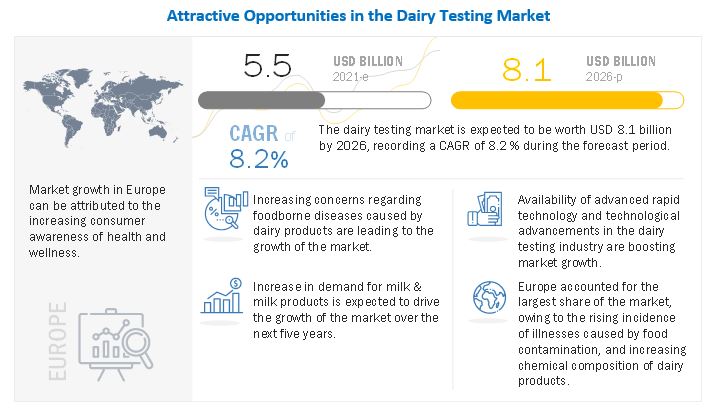

The report "Dairy Testing Market by Type (Safety (Pathogens, Adulterants, Pesticides), Quality), Technology (Traditional, Rapid), Product (Milk & Milk Powder, Cheese, Butter & Spreads, Infant Foods, ICE Cream & Desserts, Yogurt), and by Region - Global Forecast to 2026" The global dairy testing market is estimated to be valued at USD 5.5 billion in 2021 and is projected to reach a value of USD 8.1 billion by 2026, growing at a CAGR of 8.2% during the forecast period. Increase in consumer awareness regarding the safety and quality of food products, stringent regulations imposed by the regulatory bodies, and increased in the global dairy trade, have been driving the global dairy testing market.

Download PDF Brochure @

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=240885146

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=240885146

The milk & milk powder segment is estimated to witness the largest growth in the dairy testing market, in terms of value, in 2021

Among different types of dairy products, milk & milk powder segment accounted for the largest share in 2021. Milk & milk powder may be contaminated due to poor hygiene conditions during processing, storage, and transportation. Milk powder is a direct substitute for fluid milk; hence, used in varied applications, including bakery, dairy, and infant nutrition. As an after-effect of COVID-19 lockdown, an evident dip in sales and stockpiling of unsold milk powder has been plaguing the dairy industry.

The Campylobacter in the pathogen segment is estimated to account for a larger market share in the dairy testing market, in terms of value, in 2021

The most common pathogens in milk and dairy products include Bacillus cereus, Listeria monocytogenes, Yersinia enterocolitis, Escherichia coli, Salmonella, Yersinia enterocolitis, and Staphylococcus aureus. The contaminated milk or dairy product, upon consumption, can cause several diseases in human beings. Campylobacter is a gram-negative, spiral-shaped, and extremely motile bacterium responsible for food contamination and poisoning. The bacterium is found in the tract of warm-blooded animals such as cattle, sheep, pigs, dogs, and goats, and in birds, especially poultry. In humans, campylobacter can cause diarrhea, cramping, abdominal pain, and fever.

Speak to Analyst @ https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=240885146

The rising demand for dairy testing in the European markets has created opportunities for dairy testing service providers.

The Europe region is the dominant market for dairy testing and is expected to experience the fastest growth only second to Asia-Pacific. The major producers of milk in the EU region are Germany, France, Poland, the Netherlands, Italy, and Spain. Together these countries account for around 70% of the total milk production. Globalization has increased the international trade of milk and dairy products and has had a major impact on global dairy supply. However, the increase in trade has resulted in higher risk of contaminated milk and dairy products reaching dairy producers and processors, and end consumers in distant markets due to instances of cross-contamination, exposure to toxins, microorganisms, and other contaminants. Manufacturers have been using dairy testing services to ensure safety and quality of their products and to comply to the international standards.

This report includes a study on the marketing and development strategies, along with the product portfolios of the leading companies operating in the dairy testing market. It includes the profiles of leading companies such as SGS SA (Switzerland), Bureau Veritas (France), Eurofins (Luxembourg), Intertek (UK), TÜV SÜD (Germany), TÜV NORD GROUP (Germany), ALS Limited (Australia), Mérieux NutriSciences (US), Neogen Corporation (US), Romer Labs (Austria), Microbac Laboratories (US), AsureQuality (New Zealand).