by the FDA. Due to their increasing preference in the

livestock industry, the propionic segment is projected to account for the

largest share in the feed acidifiers market during the forecast period.

Dry Feed Acidifiers To Outpace the Sales of Liquid Feed

Acidifiers in the Market Throughout 2023

To maintain consistency in the application and enhance the

nutrient quotient of crops, the dry form of feed acidifiers is utilized

extensively. Demand for dry feed acidifiers is preferred as they are convenient

to store, transport, and use. Also, the dry form of feed acidifiers can be used

efficiently due to their free-flowing structure. Owing to these factors, dry

feed acidifiers are projected to outpace the sales of the liquid form during

the forecast period.

The Feed Acidifiers Market To Record the Fastest Growth in South

America During the Forecast Period

As governments in the South American region focus on

investing in the livestock sector, rearers in various countries of this region

are allocating their budget to utilize feed acidifiers. Rearers are mainly

focusing on improving the meat quality by utilizing feed acidifiers and offer

GRAS-certified produce in the market. The demand for meat and poultry products

is also projected to increase in parallel to the population growth and

disposable income of consumers in this region. Due to these factors, the market

in this region is expected to record the highest growth during the forecast

period.

Make an Inquiry:

https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=163262152

Leading players in the

feed acidifiers market are adopting strategies such as product launches,

acquisitions, expansions, and collaborations & divestments. Key players

identified in this market include Yara International ASA (Norway), Kemira OYJ

(Finland), BASF SE (Germany), Biomin Holding GmbH (Austria), and Kemin

Industries Inc., (US).

Overall, the growth of the feed acidifiers market is

projected to remain moderate during the forecast period. As the competition to

offer effective feed acidifiers intensifies in the market, leading players to

focus on expansions and collaborations to enhance their brand presence across

regions and expand their customer base. These factors are projected to

encourage high growth during the forecast period.