The report "Rice Seeds Market by Type (Hybrid and

Open-Pollinated Varieties), Grain Size (Long, Medium, and Short), Hybridization

Technique (Two-Line and Three-Line), Treatment (Treated and Untreated Seeds),

and Region - Global Forecast to 2023", The rice seeds

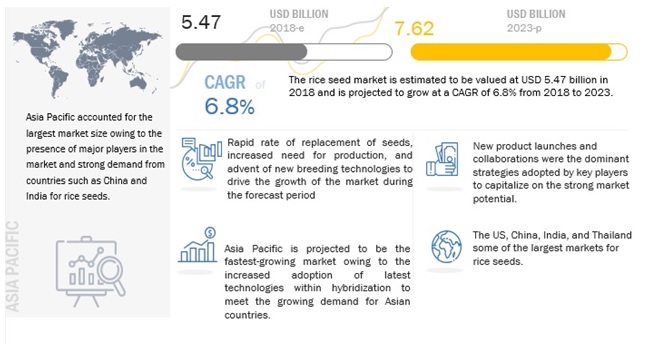

market is projected to reach USD 7.62 billion by 2023, from USD 5.47 billion in

2018, at a CAGR of 6.85% during the forecast period. The market is driven by

factors such as the increasing technological advances in rice breeding,

declining prices of hybrid rice seeds, growing adoption of hybrid rice seeds in

the developed and developing countries, and rising seed replacement rate for

paddy across Asian countries.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=129962473

Long-grain rice seeds are

estimated to be the most widely used variety of rice seeds in 2018.

Long grain rice is cultivated at a high rate across

different countries due to the changing consumer demand and limited application

of short grain rice in the food industry. The production of long rice has been

growing across the globe, particularly in the US and Asian countries. Basmati and

jasmine are some of the long grain rice varieties that are exported from Asia

in large quantities and have industrial importance from the perspective of rice

millers in terms of price value. In addition, hybrids and OPV seeds offered by

key players such as Bayer and DowDuPont are mainly for long rice grains,

followed by medium-sized rice and short rice.

The treated segment is projected to witness the fastest growth

during the forecast period.

Seed treatment has been gaining importance for field

crops, such as corn, wheat, and soybean, to reduce crop loss from early pest

attacks. However, the adoption of this technology for rice is still gradual

across countries. Rice is mainly cultivated in the Asian countries. However,

farmers are reluctant toward investing capital on crop inputs and prefer

adopting the traditional techniques of crop protection. Due to the rising need

for sustainable agriculture and integrated pest management guidelines laid by

governments in the Asian countries has encouraged farmers to adopt seed coating

technologies. On the account of these factors, this segment is projected to

grow at the highest rate during the forecast period.

Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=129962473

Asia Pacific is estimated

to dominate the market in 2018 and is projected to be the fastest-growing

market for rice seeds through 2023.

Asia Pacific is a major consumer and producer of rice

across the globe, and inadequate arable land in this region has encouraged

farmers for better yield from their cultivation. Adoption of advanced

technologies such as hybrid and certified seeds is also increasing in this

region. According to the recent data of USDA published in 2016, India and China

are the two major producers and consumers of rice, not only in the Asia Pacific

region but across the globe. The Asia Pacific market for rice seeds is

consolidated with two players occupying the largest share, followed by other

players. Since rice cultivation in other regions of the world is comparatively

low, the growth of the Asia Pacific market is projected to remain steady during

the forecast period.

This report includes a study of the development strategies, along with the product portfolios of leading companies. It also includes the profiles of leading companies such as Bayer (Germany), DowDuPont (US), Syngenta (Switzerland), Advanta Seeds (UPL) (India), and Nuziveedu Seeds (India), Mahyco (India), BASF (Germany), Kaveri Seeds (India), SL Agritech (Philippines), Rasi seeds (India), Rallis (India), JK Seeds (India), Hefei Fengle (China), LongPing (China), Guard Agri (Pakistan), and National Seeds Corporation (India).