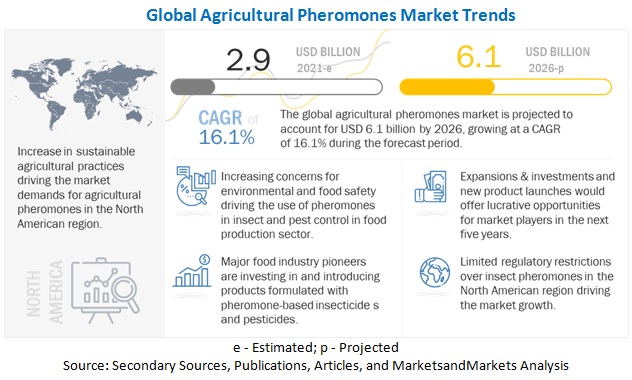

The report "Agricultural Pheromones Market by Crop Type (Fruits & Nuts, Field Crops, & Vegetable Crops), Function (Mating Disruption, Mass Trapping, Detection & Monitoring), Mode of Application (Dispensers, Traps, & Sprays), Type, and Region - Global Forecast to 2026", The global agricultural pheromones market is estimated to be valued at USD 2.9 billion in 2021. It is projected to reach USD 6.1 billion by 2026, recording a CAGR of 16.1% during the forecast period. Semiochemicals such as pheromones and allelochemicals are those biological pesticides that are organic in nature and are environmentally safe. Companies nowadays are increasing their research & development investments to diversify the application area for these pesticides and thus, propelling the growth of the overall market. Many horticulture and agriculture farmers are employing sex pheromones and attractants to decrease the number of crop-damaging insects and pests effectively.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=11243275

Impact of Covid-19 on the global agricultural pheromones market

Since the onset of the COVID-19 pandemic, consumer preferences have shifted toward consuming healthy and organic food products to maintain health and improve immunity. Other emerging industry trends, including consumption of safe, natural, clean-label, and pesticide-free products, have also changed the scenario of agriculture across the globe. COVID-19 is projected to have a considerable impact on the growth of the agricultural pheromones market. In the optimistic scenario, it is assumed that the impact would be positive, and crop protection manufacturers are willing to buy agricultural pheromones, considering the rise in demand for clean organic products and insect & pest-free environments. In addition, as the trade barriers would be relaxed to rebuild economies, trading will be easier.

Opportunities: Rising global consumption of high-value crops

High-value agricultural products are generally defined as agricultural products with a high economic value per kilogram (or pound), per hectare, or per calorie, which includes fruits, vegetables, meat, eggs, milk, and fish. The key factors driving the demand for high-value crops are the rise in the income of consumers, rapid urbanization, and the increase in awareness of health benefits associated with these high-yield crops. Since the onset of the COVID-19 pandemic, consumer preferences have shifted toward consuming healthy and organic food products to maintain health and improve immunity. Other emerging industry trends, including consumption of safe, natural, clean-label, and pesticide-free products, have also changed the scenario of agriculture across the globe.

By mode of application, the dispensers segment dominated the market in 2020, due to the ease of handling and low cost

Dispensers are utilized for the application of insect pheromones in specified amounts to different types of crops. The dispensers should be placed at a particular height to be an effective source. Dispensers are most commonly utilized to monitor insect populations in arable crops, stored products, and forest ecosystems. An ideal dispenser should be renewable and should be made of cheap organic materials alongside being economically inexpensive and toxicologically inert. Pheromone-based devices are able to ensure the successful control of pests, such as codling moths, tomato pinworm, pink bollworm, and oriental fruit moth. Pheromone dispensers are of different types, such as passive pheromone dispensers, retrievable polymeric pheromone dispensers, hollow fibers, and high emission dispensers.

Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=11243275

The North America region dominated the agricultural pheromones market and is projected to grow at the highest CAGR of 16.9% from 2021 to 2026.

The market for pheromones is growing in North America owing to the widening scope of applications in not only agriculture but also in forestry and for industrial purposes, such as in the food and pharmaceutical industries. ISCA produces a formulation to control noctuid moths on row crops that acts as a mating-disruption for the gypsy moth that is used by the US Forest Service. Some of the majorly grown agricultural crops in the region include cotton, tomatoes, grapes, corn, pome fruits, and stone fruits. These are some of the crops that are prone to attacks from various insect species, such as the pink bollworm, leaf miner, codling moth, and berry moths. In North America, pheromones are used for mating disruption purposes.

Key Market Players:

The key players in this market include Shin-Etsu Chemical Co., Ltd (Japan), Koppert Biological Systems (Netherlands), Isagro Group (Italy), Biobest Group NV (Belgium), Suterra LLC (US), Russell IPM (UK), ISCA Technologies (US), Trécé Incorporated (US), Bedoukian Research, Inc. (US), Pherobank B.V. (Netherlands), BASF (Germany), Certis Europe BV (Netherlands), Bioline AgroSciences Ltd. (US), Bio Controle (Brazil), and ATGC Biotech Pvt Ltd. (India).