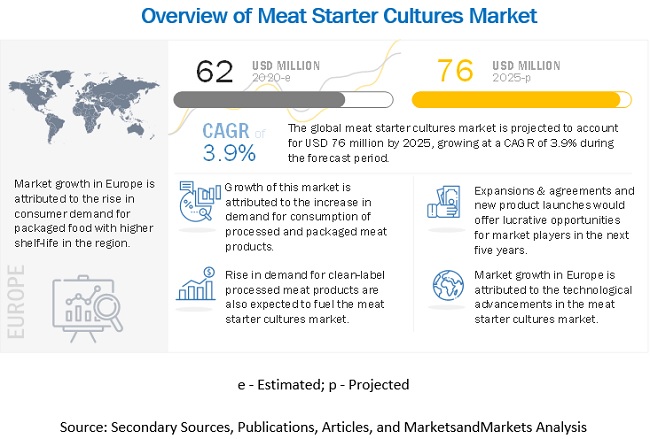

According to MarketsandMarkets, the "Meat Starter Cultures Market by Application (Sausages, Salami, Dry-cured meat, and Others), Microorganism (Bacteria, and Fungi), Composition (Multi-strain mix, Single strain, and Multi-strain), Form, and Region - Global Forecast to 2025" size is estimated to be valued at USD 62 million in 2020 and projected to reach USD 76 million by 2025, recording a CAGR of 3.9%, in terms of value. The functional properties of meat starter cultures and their benefits while incorporation in a wide range of applications are driving the global meat starter cultures market.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=43153327

By microorganism, the bacteria is projected to account for the largest share in the meat starter cultures market during the forecast period

Based on microorganism, bacteria dominated the market. Starter cultures are used to initiate the fermentation of meat products such as sausages, salami, and dry-cured meat. There are two types of microorganisms that are mainly used as meat starter cultures, namely, bacteria and fungi. Bacteria-based starter cultures are that are majorly used in the industry include lactic acid bacteria (LAB) and coagulase-negative staphylococci (CNS). These are the dominant microorganisms that are used in meat products to prohibit pathogens and spoilage microorganisms during the pre-and post-processing of meat products.

By application, sausages segment is projected to account for the largest share in the meat starter cultures market during the forecast period

By application, the market is segmented into sausages, salami, dry-cured meat, and others (such as pepperoni and other processed-meat products). The meat sausages segment, akin to most other non-processed fresh meats and meat preparations, comprises perishable food products, and most sausage manufacturers have been looking for additional safety or longer shelf life, either in terms of less spoilage or delayed oxidation. Meat starter cultures are used to provide additional safety and delay spoilage by shifting the uncontrolled fermentation that spoils the meat to a controlled fermentation by safe bacteria. Meat starter cultures ferment the sausages and preserve their flavor, texture, color, and increase their shelf-life by averting wastage.

Europe is projected to account for the largest market share during the forecast period

Europe has been a major contributor to the growth of the processed meat industry, as a huge percentage of consumers have been inclined toward packaged meat applications such as sausages, salami, and dry-cured meat. The busier lifestyles of consumers in Western European countries such as Germany, the UK, France, and Italy have been propelling the demand for meat products with higher shelf-life. Therefore, augmenting the demand for meat starter cultures in this region. The European region consists of some of the major manufacturers from the meat starter culture market, such as Chr. Hansen (Denmark), DSM (Netherlands), Kerry Group (Ireland), Biochem SRL (Italy), and Sacco SRL (Italy). These key players have been bolstering the usage of meat starter cultures in this region by offering technologically advanced equipment for monitoring and usage of meat starter cultures.

Request for Customization:

https://www.marketsandmarkets.com/requestCustomizationNew.asp?id=43153327

https://www.marketsandmarkets.com/requestCustomizationNew.asp?id=43153327

Key Market Players:

Chr. Hansen (Denmark), DSM (Netherlands), Kerry (Ireland), DuPont (US), Frutarom (Israel), Galactic (Belgium), Lallemand (Canada), Proquiga (Spain), Westcombe (UK), Biochem SRL (Italy), RAPS GmbH (Germany), DnR Sausages Supplies. (Canada), Sacco System (Italy), Canada Compound (Canada), Biovitec (France), Genesis Laboratories (Bulgaria), Meat Cracks (Germany), THT S.A. (Belgium), Stuffers Supply Co. (Canada), MicroTec GmbH (Germany), and Codex-Ing Biotech (US).